Trying to figure out the cost of Medicare Part D can feel like you're trying to nail Jell-O to a wall. It’s not a single, simple price tag. Instead, it’s a blend of different costs that shift based on your prescriptions, your income, where you live, and the specific plan you choose. It's incredibly personal.

Understanding the Total Cost of Medicare Part D

Let’s be honest, untangling your Part D costs can feel like you’re trying to solve a puzzle with moving pieces. Your out-of-pocket expenses aren't static—they change throughout the year.

Think of it like your monthly utility bill. You have a fixed service fee just to be connected (that’s your premium). Then, there's a certain amount of usage you have to cover entirely on your own at the start (your deductible). After that, the company starts sharing the cost with you, but your portion depends on how much electricity you actually use (your copays and coinsurance for drugs).

This means what you pay in January might be very different from what you pay in July, all depending on the medications you take and how much you've already spent.

The Key Pieces of the Cost Puzzle

To really get a handle on what you'll pay, you need to understand the moving parts. Each one plays a different role in your annual healthcare budget.

Here’s what really drives your final costs:

- Your Plan Choice: Every private insurance company designs its own plans with different premiums, deductibles, and cost-sharing rules. No two are exactly alike.

- Your Prescriptions: This is the big one. The specific drugs you need—and whether they’re generic, brand-name, or specialty medications—will have the largest impact on your spending.

- Your Location: Where you live matters. Premiums and plan availability can vary a lot from one state or even one county to the next.

- Your Income: If you have a higher income, you may have to pay an extra monthly amount called the Income-Related Monthly Adjustment Amount (IRMAA).

To get a clear snapshot of these costs, here’s a quick breakdown:

Your Medicare Part D Cost Components at a Glance

| Cost Component | What It Is | When You Pay It |

|---|---|---|

| Premium | Your fixed monthly fee to keep your plan active. | Every month, whether you use prescriptions or not. |

| Deductible | The amount you must pay out-of-pocket for your drugs before your plan starts to pay its share. | At the beginning of the year, until the deductible amount is met. |

| Copayment | A fixed dollar amount you pay for a prescription after meeting your deductible. | Each time you fill a prescription. |

| Coinsurance | A percentage of the cost of a prescription that you pay after meeting your deductible. | Each time you fill a prescription. |

Each of these components works together to determine your total out-of-pocket spending for the year.

A Look at National Averages and Trends

While your own costs are unique, looking at the national numbers can give you a useful benchmark. For example, Medicare Part D premiums have stayed fairly steady over the years.

The average monthly premium for a standalone drug plan is around $45 in 2025, which is a small bump up from $42 in 2024. But remember, this is just an average. The actual premiums people pay can range from $0 to over $100 per month, depending on the plan and location.

On top of that, individuals with higher incomes—starting at $106,000 for an individual—will pay an extra surcharge on their premiums, anywhere from $13.70 to $85.80 per month.

Getting a grip on these individual pieces is the first step to planning effectively. For a full look at how this fits into your larger retirement healthcare picture, our guide on comprehensive Medicare planning can help. In the next sections, we’ll dive deeper into each cost and coverage stage, so you can choose your plan with total confidence.

Untangling the Four Key Costs of Part D

Trying to figure out Medicare Part D costs can feel like you’re looking at a puzzle with a lot of moving pieces. But once you understand the four main parts, the whole picture becomes much clearer. Instead of one single price, your total annual cost is a mix of these components working together.

Getting a handle on each one helps you see beyond the monthly price tag and choose a plan that actually works for your health needs and your wallet. Let's walk through them one by one.

The Monthly Premium

This is the most straightforward cost. Your premium is the fixed amount you pay the insurance company each month to keep your Part D coverage active. Think of it like a gym membership—you pay it every month, whether you use it or not.

Premiums are all over the map. Some Medicare Advantage plans wrap in Part D coverage for a $0 premium, while standalone drug plans can run from under $20 to over $100 a month. It's tempting to grab the plan with the lowest premium, but be careful. A super-low monthly payment often means you'll face a higher deductible or bigger copays when you actually go to the pharmacy.

A plan’s premium is almost always a trade-off. A low monthly bill might look great, but it could lead to higher out-of-pocket costs down the line. It's so important to look at the total package, not just this one number.

The Annual Deductible

The deductible is what you have to pay out-of-pocket for your prescriptions before your plan starts to help out. For 2026, Medicare sets a maximum standard deductible, but some plans will offer a lower one—or even a $0 deductible—to be more competitive.

Think of it as your initial buy-in for the year's drug costs. You'll pay 100% of the pharmacy price for your medications until you've spent enough to hit that deductible amount. Once you do, you enter the next phase of coverage, where you start sharing the cost with your plan. If you want to get deeper into the nuts and bolts, check out our guide on the Part D Medicare deductible.

Copayments and Coinsurance

After your deductible is met, you don't stop paying entirely. Instead, you start sharing the cost with your insurance plan through either copayments or coinsurance. This is what you pay each time you fill a script.

- Copayment (Copay): This is a simple, flat fee. For example, you might pay $10 for a generic drug or $45 for a preferred brand-name. Copays are great because they're predictable and make it easy to budget.

- Coinsurance: This is a percentage of the drug's total cost. You might pay 25% for a specialty medication. So, if your drug costs $400, your share is $100. The catch? This amount can go up or down if the drug's price changes.

Knowing which of your medications are in which cost tier is crucial. When you're adding up the potential costs of a Part D plan, understanding the details of your prescriptions, like whether you take antiarrhythmic drugs, helps you get a much more accurate estimate of these expenses.

The Late Enrollment Penalty

This last one isn't a cost for everyone, but it's a critical one to avoid. The late enrollment penalty is an extra fee that gets tacked onto your monthly premium—for life. It kicks in if you go without a creditable prescription drug plan for 63 consecutive days or more after you first become eligible for Medicare.

The penalty is calculated as 1% of the "national base beneficiary premium" for every full month you went without coverage. That amount is then permanently added to your monthly bill. The government created this penalty to encourage everyone to sign up on time, which helps keep the program affordable for all. Staying clear of this penalty is one of the smartest moves you can make to manage your long-term Medicare costs.

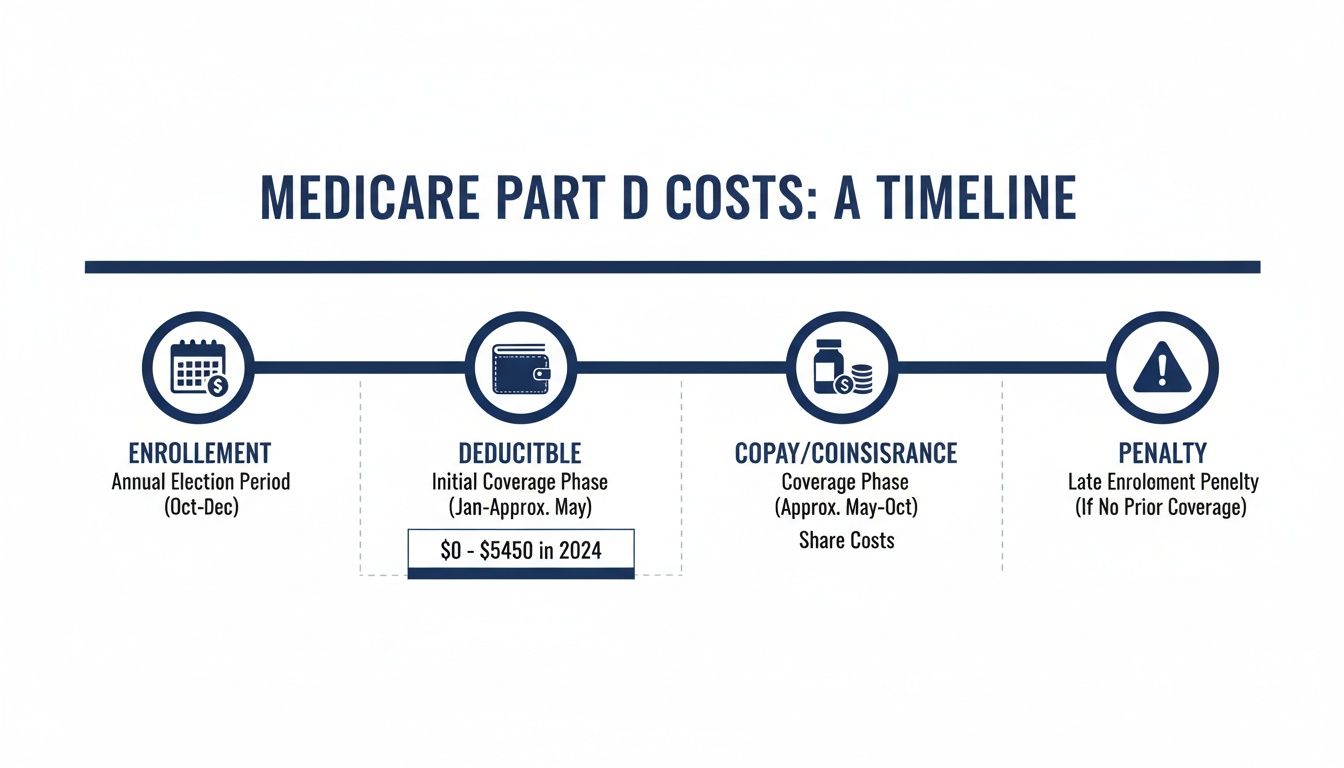

Understanding the Four Coverage Stages of a Part D Plan

When it comes to Medicare Part D, your costs aren't set in stone for the entire year. They actually change as you move through four distinct coverage stages. Think of it as a journey with different checkpoints. Each time you hit a certain spending milestone, the rules for what you pay can shift.

It's a year-long cycle, and knowing what to expect in each phase is the key to managing your prescription drug spending.

Here’s a quick visual that lays out the path your costs will follow throughout the year.

This timeline gives you a bird's-eye view of how costs progress, starting with your deductible, moving into your regular copays, and highlighting why avoiding penalties is so crucial. Each stage builds on the last and directly impacts your total out-of-pocket expenses.

Stage 1: The Deductible Stage

Your journey begins here every January 1st. In the Deductible Stage, you're responsible for 100% of your prescription drug costs until you meet your plan's annual deductible.

For 2026, Medicare sets a maximum standard deductible, but some plans will offer a lower one—or even a $0 deductible—to be more competitive.

So, if your plan’s deductible is $545, you’ll pay the full retail price for your medications until your total spending hits that $545 mark. After that, you move into the next stage where your plan starts helping out.

Stage 2: The Initial Coverage Stage

Once your deductible is met, you’ve officially entered the Initial Coverage Stage. This is where your plan really kicks in. Instead of paying the full price, you'll just pay a set copayment (like $15) or coinsurance (a percentage) for each prescription.

You and your insurance plan share the costs during this phase. This continues until the total amount spent on your drugs—combining what you've paid and what your plan has paid—reaches $5,450 for 2026. Most people with low-cost, generic prescriptions will spend the entire year in this stage.

Stage 3: The Coverage Gap (aka The Donut Hole)

If your total drug spending hits that $5,450 limit, you enter the Coverage Gap, which most people know as the "donut hole." Years ago, this phase meant paying a lot more out of pocket, but thankfully, that's changed.

Today, while you're in the donut hole, you'll pay no more than 25% of the cost for both your brand-name and generic drugs. You'll stay in this stage until your out-of-pocket spending for the year reaches a certain limit. For a deeper dive, you can learn more about the insurance donut hole in our complete guide.

The name "donut hole" can sound scary, but it's not a total black hole of coverage anymore. Thanks to new rules and manufacturer discounts, your costs are capped, providing a much-needed safety net that didn't exist in the past.

Stage 4: Catastrophic Coverage

Finally, if your out-of-pocket costs reach a high enough threshold, you enter the Catastrophic Coverage stage. This is the final and most protective phase of Part D, designed to shield you from truly overwhelming drug costs for the rest of the year.

Once you’re here, your cost-sharing drops dramatically. In fact, starting in 2025, a major change kicked in: once you hit the catastrophic threshold, your out-of-pocket costs for covered drugs fall to $0 for the rest of the year. This is a massive relief for anyone who relies on expensive, life-saving medications.

Seeing Part D Costs in the Real World

Knowing the rules of Medicare Part D is one thing. Seeing how they actually play out for real people—that’s where it all starts to make sense. The cost of Medicare Part D isn’t just a single number on a website; it’s a personal journey that looks completely different for everyone.

To bring these ideas to life, let’s walk through the year with three different people: Susan, Robert, and Maria. Each one has their own health needs, and you'll see how the Part D stages affect them in totally different ways.

Scenario 1: Susan and Her Low-Cost Generics

Susan is in great health and only takes two common generic pills—one for her blood pressure and another for cholesterol. Her plan is straightforward, with a $50 monthly premium and the standard $545 deductible for 2026.

- Paying the Deductible: Susan’s two medications have a combined retail cost of $75 per month. For the first several months, she pays this full amount out of her own pocket. It takes a little while, but she's chipping away at that deductible.

- Initial Coverage: About seven months into the year, she finally spends enough to meet her $545 deductible. Just like that, her plan's cost-sharing kicks in. Her copays for her generics plummet to just $5 each, meaning she now only pays $10 a month.

- The Year-End Picture: Susan’s total drug spending for the year stays far below the $5,450 limit for the coverage gap. She never even comes close to the donut hole and enjoys low, predictable costs for the rest of the year.

Susan's Takeaway: For a lot of people who only need generic drugs, this is what Part D looks like. Once you get past the deductible, your costs become very manageable for the rest of the year.

Scenario 2: Robert Managing a Chronic Condition

Robert has Type 2 diabetes and relies on several medications, including a popular and expensive brand-name GLP-1 drug. To make sure that key prescription is covered, he chose a plan with a higher $95 monthly premium and the standard $545 deductible.

- Meeting the Deductible (Instantly): Robert's brand-name drug has a staggering retail price of $900 per month. With his very first refill in January, he pays his $545 deductible in one go.

- Initial Coverage (For a While): For the next few months, Robert's out-of-pocket cost is a much more reasonable $45 copay for his main drug. But here's the catch: the total cost of the drug (what he pays plus what the plan pays) is so high that he barrels toward the $5,450 coverage limit very quickly.

- Hitting the Donut Hole: By late summer, he enters the coverage gap. His cost structure changes completely. Now, he's responsible for 25% of his drug's retail price, which works out to $225 per month ($900 x 0.25). That’s a huge jump from his old copay.

Robert’s experience is becoming more and more common. Expensive new drugs are driving up costs across the board. In fact, total gross drug spending in Part D shot up by 103.5% over the last decade, with pricey specialty drugs now making up 51% of all spending, up from 32%. You can learn more about how these trends are impacting Part D costs and what it means for beneficiaries.

Scenario 3: Maria and Her High-Cost Specialty Drug

Maria is managing rheumatoid arthritis with a specialty biologic drug that costs a jaw-dropping $5,000 per month. She knew her expenses would be high, so she carefully chose a Part D plan with a $120 monthly premium that she confirmed covers her medication.

- Deductible and Initial Coverage (Gone in a Flash): With her very first fill in January, Maria meets her $545 deductible and blows past the entire $5,450 initial coverage limit. It all happens in a single pharmacy visit.

- The Donut Hole (A Brief Stop): She immediately lands in the donut hole. For that one fill, she pays 25% of the $5,000 cost, which is $1,250.

- Catastrophic Coverage (The Safety Net): After paying her deductible and that $1,250, Maria’s out-of-pocket spending has already hit the catastrophic threshold. For the rest of the entire year, her cost for that life-changing specialty drug drops to $0.

This catastrophic protection is an absolute lifeline for people like Maria. It acts as a crucial safety net that prevents prescription costs from spiraling out of control. The complex pricing world behind these numbers often involves powerful middlemen; you can learn more by reading our guide on what a pharmacy benefit manager is.

Figuring out how Part D works is the first big step. But what really makes a difference is taking control of your expenses.

The good news? You have several powerful ways to lower your Medicare Part D costs. This isn't about finding some hidden loophole. It’s about making smart, informed choices that fit your health needs and your budget.

From financial assistance programs to a simple chat with your doctor, these strategies can make a huge dent in what you spend out-of-pocket each year. The secret is to be proactive and check out every option you have.

See if You Qualify for Extra Help

For anyone with a limited income and resources, the Extra Help program is a total game-changer. It's also known as the Low-Income Subsidy (or LIS), and it’s a federal program that helps pay for your Part D plan’s premiums, deductibles, and even your copayments. For some people, it can drop the cost of a prescription down to just a few dollars.

Getting approved for Extra Help can lift a massive financial weight off your shoulders. The program's impact has been incredible. When Part D first started, out-of-pocket drug spending for people who qualified for the subsidy fell from an average of $741 to just $160. That's a 78% drop that completely changed drug affordability for seniors who needed it most. You can read more about how Part D transformed prescription drug economics for low-income individuals.

To find out if you qualify, you can apply in a few ways:

- Directly on the Social Security Administration’s website.

- By calling Social Security to get help over the phone.

- With free assistance from your state’s Health Insurance Assistance Program (SHIP).

Pick a Plan That Actually Covers Your Meds

This sounds like a no-brainer, but it is the single most important thing you can do to control your costs. Every single Part D plan has its own formulary—which is just a fancy word for the list of drugs it covers. If a medicine you rely on isn't on a plan's formulary, you could get stuck paying 100% of the cost yourself.

Before you even think about enrolling, make a list of every prescription you take, including the exact dosages. Then, use the Medicare Plan Finder tool or let an advisor at My Policy Quote help you enter your specific medications. This will show you which plans cover your drugs and give you a solid estimate of your yearly costs with each one.

A plan with a super-low premium is a terrible deal if it doesn’t cover your most expensive prescription. Always, always check the formulary first—it's more important than the monthly premium.

Use Preferred Pharmacies and Mail-Order

Most Part D plans have a network of pharmacies they partner with. But here's a pro-tip: within that network, they usually have preferred pharmacies. When you fill your prescriptions at one of these spots, you’ll save money because your copays and coinsurance are almost always lower than at a standard, in-network pharmacy.

Lots of plans also offer mail-order pharmacy services. This can be a huge help, both for convenience and for your wallet, especially for maintenance drugs you take long-term. You can often get a 90-day supply for less than the cost of three separate 30-day refills at the drugstore, saving you time and money.

Talk to Your Doctor About Cheaper Options

Your doctor is your best ally in managing both your health and your healthcare costs. Don't be afraid to have an honest conversation with them about how much your medications are costing you. More often than not, there are less expensive alternatives that work just as well.

Here are a few key questions to ask at your next appointment:

- Is there a generic version of this brand-name drug? Generics have the exact same active ingredients and are proven to be just as safe and effective, but they can cost up to 85% less.

- Could we try a lower-cost therapeutic alternative? Sometimes, a different drug in the same family can give you the same health benefit for a fraction of the cost.

- Is there a similar medication on my plan's formulary? Your doctor might be able to switch you to a drug that your plan covers with a much smaller copay.

That one simple conversation empowers both of you to find a treatment that keeps you healthy without breaking the bank.

Frequently Asked Questions About Part D Costs

Diving into the world of Medicare Part D can leave anyone with a few lingering questions. Even when you’ve got the basics down, some situations can still feel tricky. Let’s clear up some of the most common uncertainties people have about the cost of Medicare Part D.

Think of this as a quick-reference guide to help you plan with confidence and sidestep those common pitfalls.

Can My Part D Premium Change Unexpectedly?

It’s a fair question. You find a plan with a great monthly premium, but then you start to worry: will it suddenly jump halfway through the year?

The good news is, your premium is locked in for the entire plan year, which runs from January 1st to December 31st. Your insurance company can't just raise your premium in the middle of the year.

However, they do re-evaluate their costs every year. That means your premium, deductible, and copays can—and often do—change for the following year. This is exactly why the Annual Enrollment Period each fall is so important. It’s your dedicated time to review your plan’s upcoming changes and switch to a new one if it no longer fits your budget or health needs.

What if I Don’t Need Prescriptions Right Now?

If you’re healthy and don’t take any regular medications, it’s incredibly tempting to skip enrolling in Part D and save that monthly premium. Honestly, this is one of the most common and costly mistakes you can make.

Waiting to sign up will almost certainly trigger the permanent Late Enrollment Penalty. The penalty is calculated as 1% of the national base beneficiary premium for every single month you were eligible but didn’t have coverage. That amount gets tacked onto your monthly premium for as long as you have a Part D plan.

Enrolling on time, even if you don't think you need it, is a crucial insurance policy against future penalties and sudden health issues.

Think of it like car insurance. You pay for it every month hoping you never have to use it, but you're so glad it's there if you do. Part D works the same way—it’s there to shield you from crushing costs when you need it most.

How Has The Donut Hole Changed?

The term "donut hole" used to strike fear into the hearts of anyone on Medicare, because it meant you were suddenly responsible for paying 100% of your drug costs. Thankfully, that has changed in a big way.

Today, the coverage gap is much, much more manageable.

When you're in the donut hole, your out-of-pocket costs are capped. You'll pay no more than 25% of the retail price for both brand-name and generic drugs, which provides a much stronger safety net. Even better, new rules starting in 2025 will cap your total out-of-pocket drug spending for the year. Once you hit that annual limit, your costs for all covered drugs will drop to $0.

Of course, Part D is just one piece of the puzzle. You might also have questions about how to pay for hospice care or other services. Understanding the full picture helps you plan your healthcare finances more effectively.

Is a Plan with a Higher Premium Always Better?

This is a persistent myth that can lead people to overspend. It’s easy to assume that a higher monthly premium automatically buys you better coverage, but that’s not always true. The "best" plan has nothing to do with a high price tag and everything to do with how well it lines up with your specific needs.

Here’s why a pricier plan isn't always the right fit:

- Formulary Mismatches: An expensive plan might not even cover the specific medications you take, leaving you to pay the full price anyway.

- Cost-Sharing Differences: A lower-premium plan could actually offer better copays for your drugs, saving you more money in the long run.

- Network Restrictions: The "better" plan might not include your favorite local pharmacy in its network, creating a hassle and potentially higher costs.

The smartest way to choose a plan is to look at the total estimated annual cost—not just the monthly premium. That means adding up the premium, the deductible, and your projected copays based on your exact list of prescriptions. This is the only way to find a plan that is truly cost-effective for you.

Finding the right Part D plan means balancing premiums, deductibles, and formularies to match what you actually need. At My Policy Quote, we specialize in making this simple. We help you compare every option to find coverage that provides real value and peace of mind. Let us help you make a confident choice by visiting https://mypolicyquote.com today.