You’ve probably heard the term "donut hole" when people talk about Medicare, and it usually comes with a story about surprise medical bills. For years, it was a source of real anxiety for anyone relying on a Part D prescription drug plan.

But what was it, really? And does it still exist? Let’s clear things up.

What Was the Medicare "Donut Hole"?

Think of it like a temporary gap in your prescription drug coverage. In the beginning of the year, your plan worked as expected, covering its share of your medication costs. But once you and your plan spent a certain amount, you’d suddenly fall into the “donut hole.”

Once you were in this gap, your out-of-pocket costs would jump dramatically. It was a stressful time for many, especially those with chronic conditions who depended on expensive, life-saving drugs. You were left paying a much higher percentage of the cost until you spent enough to climb out the other side and reach what’s called catastrophic coverage.

Closing the Gap for Good

This gap was a big problem. It forced people to choose between their health and their budget, and for a long time, it felt like a system that punished you for needing your medication.

Thankfully, that’s all in the past. Major healthcare reforms have slowly been closing this gap, and as of 2025, the donut hole is officially a thing of the past.

Now, instead of falling into a coverage gap, you’re protected by a hard cap on your spending. The new rules establish an annual out-of-pocket maximum of $2,000 for your covered prescriptions. Once you hit that limit, you won't pay anything more for your covered drugs for the rest of the year.

This is a game-changer. It replaces a confusing, stressful system with a simple, predictable safety net. You can learn more about how this simplifies your retirement planning in our complete Medicare planning guide.

This change is one of the most important improvements to Medicare Part D ever. It means millions of Americans no longer have to worry about their drug costs spiraling out of control halfway through the year.

Understanding this history helps you appreciate the stability of today’s Medicare. The donut hole is gone, and in its place is a straightforward system designed to protect you from financial hardship. Now, you can plan your year with confidence, knowing there’s a firm ceiling on what you’ll have to spend.

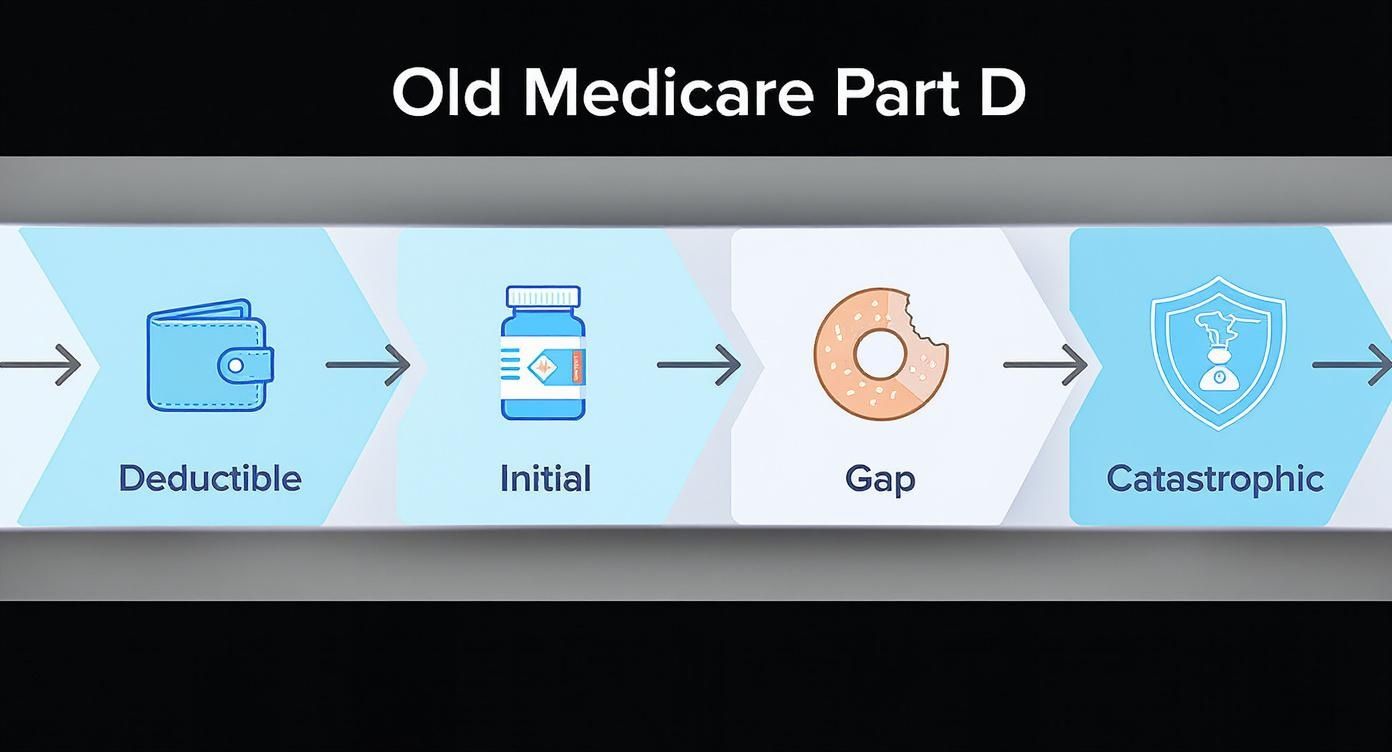

How The Old Part D Coverage Phases Worked

To really appreciate the peace of mind that today’s Medicare Part D offers, it helps to look back at the financial roller coaster it replaced. For years, beneficiaries had to navigate a complicated four-phase system that often felt unpredictable and, frankly, stressful.

Think of it like a long road trip. You'd start on a smooth, easy stretch, suddenly hit a steep and expensive toll road, and then, finally, find your way to an open highway. It was a bumpy ride.

The First Step: The Deductible Phase

Every year, the journey started with the Deductible Phase. This was simple: you were responsible for 100% of your prescription drug costs until you hit your plan's annual deductible.

The exact amount varied from plan to plan, but Medicare set a maximum each year. During this stage, you paid the full retail price for your medications right out of your own pocket. Once you spent enough to meet that deductible, you could move on to the next phase.

The Second Step: The Initial Coverage Phase

After hitting your deductible, you entered the Initial Coverage Phase. This part of the journey felt much more comfortable because you and your insurance plan started sharing the costs.

You’d only pay a small copayment or coinsurance for each prescription, while your plan handled the rest. This teamwork continued as long as the total spending—what you paid plus what your plan paid—stayed under a certain limit. In 2024, for example, that limit was $5,030. Crossing that threshold meant you were about to enter the dreaded donut hole.

The Third Step: The Coverage Gap, a.k.a. The Donut Hole

This is where the road got rough. Entering the Coverage Gap, better known as the donut hole, meant your out-of-pocket costs would suddenly shoot up. In the final years before the donut hole was closed, you were on the hook for 25% of the cost for both your brand-name and generic drugs.

For people with chronic conditions or expensive medications, this was a massive financial shock. It created a high-stakes coverage cliff that impacted millions of people every year. The anxiety it caused was very real. In fact, one insightful report from The Commonwealth Fund highlighted just how this financial burden affected nearly 7 million Americans.

The Fourth Step: The Catastrophic Coverage Phase

Finally, after paying enough out-of-pocket to climb out of the donut hole, you reached the last stage: Catastrophic Coverage. This was designed to be a safety net, protecting you from sky-high prescription costs for the rest of the year.

Once you hit this phase, your expenses dropped dramatically. You’d only have to pay a small coinsurance or copay for your medications. While this was a huge relief, the journey to get there was often financially draining, which really showed the flaws in the old system. The logic behind how plans cover these phases has some things in common with figuring out what is creditable coverage when you're moving from one type of insurance to another.

Before the recent changes, this four-phase model was the reality for millions. The table below gives a quick snapshot of how that old system worked.

A Look at the Previous Medicare Part D Coverage Phases

This table illustrates the four distinct phases of prescription drug coverage under the former Medicare Part D model, showing how a beneficiary's costs changed as their spending increased throughout the year.

| Coverage Phase | What You Paid | Example Spending Threshold |

|---|---|---|

| Deductible | 100% of your drug costs | Up to your plan's annual deductible |

| Initial Coverage | A small copay or coinsurance | Until total drug costs reached $5,030 (2024) |

| Coverage Gap (Donut Hole) | 25% of brand-name & generic drug costs | From $5,030 until your out-of-pocket spending hit a set limit |

| Catastrophic Coverage | A very small copay or coinsurance | For the rest of the year |

The Old System in a Nutshell: The previous four-phase model created a "spending cliff" where your costs could suddenly spike. This made it incredibly difficult and stressful to budget for essential medications.

Looking at this old roadmap makes it clear why the new system is such a welcome change. By getting rid of the donut hole and putting a firm cap on spending, Medicare has finally smoothed out the financial journey, giving beneficiaries the predictability and security they deserve.

The End of the Medicare Donut Hole

For years, anyone with Medicare Part D knew the feeling of dread that came with the "donut hole." It was a source of anxiety, a financial cliff you hoped to avoid but often couldn't.

But that story is finally over. A huge change in Medicare has officially closed the donut hole for good, bringing a new level of predictability and relief to millions of Americans.

This isn't just a minor adjustment; it's a complete redesign. The old, confusing four-phase system is gone, replaced by something much simpler. At the heart of it all is a powerful new protection: a hard limit on what you'll ever have to pay for your prescriptions each year.

The $2,000 Spending Cap: Your New Safety Net

The biggest and best part of this change is the new $2,000 maximum out-of-pocket (MOOP) limit. Think of it as a financial safety net. No matter how high the cost of your medications, you will never pay more than this amount in a single year.

Once your personal spending on covered drugs—which includes what you pay for your deductible, copayments, and coinsurance—hits that $2,000 mark, you're done. For the rest of the calendar year, you will pay $0 for all your covered prescriptions.

This cap transforms budgeting for your medications. It's no longer a stressful guessing game. It’s a clear, predictable plan.

This is such a big deal that it’s changing how insurance companies design their plans. In fact, data from the Centers for Medicare & Medicaid Services shows that the average monthly bids for 2025 Part D plans have gone up. While that might sound a little scary, it's mostly a reflection of a behind-the-scenes shift as the government and insurers adjust to this new, much more friendly system for beneficiaries. You can read more about these CMS findings on the 2025 plan changes.

From Four Confusing Phases to Three Simple Ones

Remember the old system? It was a four-part maze: the deductible, initial coverage, the dreaded donut hole, and then finally, catastrophic coverage. This infographic is a good reminder of the confusing and costly path people used to navigate.

Those spending cliffs were what made the donut hole so stressful for so many people. Thankfully, the new model is streamlined into just three straightforward phases.

Here’s how the simpler new structure works:

- The Deductible Phase: You start the year paying for your prescriptions until you meet your plan's deductible. Simple enough.

- The Initial Coverage Phase: After the deductible is met, you and your plan share the costs. You'll just pay your normal copay or coinsurance.

- The Catastrophic Phase: Once your total out-of-pocket spending gets to the $2,000 cap, you’re in the clear. You’ll pay nothing more for covered drugs for the rest of the year.

That’s it. The infamous coverage gap—the donut hole itself—has been completely eliminated. No more sudden spikes in what you owe.

Getting rid of the donut hole and putting in a $2,000 annual cap are the most important improvements to Medicare Part D in more than a decade. It gives people a level of financial certainty that just didn't exist before.

This newfound security is a true game-changer, especially if you manage a chronic condition that requires expensive medications. Instead of worrying about your costs jumping halfway through the year, you can now budget with confidence. You know exactly where the ceiling is, turning a once-risky journey into a clear and manageable path.

Smarter Ways to Manage Your Drug Costs

With the old insurance donut hole gone and a new $2,000 spending cap in its place, the way you think about your medication costs needs a refresh. The game has changed for the better, but being strategic is still the key to keeping your out-of-pocket expenses as low as possible.

Proactive management can help you stay under that annual cap for longer—or even avoid hitting it altogether. Your most powerful tool is knowledge. When you understand your Part D plan inside and out, you can make informed choices that save you real money. It’s all about working smarter within this new, more predictable system.

Review Your Plan Formulary Every Year

This is the single most important thing you can do. Every year during Open Enrollment, you need to sit down and review your plan's formulary—which is just a fancy word for the list of prescription drugs your plan agrees to cover.

That list is not set in stone. In fact, it often changes from one year to the next.

A drug that’s affordable this year might be moved to a more expensive tier or even dropped completely next year. Assuming your coverage will stay the same is a costly mistake. During Open Enrollment, take the time to:

- Confirm your current medications are still covered. Make a list and check it against the new formulary for any plan you're considering.

- Check the drug tiers. See if any of your medications have been moved to a higher, more expensive tier. This will directly increase your copay.

- Look for new restrictions. Plans can add new hurdles like "prior authorization" or "step therapy" for certain drugs.

A yearly plan review is your best defense against surprise cost increases. It makes sure your plan still fits your health needs, preventing a nasty shock at the pharmacy counter.

Choose Generic Drugs Whenever Possible

When it comes to cost, the debate between generic and brand-name drugs has a clear winner. Generic medications are chemically identical to their brand-name counterparts. They have the same dosage, safety, and effectiveness, but they cost a fraction of the price. The FDA holds them to the same strict quality standards.

Choosing a generic directly lowers what you pay for each prescription. This simple move helps you progress much more slowly toward that $2,000 annual cap, saving the safety net for when you truly need it. Always ask your doctor or pharmacist if there's a generic alternative that’s right for you.

Understand Your Plan's Tiered Formulary

Most Part D plans use a tier system to set drug prices, and getting to know this structure is crucial for managing your budget. While the exact details can vary, a typical formulary looks something like this:

| Drug Tier | Description | Your Cost |

|---|---|---|

| Tier 1 | Preferred Generic Drugs | Lowest Copayment |

| Tier 2 | Non-Preferred Generic Drugs | Low Copayment |

| Tier 3 | Preferred Brand-Name Drugs | Medium Copayment |

| Tier 4 | Non-Preferred Brand-Name Drugs | Higher Copayment/Coinsurance |

| Tier 5 | Specialty Drugs | Highest Cost-Sharing |

It’s pretty clear—drugs in the lower tiers cost you a lot less out of your own pocket.

Whenever your doctor prescribes a new medication, ask if there are effective options in a lower tier on your plan's list. For federal retirees, managing these costs often involves coordinating Medicare with their existing federal retirement health benefits, including Medicare options. This coordinated approach can help optimize your choices within a tiered system, making sure you get the most affordable and effective treatments available. Sticking to lower-tiered drugs is a simple and powerful way to control your annual spending.

Finding Help for High Prescription Expenses

Even with the new $2,000 spending cap in place of the old donut hole, that number can still feel daunting. For many people on a fixed income, hitting that limit is a real financial strain.

But here’s the good news: you don’t have to carry that burden alone. There are some incredibly helpful programs out there designed to give you a lifeline when you need it most. Knowing where to look is the first step toward getting your medication costs under control and finding some much-needed peace of mind.

Medicare Extra Help Program

One of the most powerful resources available is the Medicare Extra Help program, which you might also hear called the Low-Income Subsidy (LIS). This is a federal program created specifically to help people with limited income and resources afford their Medicare Part D prescription drugs.

If you qualify, the support is significant. Extra Help can cover your monthly Part D premiums, your yearly deductible, and the copayments you’re asked to pay at the pharmacy counter. For some folks, it brings the cost of each prescription down to just a few dollars.

So, who gets this assistance? People often qualify automatically if they:

- Are enrolled in Medicaid.

- Receive help from their state to pay for Medicare Part B premiums.

- Get Supplemental Security Income (SSI) benefits.

But even if you don't fall into one of those groups, you might still be eligible based on your income and resources. It never hurts to apply on the Social Security Administration’s website—it could unlock a huge amount of savings.

State and Manufacturer Assistance Programs

Beyond the big federal program, there are other layers of support you can tap into. These come from both state governments and the drug companies themselves.

Many states have their own State Pharmaceutical Assistance Programs (SPAPs). Think of these as a local boost to your Medicare Part D plan. They step in to provide another layer of financial help, but since each state runs its own program, the eligibility rules can be different. The best place to start is your state's Department of Aging or Health.

On top of that, most drug manufacturers offer Patient Assistance Programs (PAPs). These are run by the pharmaceutical companies and often provide their brand-name drugs for free or at a very low cost to people who can't afford them. If you take an expensive brand-name medication, a quick search on the manufacturer's website for their PAP could save you a fortune.

It might feel like a bit of homework to look into all these programs, but the payoff can be life-changing. When you stack federal, state, and manufacturer aid together, you can sometimes bring your out-of-pocket drug costs down to almost nothing.

Smart Strategies Like Mail-Order Pharmacies

Sometimes, saving money is less about finding a program and more about changing your routine. Using a mail-order pharmacy through your Part D plan is a perfect example of a small change that leads to big savings.

Most plans offer a 90-day supply of your long-term medications for a lower price than you'd pay for three separate 30-day refills at your local drugstore. It's a win-win: you save money on copayments and make fewer trips to the pharmacy. If you take medicine for a chronic condition like high blood pressure or diabetes, this is a no-brainer.

Of course, dealing with insurance isn't always straightforward. If your plan ever denies coverage for a drug or you think you're being charged too much, remember you have rights. You can always challenge a plan’s decision, and our guide on the Medicare appeals process can walk you through the steps.

To help you see all these options in one place, here’s a quick comparison of the different ways you can get help with your prescription costs.

Comparing Prescription Drug Cost-Assistance Programs

Here’s a summary of different programs and strategies available to Medicare beneficiaries to help reduce out-of-pocket prescription drug costs.

| Program or Strategy | Who It Is For | How It Helps You Save |

|---|---|---|

| Medicare Extra Help (LIS) | Beneficiaries with limited income and resources. | Helps pay for Part D premiums, deductibles, and copayments, often reducing drug costs to just a few dollars. |

| State Pharmaceutical Assistance (SPAPs) | Eligible residents of specific states; requirements vary. | Provides an additional layer of financial aid on top of your Part D plan, helping to cover remaining costs. |

| Patient Assistance Programs (PAPs) | Individuals who cannot afford specific brand-name drugs. | Offers free or significantly discounted medications directly from the drug manufacturer. |

| Mail-Order Pharmacies | Anyone taking long-term or maintenance medications. | Provides a 90-day supply of drugs for a lower copay than three 30-day refills, reducing annual costs. |

Your Action Plan for Medicare Part D

Managing your Medicare Part D coverage just got a whole lot simpler. With the old, dreaded donut hole officially gone, your focus can finally shift from worrying about a sudden coverage gap to proactively managing your plan to get the most out of it.

This change is about more than just policy—it's about empowerment. It gives you the confidence to take back control of your prescription drug costs. The strategy is straightforward, and it all boils down to a few key ideas that will help you keep your healthcare budget predictable and your mind at ease.

Key Takeaways for Success

Think of these as your new golden rules for navigating Part D. Stick to them, and you’ll be in great shape all year long.

- Embrace the New Predictability. The single biggest game-changer is the $2,000 annual spending cap. This is your ultimate safety net, making sure your out-of-pocket drug costs never spiral out of control.

- Make Annual Reviews Non-Negotiable. Insurance plans aren't set in stone. Formularies (the list of covered drugs), premiums, and pharmacy networks can change every single year. Use the Open Enrollment period to double-check that your plan still fits your health needs and your wallet.

- Always Explore Financial Assistance. Even with the new cap, medication costs can add up. Never be afraid to see if you qualify for programs like Medicare Extra Help or a State Pharmaceutical Assistance Program. These exist to help you.

The most powerful tool you have is your annual plan review. A plan that was perfect last year might be a poor fit this year due to changes in its formulary or your medication needs.

Beyond mastering your Medicare Part D plan, having a good grasp of how to file an insurance claim effectively can also be a huge help. It gives you another layer of confidence in managing your healthcare finances. By staying informed and proactive, you put yourself in the best possible position to protect both your health and your savings.

Clearing Up Questions About the Donut Hole

Even with these big updates, it’s normal to have questions. The old donut hole system was confusing, so let's walk through the most common questions to make sure you feel totally clear about your coverage.

Is the Medicare Donut Hole Really Gone for Good?

Yes, the old "donut hole" coverage gap is officially gone as of 2025. It's been replaced with a much simpler and safer system: a $2,000 annual cap on what you pay out-of-pocket for your prescription drugs.

Once you hit that $2,000 limit, your costs drop to $0 for all your covered medications for the rest of the year. While you might still hear people use the old term, the financial cliff it once represented has been completely removed.

What Actually Counts Toward That New Spending Cap?

This is a great question, because knowing what counts is key to tracking your costs. The $2,000 spending cap is all about what you personally pay for your prescriptions.

Here’s exactly what adds up toward your limit:

- Your annual deductible: The amount you have to pay first before your plan starts covering costs.

- Your copayments: Those fixed dollar amounts you pay for each prescription fill.

- Your coinsurance: The percentage of a drug's cost that you're responsible for.

It's also super important to know what doesn't count. Your monthly plan premiums and anything you pay for drugs that aren't on your plan's approved list (its formulary) won't help you reach the cap.

Should I Bother Comparing Part D Plans Every Year?

Absolutely. In fact, it’s more important now than ever. Think of the $2,000 cap as a safety net that every plan has, but how you get there—and how much you spend along the way—can be wildly different from one plan to the next.

A plan’s formulary (the list of drugs it covers) isn't set in stone. A medicine that’s cheap for you this year could be moved to a higher-cost tier—or dropped entirely—next year.

Every plan still sets its own monthly premiums, deductibles, and drug list. A quick yearly review during Open Enrollment is your best defense against surprise costs at the pharmacy. It ensures you’ve got the right plan for your specific medications.

For even more answers, feel free to check out our complete FAQ about Medicare for other useful insights.

At My Policy Quote, our job is to help you feel confident navigating these changes. We can help you find the right plan that fits your health needs and your budget in this new Medicare landscape. https://mypolicyquote.com