When you hear the term “deductible,” you probably think of a simple, one-time annual payment. Pay it once in January, and you're set for the year. But with Medicare, things work a little differently.

The Medicare Part A deductible is the amount you pay out of your own pocket for hospital care before Medicare starts chipping in. But here’s the twist: it doesn’t reset every calendar year. Instead, it applies to each unique "benefit period," which means you could end up paying it more than once a year.

What Is the Medicare Part A Deductible, Anyway?

Let’s cut through the jargon. Think of it like the deductible on your car insurance. If you get into an accident, you have to pay that first chunk of the repair bill yourself before your insurance company takes over.

The Part A deductible works the same way for your hospital coverage. It's the fixed amount you’re responsible for when you’re admitted as an inpatient. For 2026, that amount is $1,736. Once you’ve paid it, Medicare steps in to share the costs for the rest of your hospital stay.

Basically, it's the key that unlocks your Part A benefits for that specific hospital visit.

To make this even clearer, here's a quick summary of how the Part A deductible works for a hospital stay.

Medicare Part A Deductible at a Glance

| Aspect | Explanation |

|---|---|

| Deductible Amount (2026) | You pay the first $1,736 of your inpatient hospital costs. |

| When It Applies | It applies at the start of each new "benefit period." |

| Frequency | This is not an annual deductible; you could pay it more than once per year. |

| What It Unlocks | After paying, Medicare covers days 1-60 of your hospital stay in full. |

Once you understand these key points, you can start to see how important it is to plan for this potential cost.

The Benefit Period: A Crucial Concept

This is the part that trips most people up. The Medicare Part A deductible is not an annual deductible. You don't just pay it once and forget about it for the year. It's tied to something called a benefit period.

A benefit period kicks off the very day you're admitted to a hospital. It only ends after you’ve been out of the hospital (or a skilled nursing facility) for 60 consecutive days.

If you have to go back to the hospital after that 60-day break, a new benefit period starts. And yes, that means you have to pay the Part A deductible all over again. This unique structure is a huge part of smart financial planning, something we dive deeper into in our complete Medicare planning guide.

In simple terms: The deductible is like your entry fee for hospital coverage for a specific illness. If you get better and then have a completely separate hospital stay later on, you might have to pay that entry fee again.

What Services Does It Cover?

The Part A deductible is strictly for inpatient care—the services you get when you are formally admitted to a facility.

- Inpatient Hospital Stays: This includes your semi-private room, meals, nursing care, and medications given as part of your treatment in the hospital.

- Skilled Nursing Facility (SNF) Care: It also applies to care in a SNF, but only if you’ve had a qualifying hospital stay first.

It does not cover outpatient services. Things like regular doctor’s visits, lab work, or preventive screenings fall under Medicare Part B, which has its own separate deductible. Getting this distinction right is key to understanding what costs you might be on the hook for.

How Benefit Periods Define Your Deductible Costs

If there's one thing that trips people up about the Medicare Part A deductible, it's this: it doesn't follow a calendar. Forget January 1st. Unlike your car insurance or other health plans that reset with the new year, Medicare marches to the beat of its own drum.

This is where you need to get familiar with a little something called a benefit period.

Think of a benefit period as a self-contained "episode of care." It’s the timeline that dictates when your deductible is due and how long your hospital coverage lasts. Nailing this concept is the absolute key to understanding what you might actually owe.

What Kicks Off a New Benefit Period?

A benefit period officially starts the day you're admitted to a hospital as an inpatient. The moment you're checked in, the clock starts ticking and that Part A deductible becomes your responsibility.

Once you pay it, Medicare steps in to cover its share for the first 60 days of your hospital stay. But when does the benefit period end? This is the important part: it only ends after you’ve been out of the hospital (or a skilled nursing facility) for 60 consecutive days.

That 60-day gap is the magic reset button. If you're readmitted to the hospital after being out for 60 days straight, you’ve started a brand-new benefit period. And that means you'll have to pay the deductible all over again.

Key Takeaway: The Medicare Part A deductible isn't an annual fee you pay once and forget. It's a cost tied to each distinct inpatient episode, which is defined by a benefit period. One long stay might mean one deductible, while several shorter stays could mean paying it multiple times.

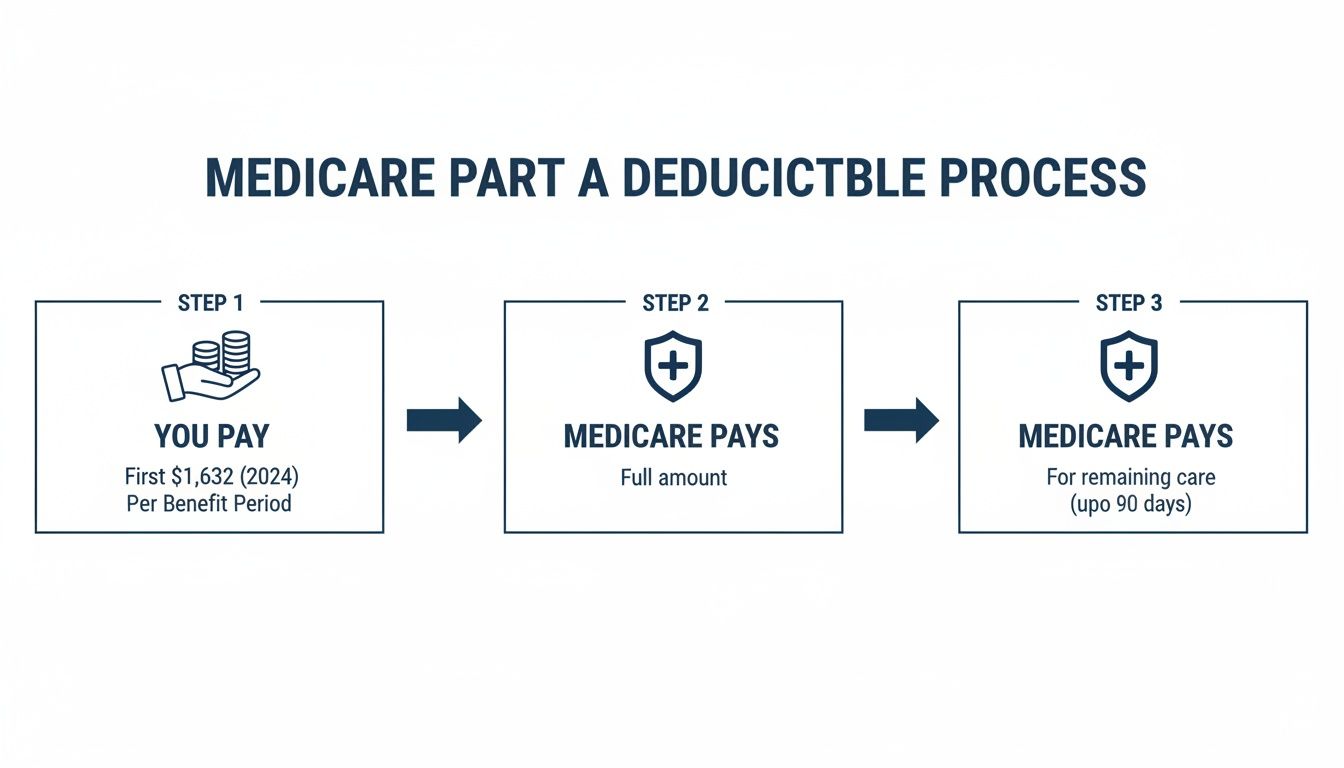

This chart breaks down how the payment process flows between you and Medicare.

As you can see, you paying your deductible is the trigger that unlocks Medicare's coverage for your hospital stay.

Real-World Scenarios: Putting the Benefit Period to the Test

Rules on paper can feel a bit abstract, so let's walk through a few real-life examples to see how this plays out. We'll use the 2026 Part A deductible of $1,736 to keep things simple.

Example 1: One Long Hospital Stay

- The Situation: David is admitted to the hospital on February 1st for heart surgery. His recovery is tough, and he ends up staying for 75 days, finally going home on April 16th.

- His Deductible Cost: David pays the $1,736 deductible just one time.

- Why? His entire 75-day stay happened within a single benefit period. After he paid that initial deductible, Medicare covered the first 60 days. He'll owe a daily coinsurance for days 61-75, but he won't get hit with another deductible.

Example 2: Two Separate Hospital Stays in One Year

- The Situation: Maria goes to the hospital for pneumonia on March 10th and is discharged five days later. She pays her Part A deductible. In July—well over 60 days later—she falls and breaks her hip, requiring another hospital stay.

- Her Deductible Cost: Maria pays the $1,736 deductible twice in the same year, totaling $3,472.

- Why? More than 60 consecutive days passed between her first discharge and her second admission. That gap officially ended her first benefit period, so her second hospital stay started a completely new one.

Example 3: A Quick Readmission

- The Situation: John is hospitalized for a bad infection on May 5th. He pays his deductible and is sent home on May 10th. Unfortunately, he has a relapse and is readmitted just 20 days later.

- His Deductible Cost: John pays the $1,736 deductible only once.

- Why? Because he was readmitted within that 60-day window, he was technically still in his original benefit period. His deductible was already covered for that episode of care.

Getting these distinctions right is everything. It shows how one person might pay the deductible just once a year, while someone else could face it two or three times depending on their specific health journey.

The Rising Cost of the Part A Deductible Over Time

To really wrap your head around the Medicare Part A deductible, you have to look back at where it started. This isn't just a history lesson in numbers; it's the story of how dramatically healthcare costs have ballooned over the decades. What began as a pretty small expense has morphed into a major out-of-pocket hit for millions of Americans.

When Medicare first rolled out, the medical world was a completely different place. Costs were way lower, and the first-ever deductible was just a minor, predictable hurdle for people. But as medical technology took off and healthcare spending skyrocketed, that deductible started its slow, steady climb, year after year.

This relentless growth has completely changed the game for retirees. Today, relying only on Original Medicare for a hospital stay is a much bigger gamble than it was for our parents' or grandparents' generation. Understanding this trend is key to planning a financially sound retirement.

From Minor Cost to Major Concern

The journey of the Part A deductible is pretty shocking when you see it laid out. When the program kicked off back in 1966, you were on the hook for a tiny $40 deductible for a hospital stay. That amount felt more like a simple copay than something that could derail your budget.

Flash forward to today, and the picture couldn't be more different. That small initial cost is a distant memory. By 2023, the deductible had exploded to $1,600 for each hospital benefit period. It kept climbing to $1,676 in 2025 and is set to hit $1,736 in 2026.

That’s a mind-boggling 4,240% increase in about 60 years. It’s a crystal-clear sign of how much the cost of hospital care has reshaped what Medicare beneficiaries have to pay.

This isn't just simple inflation doing its thing; it's a direct reflection of the soaring price of inpatient medical services.

This dramatic increase underscores a critical point: The Part A deductible is not a static figure. It is actively managed and adjusted to keep pace with rising hospital costs, meaning you can expect it to continue growing in the years ahead.

The Year-Over-Year Trend

This isn't just something that happened in the past—it’s an ongoing reality. Every single year, the Centers for Medicare & Medicaid Services (CMS) reevaluates the numbers and adjusts the deductible to reflect the most current hospital cost data.

Just look at the recent trend to see how quickly it moves:

- 2024: The deductible was $1,632.

- 2025: It jumped to $1,676, a $44 increase.

- 2026: It’s scheduled to rise again to $1,736, another $60 jump.

These bumps might not seem huge on their own, but they add up fast and create real financial uncertainty. This is especially true if you end up having more than one benefit period in a single year, since you have to pay that deductible all over again each time. Our guide on the Medicare deductible for 2024 gives you more context on how these annual changes work.

This whole historical trend is exactly why so many people choose to get extra coverage beyond Original Medicare. The ever-growing Part A deductible is one of the main reasons Medigap and Medicare Advantage plans are so popular—they’re built to protect you from these unpredictable and rising costs.

What You Pay After The Deductible Is Met

Meeting your Medicare Part A deductible is the first hurdle, but it doesn't mean your hospital costs are over. Think of it as opening the gate. Once you're inside, a clear timeline of cost-sharing begins, especially if your hospital stay gets longer than expected.

Understanding this structure is key to avoiding serious financial surprises. The deductible gets you through the first 60 days of an inpatient stay, but after that, a new set of costs—known as coinsurance—kicks in.

Unpacking Your Inpatient Hospital Coinsurance

For the first 60 days you're in the hospital as an inpatient (within a single benefit period), Medicare Part A covers 100% of your eligible costs once you've paid that initial deductible. During this time, you pay nothing more for your room, meals, or nursing care.

But if your stay stretches past that 60-day mark, you start sharing the bill with Medicare. This is where daily coinsurance payments begin. These are fixed, per-day amounts you'll owe out of your own pocket.

For 2026, here’s how your daily costs break down:

- Days 1–60: You pay $0 after meeting your Part A deductible.

- Days 61–90: You are responsible for a daily coinsurance of $434.

- Days 91 and beyond: Your responsibility doubles to $868 per day.

These daily charges can add up alarmingly fast, turning a long hospital stay into a major financial event. For example, a 90-day stay would leave you with a $13,020 coinsurance bill on top of the deductible you already paid.

Your Lifetime Reserve Days Explained

So, what happens if you need to be in the hospital for more than 90 days in one benefit period? Medicare does offer a safety net, but it's a limited one. You get a total of 60 lifetime reserve days that you can use over your entire life.

Think of them as a one-time bank of extra coverage days for exceptionally long hospital stays. Once you use a lifetime reserve day, it’s gone for good—it doesn't reset when a new benefit period starts.

The coinsurance for these lifetime reserve days is much higher. In 2026, you'll pay $868 per day for each reserve day you use. That’s double the rate for days 61-90, and it really shows how the costs escalate the longer you need inpatient care.

If you run out of all 60 lifetime reserve days, you are on the hook for all costs for the rest of that hospital stay. At that point, your financial exposure under Original Medicare alone is completely unlimited.

A Clear View Of Your Financial Responsibility

To give you a clearer picture of how these costs stack up, the table below maps out what you would pay at each stage of a long inpatient hospital stay.

Medicare Part A Cost-Sharing for Inpatient Stays

This table shows what you pay for an inpatient hospital stay after meeting your Part A deductible within a benefit period.

| Days of Stay | Beneficiary Pays (2026 Rates) |

|---|---|

| Days 1–60 | $0 (after the $1,736 deductible is paid) |

| Days 61–90 | $434 per day |

| Days 91+ (Using Lifetime Reserve Days) | $868 per day (for up to 60 days) |

| Beyond Lifetime Reserve Days | 100% of all costs |

This structure makes it clear: while the Part A deductible is the initial hurdle, the real financial danger lies in the daily coinsurance for longer hospital stays.

These escalating daily costs are exactly why so many people turn to supplemental insurance plans to fill these potentially devastating gaps. Without that extra protection, a severe illness or injury could easily lead to overwhelming medical debt. Planning for these "what-if" scenarios is a critical part of building a secure retirement.

How to Cover Your Part A Deductible

Let’s be honest: seeing a huge, unexpected hospital bill is enough to make anyone’s stomach drop. The Medicare Part A deductible is exactly that kind of expense—a big one that can pop up without any warning.

The good news? You don’t have to face that cost on your own. There are smart, effective ways to protect yourself and get some much-needed peace of mind. The trick is to be proactive. Instead of just reacting to a bill after you’ve already been in the hospital, you can set up a plan that handles the deductible for you. This turns a potential financial shock into a predictable, manageable expense.

Medigap Plans: Your First Line of Defense

For most people, the simplest and most direct solution is a Medicare Supplement Insurance plan, better known as Medigap. Private insurance companies sell these plans, and they’re designed to do exactly what their name says: fill in the financial "gaps" in Original Medicare, like deductibles and coinsurance.

Nearly all Medigap plans cover the Part A deductible in full. This means if you have one of these plans and you’re admitted to the hospital, your Medigap policy pays that big initial bill for you. It’s that simple.

The Power of Medigap: With the right plan, a hospital stay doesn't start with a massive out-of-pocket payment. Your Medigap policy steps in and handles that first hurdle, so you can focus on getting better—not on the bill.

This strategy gives you incredible predictability. You pay a monthly premium for your Medigap plan, and in return, you wipe out the risk of facing that hospital deductible, which could hit you more than once a year. Understanding how these policies work is a great first step. You can dive deeper in our complete guide on what a Medicare Supplement plan is.

How Medicare Advantage Plans Handle Hospital Bills

Another popular route is enrolling in a Medicare Advantage (Part C) plan. These plans are a different way to get your Medicare benefits. They bundle everything—Part A, Part B, and often prescription drug coverage (Part D)—into a single plan managed by a private insurer.

Medicare Advantage plans work differently when it comes to hospital costs. Instead of the standard Part A deductible for each benefit period, they have their own cost structure, which usually involves a fixed daily copayment for the first few days of a hospital stay.

For instance, a plan might have you pay:

- $400 per day for the first five days you're in the hospital.

- $0 per day from day six onward.

In that case, your maximum out-of-pocket cost for that hospital stay is $2,000 (5 days x $400). Every plan has its own rules, so it's absolutely critical to check the "Summary of Benefits" to see the specific hospital copayments before you enroll.

Help for Those with Limited Incomes

For people with limited income and resources, that Part A deductible can feel like an impossible hurdle. Thankfully, help is available.

The main program is Medicaid. If you qualify for both Medicare and Medicaid (often called being "dual-eligible"), Medicaid can step in to pay for your Medicare premiums, deductibles, and other costs. This means Medicaid would likely cover your Part A deductible completely.

There are also Medicare Savings Programs (MSPs) for people who might not qualify for full Medicaid but still need some help. One of these, the Qualified Medicare Beneficiary (QMB) program, helps pay for Part A and Part B costs, including the deductibles.

These programs are more important than ever. The Part A hospital deductible has been climbing steadily, jumping from $1,288 in 2016 to $1,632 in 2024. If you’re worried about affording your out-of-pocket costs, looking into your eligibility for these programs is a smart move.

Frequently Asked Questions About the Part A Deductible

Even after we've gone through the numbers and the rules, some questions always seem to pop up about the Medicare Part A deductible. Let's treat this section like a final check-in to clear up any lingering confusion so you can feel confident about how your hospital costs work.

We'll tackle the most common questions we hear every day from people just like you.

Do I Pay the Part A Deductible with a Medicare Advantage Plan?

This is a great question because it gets right to the core of how different Medicare paths work. The short answer is no. If you're enrolled in a Medicare Advantage (Part C) plan, you won't pay the traditional Part A deductible.

Instead, Medicare Advantage plans have their own cost structure. For a hospital stay, you’ll typically pay a set amount—a copayment—for each of the first few days you’re admitted.

For example, your plan might look something like this:

- A copay of $425 per day for days one through five of your hospital stay.

- $0 for every day after that during that same admission.

In that scenario, your total out-of-pocket cost for that hospital stay would be capped at $2,125 (5 days x $425). This could be more or less than the standard Part A deductible, all depending on your plan’s design and how long you stay in the hospital.

Key Insight: With Medicare Advantage, you trade a single, large deductible for a series of daily copayments. Always, always check a plan’s "Summary of Benefits" to see its specific hospital costs before you sign up.

This different way of sharing costs is one of the biggest distinctions between sticking with Original Medicare and choosing a Medicare Advantage plan.

Is the Part A Deductible Based on the Calendar Year?

This is easily one of the most misunderstood parts of Medicare, and it's so important to get it right. The Medicare Part A deductible is not an annual deductible. It doesn't reset on January 1st like your car insurance or other health plans.

It’s actually tied to what Medicare calls a benefit period. A benefit period kicks off the day you’re admitted to a hospital as an inpatient. It only ends after you’ve been out of the hospital (or a skilled nursing facility) for 60 consecutive days.

If you have to go back to the hospital after that 60-day break, a brand-new benefit period begins, and yes, you'll have to pay the deductible all over again. This structure means it's entirely possible to pay the Part A deductible more than once in a single year if you have separate hospital stays. It’s a critical detail to understand when you're planning for potential medical expenses.

What Services Does the Deductible Actually Apply To?

The Part A deductible is specifically for inpatient services. Think of it as your entry ticket—it’s what you pay before Medicare starts covering its share of the costs once you are formally admitted to a facility.

It mostly applies to these situations:

- Inpatient Hospital Care: This is the big one. It covers your semi-private room, meals, nursing care, and the drugs and supplies you receive as part of your inpatient treatment.

- Skilled Nursing Facility (SNF) Care: It also covers a stay in a SNF, but only if that stay comes right after a qualifying hospital admission of at least three days.

- Inpatient Mental Health Care: If you receive care in a psychiatric hospital, it falls under the Part A deductible.

- Hospice and Home Health Care: While Part A covers these, the deductible usually doesn't apply. Most of these services come with little to no cost-sharing.

Just as important is what it doesn't cover. The Part A deductible has nothing to do with outpatient services like a check-up with your doctor, preventive screenings, or lab tests at a clinic. Those are all handled by Medicare Part B, which comes with its own separate annual deductible. For more answers to common questions about the entire Medicare program, our comprehensive FAQ about Medicare is a great place to look.

Does Everyone with Medicare Pay the Part A Deductible?

Not always. While anyone on Original Medicare is technically on the hook for the Part A deductible during a hospital stay, many people have other coverage that steps in to pay it for them.

This is one of the main reasons people get additional insurance in the first place.

Here are the most common ways people get that deductible covered:

- Medicare Supplement (Medigap) Plans: Nearly all modern Medigap plans are designed to pay the Part A deductible in full.

- Medicaid: If you have both Medicare and Medicaid, Medicaid generally picks up the tab for your Medicare deductibles and other costs.

- Employer or Union Coverage: Some retiree health plans coordinate with Medicare and help cover the deductible.

If you don't have one of these backups, you'll have to pay the full deductible out-of-pocket each time you start a new benefit period.

Trying to figure out healthcare costs can be a real headache, but you don't have to go it alone. The experts at My Policy Quote are here to help you find a plan that protects you from surprise bills like the Part A deductible. Compare your options and get a free, no-obligation quote today. Visit us at https://mypolicyquote.com.