When it comes to your family's future, one of the kindest things you can do is plan for the costs you’ll leave behind. Using life insurance for funeral costs is a smart, compassionate way to shield your loved ones from a huge financial hit during an already heartbreaking time.

Think of it as a dedicated safety net. The policy provides a cash payout directly to your family, giving them immediate funds to handle a burial, memorial service, and other final expenses without draining their own savings or going into debt.

Protecting Your Family from Final Expense Burdens

Planning for your end-of-life costs isn't just about money; it's a profound act of love. Let's be real—a funeral can be one of the biggest expenses a family ever has to face, and it often comes out of nowhere, creating a ton of stress.

Imagine your family suddenly getting a bill for $10,000 or more. It happens all the time. This is where life insurance steps in, acting as a financial shield so they can focus on what truly matters: grieving and remembering.

The Real Impact of Unplanned Expenses

Without a plan in place, families are often forced to make tough choices under immense pressure. They might have to pull money from retirement accounts, run up high-interest credit cards, or even turn to crowdfunding just to cover the costs. It's a financial scramble that only adds to their grief.

A life insurance policy designed for funeral costs changes that entire story. Here’s how:

- Immediate Cash: The policy pays out a lump sum, so your family gets access to the money they need, right when they need it.

- Financial Protection: It keeps their personal savings and other assets safe, so they aren't depleted by final expenses.

- Peace of Mind: Most importantly, it allows them to grieve and heal, knowing the bills are taken care of.

By planning ahead, you make sure your legacy is one of love and support, not unexpected financial burdens. You're giving your family the gift of security when they are at their most vulnerable.

The person you name as your executor will have a mountain of tasks to handle, from managing assets to paying off debts. A good executor duties checklist is a lifesaver, and having funds from an insurance policy makes their job infinitely smoother.

These policies, often called burial insurance or final expense insurance, are built specifically for this purpose. In this guide, we'll walk you through your options, help you figure out how much coverage you need, and show you how to find a policy that brings true peace of mind.

Decoding the Types of Life Insurance for Funeral Costs

Trying to figure out life insurance for final expenses can feel like a chore, but it really boils down to a few straightforward options. Instead of getting bogged down in confusing terms, let’s break down what each policy does and who it’s really for.

Think of it this way: each type of life insurance is a different tool designed for a specific job. Some are perfect for one particular task, while others are more of a multi-purpose solution. Understanding the difference is the key to choosing with confidence.

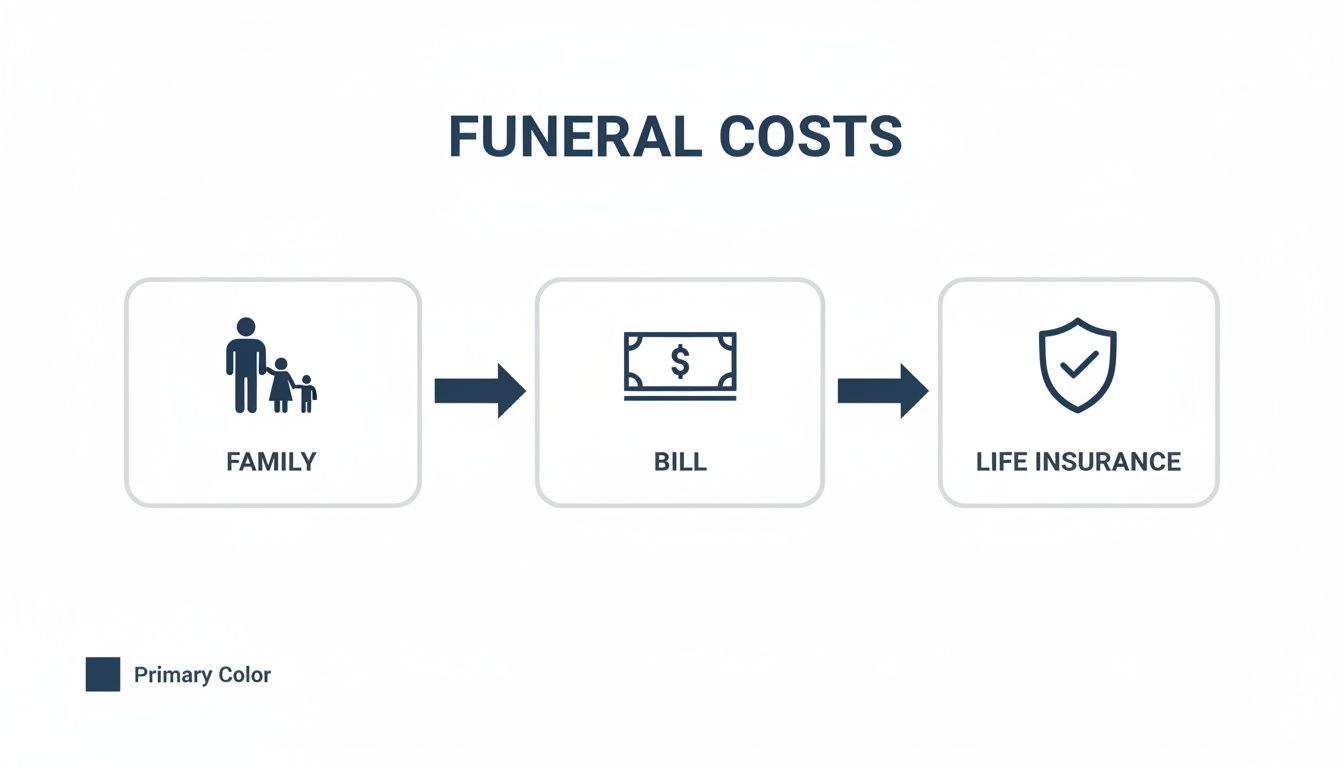

This flowchart lays it all out, showing how a life insurance policy steps in to shield a family from the financial stress of a funeral bill.

As you can see, life insurance acts as a safety net, catching the financial weight of funeral bills so your family doesn't have to.

Final Expense Insurance: The Specialist

Think of Final Expense Insurance (often called burial insurance) as a dedicated fund with one clear purpose: to cover funeral costs and other end-of-life bills. These policies are built to be simple and accessible.

- Coverage Amounts: You’ll typically find smaller coverage amounts, from $5,000 to $25,000, which lines up perfectly with the average cost of a funeral.

- Best For: It’s a great fit for seniors, anyone with health issues, or someone who just wants a straightforward policy for their final arrangements without any fuss.

- Key Feature: The biggest draw is often the "simplified underwriting." This usually means no medical exam is needed—just a few health questions to answer.

This focus on simplicity is why its popularity is soaring. The global market for burial insurance hit USD 280 billion in 2023 and is expected to jump to USD 463.7 billion by 2032. It shows just how many families are taking proactive steps to handle these costs.

Term Life Insurance: The Temporary Shield

Term Life Insurance is like renting financial protection for a set amount of time. You pick a "term"—say, 10, 20, or 30 years—and if you pass away during that window, your family gets a payout. It’s fantastic for covering big, temporary responsibilities like a mortgage or replacing your income while your kids are growing up.

While you can use it for funeral costs, that’s not what it was designed for. The catch is that if the policy expires and you're still alive, the coverage ends. You’d have to get a new policy, likely at a much higher price because you’re older.

Whole Life Insurance: The Lifelong Asset

If term life is like renting, Whole Life Insurance is like owning. It covers you for your entire life, as long as the premiums are paid. It also has a "cash value" component that grows over time, which you can even borrow against if you ever need to.

A whole life policy provides a guaranteed death benefit that can easily handle funeral costs and leave extra for your loved ones. The trade-off for this lifelong coverage and cash value? The premiums are quite a bit higher than both term and final expense insurance. It’s also important to understand the fine print, like how guardianship might impact life insurance policies in Texas, for example.

Comparing Life Insurance Options for Funeral Costs

To make things even clearer, here’s a quick side-by-side look at how these three main options stack up when your goal is covering funeral expenses.

| Feature | Final Expense Insurance | Term Life Insurance | Whole Life Insurance |

|---|---|---|---|

| Primary Purpose | Covering final expenses like funerals and medical bills. | Income replacement and covering large, temporary debts. | Lifelong financial protection and wealth transfer. |

| Coverage Length | Your entire life. | A specific period (e.g., 10, 20, 30 years). | Your entire life. |

| Coverage Amount | Smaller ($5,000 – $25,000). | Larger (often $100,000+). | Can be large, but available in smaller amounts too. |

| Premiums | Low and affordable. | Very low for young, healthy individuals. | Significantly higher than term or final expense. |

| Medical Exam | Usually not required. | Often required for higher coverage amounts. | Usually required. |

| Cash Value | Typically no, or a very small amount. | No. | Yes, it grows over time and can be borrowed against. |

| Best For Funerals? | Excellent. Specifically designed for this purpose. | Okay, but risky. Only works if you pass away during the term. | Very good. Provides a guaranteed payout but is more expensive. |

Each policy has its place, but when it comes to covering a funeral, Final Expense insurance is often the most direct and cost-effective tool for the job.

Guaranteed Issue Life Insurance: The Safety Net

What if you have serious health problems that make it hard to get approved for other policies? That's where Guaranteed Issue Life Insurance comes in. It’s a true safety net.

Just as the name says, your acceptance is guaranteed if you’re within the eligible age range (usually 50-85). There are no health questions and no medical exam. Period.

To balance this risk, these policies have a couple of key features:

- Lower Coverage: The payout is typically capped at around $25,000.

- Graded Death Benefit: If you pass away from natural causes in the first two or three years, your beneficiary usually gets back all the premiums you paid, plus some interest. The full death benefit is paid out after that waiting period.

This structure makes sure that everyone, regardless of their health, has a way to secure some coverage for their final expenses.

If you’d like to dive deeper, our guide on the different types of life insurance explained covers all these options in more detail.

How to Accurately Estimate Your Final Expenses

Figuring out the right amount of life insurance for funeral costs isn’t a guessing game. It’s about creating a clear, realistic budget so your family has exactly what they need—without you paying for coverage you don’t. Think of it as drawing a financial map for them to follow during a difficult time.

This turns a vague worry into a concrete plan, giving you real confidence that every detail is covered. Many people are shocked when they see what a modern funeral actually costs, but facing the numbers head-on is the first step to true peace of mind.

And the numbers can be jarring. In the U.S., the median funeral cost hit $7,848 in 2023, a 12.5% jump from 2014. Globally, you can expect to see prices anywhere from $4,000 to $10,000. That’s why the burial insurance market is expected to surge from $142.9 billion to $370.1 billion by 2032, as more families look for ways to avoid that financial hit. You can read the full research on the burial insurance market to see the trends for yourself.

Breaking Down the Major Funeral Service Costs

The biggest chunk of your budget will almost always go to the funeral home's professional services. These fees are the foundation of any funeral arrangement, covering all the essential logistics and paperwork.

Here’s a look at what you should plan for:

- Professional Service Fee: This is the non-negotiable base fee. It covers the funeral director’s time, planning, securing permits, and coordinating everything. It’s the operational cost of the business.

- Embalming and Body Preparation: If you’re planning a public viewing, embalming is usually required. This line item also includes things like cosmetology and dressing.

- Facility Use: This is the fee for using the funeral home for the viewing, wake, or memorial service.

- Transportation: This covers the hearse used to transport the body to the funeral home and then to the cemetery or crematory.

These core services alone can easily run into thousands of dollars, making up the bulk of the final bill.

Itemizing Casket, Burial, and Cemetery Expenses

After the funeral home’s services, the next set of big-ticket items relates to the burial itself. These costs can swing wildly depending on your choices and where you live.

Your checklist for these expenses should include:

- Casket or Urn: A casket is often the single most expensive item, with prices ranging from $2,000 for a basic model to over $10,000 for high-end options. An urn for ashes is a far more affordable choice.

- Burial Plot: The price of a cemetery plot depends heavily on location. A plot in a rural town might be a few hundred dollars, while one in a major city could cost thousands.

- Headstone or Grave Marker: A simple, flat marker might be around $1,000, but a more traditional, upright headstone can easily cost $3,000 or more.

- Opening and Closing of the Grave: This is what the cemetery charges for the labor of digging and filling the grave.

Key Takeaway: The single biggest choice affecting your final cost is burial versus cremation. Cremation is almost always the more budget-friendly option.

For a more precise estimate tailored to you, an online tool can make all the difference. Play around with different options using our life insurance needs calculator to get a clearer picture.

Accounting for Often-Overlooked Costs

Finally, there are all the smaller details that make a service personal and meaningful—and they all come with a price tag. These costs add up fast if you don't account for them.

Make sure to include these items in your final budget:

- Flowers: Floral arrangements for the casket and service.

- Obituary Notices: Fees to publish an obituary in local papers.

- Memorial Service Items: Printing costs for programs, guest books, or thank-you cards.

- Reception or Wake: Expenses for a venue, catering, or refreshments for guests.

- Outstanding Debts: Don't forget any final medical bills or small credit card balances that will need to be paid off.

Once you add up these three categories—professional services, burial items, and the miscellaneous costs—you’ll have a realistic total. That’s the number your life insurance policy should aim to cover, ensuring your family isn’t left solving a financial puzzle.

Understanding Policy Costs at Different Ages

When you're looking into life insurance for funeral costs, the first question is usually pretty simple: "What's this going to cost me?"

The good news is that these policies are designed to be affordable. But the final price tag isn't just a random number. Insurers carefully calculate it based on your personal profile to assess risk—the lower your risk, the lower your monthly premium.

This is where planning ahead becomes your biggest superpower. Getting a policy when you're younger and healthier lets you lock in a much lower rate that will never go up. That adds up to serious savings over the years.

The Key Factors Driving Your Premium

Insurers look at four main things to figure out your monthly premium for a final expense policy. Each one plays a part.

- Your Age: This is the big one. The younger you are when you buy, the less you'll pay for the same amount of coverage.

- Your Health: Many final expense policies don't require a full medical exam, but they will ask some health questions. Better health usually means a better rate.

- Your Gender: It's a statistical fact—women tend to live longer than men. Because of that, women often pay slightly less for life insurance than men of the same age.

- Coverage Amount: This is straightforward. The more coverage you want (say, $20,000 instead of $10,000), the higher your premium will be.

Once you understand these pieces, it's easy to see why getting a quote sooner is always better. Every year you wait, the cost for the exact same policy is likely to climb.

Real-World Premium Examples

Seeing actual numbers makes it all much more real. To give you a clear idea of what to expect, let's look at some sample monthly costs for a $15,000 final expense policy.

Estimated Monthly Premiums for a $15,000 Final Expense Policy

| Applicant Profile | Estimated Monthly Premium (Non-Smoker) | Estimated Monthly Premium (Smoker) |

|---|---|---|

| 40-Year-Old Female | $25 – $35 | $35 – $45 |

| 40-Year-Old Male | $30 – $40 | $45 – $60 |

| 50-Year-Old Female | $35 – $45 | $50 – $65 |

| 50-Year-Old Male | $45 – $55 | $70 – $90 |

| 65-Year-Old Female | $55 – $75 | $90 – $120 |

| 65-Year-Old Male | $70 – $95 | $125 – $160 |

The difference is pretty stark, isn't it? A 40-year-old might secure $15,000 in coverage for about the cost of a few lattes a month. Someone in their 60s will pay more for that same peace of mind.

This shows that acting early is the single best way to make life insurance for funeral costs as affordable as possible. It’s a small, manageable expense today that protects your family from a much larger one tomorrow.

Navigating the Application and Approval Process

The thought of applying for life insurance can feel like a huge task, especially if you’re managing a few health conditions. Lots of people picture stacks of paperwork and a medical exam, but when it comes to life insurance for funeral costs, the process is usually far simpler than you’d imagine.

Insurers know that not everyone is in perfect health, so they’ve created different ways to get you covered. The secret is to understand the different types of underwriting—which is just the fancy term for how an insurance company reviews your application to decide if they can cover you and at what price.

The Traditional Route: Fully Underwritten Policies

A fully underwritten policy is the most detailed application you can go through. It typically means answering a long list of health questions, letting the insurer see your medical records, and completing a medical exam.

While this approach is thorough, it’s not something you’ll usually see for smaller final expense policies. It’s more for people seeking large term or whole life policies with huge coverage amounts. When you’re just looking to cover a funeral, there are much easier paths.

The No-Exam Sweet Spot: Simplified Issue

This is where final expense insurance really comes into its own. A simplified issue policy hits that perfect sweet spot, which is why it’s so popular for covering funeral expenses.

There’s no medical exam involved. Instead, you just have to answer a few health questions on the application. They’re usually very direct, asking about major health events like a recent cancer diagnosis, heart attack, or stroke.

- No Medical Exam: You can skip the needles and the hassle of a doctor’s visit.

- Quick Approval: Because it’s so straightforward, approval often comes in a matter of days, not weeks.

- Accessible for Many: This opens the door for people with managed chronic conditions who might otherwise worry they won’t qualify.

This streamlined approach is the go-to for millions of Americans looking for affordable life insurance for funeral costs. To get a better feel for how it all works, you can explore the complete life insurance underwriting process and see why no-exam options are so common.

Your Safety Net: Guaranteed Issue

But what happens if your health history makes even a simplified issue policy a no-go? That’s exactly why guaranteed issue life insurance exists. Just like the name says, your approval is guaranteed as long as you fall within the eligible age range (usually 50-85).

There are zero health questions and zero medical exams. You are accepted based on your age, period. This makes it an absolute lifeline for anyone with significant pre-existing conditions.

Now, to make this work, these policies have a unique feature called a graded death benefit. Here’s the breakdown:

If you pass away from natural causes (like an illness) during the first two or three years of the policy, your beneficiary gets back all the premiums you paid, plus a little extra interest (often around 10%). If your death is accidental, the full benefit is paid out, even on day one. After that initial waiting period is over, the full death benefit is paid no matter the cause of death.

This structure ensures that absolutely everyone has an option, providing a critical safety net for the people they love most.

Ready to Protect Your Family? Here's What to Do Next.

You’ve done the hard part. You’ve learned how life insurance can cover funeral costs and why it’s such a powerful gift to your loved ones. Now, you know how to turn that worry into a solid plan.

The final step isn’t complicated. It’s about taking what you’ve learned—about the different types of policies, how to estimate costs, and what to expect—and putting it into action. It’s about securing that peace of mind for good.

Let’s walk through it together.

Taking Action in Three Easy Steps

There’s no pressure here. No mountain of paperwork. This is just about exploring your options and finding a plan that feels right for you.

-

Get Your Free Quote Online: First things first, let’s see what’s out there. Grab a no-obligation quote from My Policy Quote to instantly compare plans and rates that fit your age and budget. This gives you a real, practical starting point.

-

Chat with a Friendly Advisor: Numbers are great, but sometimes you just need to talk to a real person. A quick call with one of our licensed professionals lets you ask specific questions about your health, family, and goals. It’s a simple conversation to make sure you’re on the right track.

-

Compare and Choose with Confidence: With your personalized options in hand, you can lay them out side-by-side. Compare the coverage, the monthly premiums, and the benefits. You’ll be able to confidently pick the policy that gives your family the exact protection you want them to have.

Taking this step is a true act of love. It turns a potential future burden into a guarantee of support, ensuring your legacy is one of care, not financial stress. ❤️

This whole process is designed to be simple and empowering. By investing a few minutes today, you’re locking in invaluable comfort for the future, knowing you’ve got a plan in place to protect the people who matter most.

Frequently Asked Questions

Thinking about life insurance for funeral costs brings up a lot of questions. It’s natural. Getting clear, honest answers is the best way to feel confident you’re making the right choice for your family.

Let’s go over a few of the most common questions we hear from people just like you. Think of this as clearing up the last few details, so you can see the full picture.

Can My Family Use the Payout for Other Expenses?

Yes, they absolutely can. The death benefit from a final expense policy is paid directly to your beneficiary as a tax-free, lump-sum of cash. They have total freedom to use it where it's needed most.

While its main purpose is covering funeral costs, that money can also help with:

- Paying off lingering medical bills.

- Clearing small debts, like a credit card balance.

- Covering household bills while your loved ones adjust.

This flexibility is a huge relief. It means your family has the resources to handle whatever comes their way, not just the funeral itself.

What if I Already Have Life Insurance Through Work?

Having life insurance through an employer is a great perk, but it comes with a big string attached: it's almost always tied to your job. This is called group life insurance, and you usually can't take it with you.

If you change jobs, get laid off, or retire, that coverage often vanishes. You could be left with no protection at an age when finding a new policy is much more expensive.

A personal final expense policy is yours and yours alone. You own and control it. It stays with you no matter where you work, giving your family a permanent safety net you can count on.

This private ownership ensures the plan you put in place will be there when it’s needed, no matter what happens in your career.

Is Final Expense Insurance Better Than a Prepaid Funeral Plan?

For most people, yes. Final expense insurance offers far more flexibility and real value than a prepaid funeral plan. A prepaid plan locks you into one specific funeral home and a fixed list of services.

That sounds simple, but it can create real problems down the road:

- What if you move? Your plan might not transfer to a funeral home in another city or state.

- What if the business closes? If the funeral home goes out of business, your family’s investment could be gone.

- What if prices go up? Some prepaid plans don't cover everything, leaving your family with surprise bills for things you thought were paid for.

A final expense policy, on the other hand, gives your family a cash benefit. They can shop around, choose any funeral home they want, and use any leftover money for other needs. That control and freedom make it a much better way to protect your loved ones from stress.

Ready to give your family financial security and yourself true peace of mind? The team at My Policy Quote is here to help you find an affordable plan that fits your life perfectly. Get your free, no-obligation quote from My Policy Quote today!