When you're looking at health insurance, the choice often comes down to two main paths: getting coverage through your job (group health insurance) or buying a plan on your own (individual health insurance). At its heart, this is a decision about what matters most to you.

Group plans, the kind offered by an employer, usually mean lower costs and a much simpler enrollment process. On the other hand, individual plans give you the freedom to choose exactly what you want. It's a classic trade-off: convenience and savings versus control and customization.

Understanding the Health Insurance Landscape

Choosing the right health insurance is one of those big financial decisions that goes way beyond just reading a few definitions. It’s really about understanding how your choice will affect your wallet, which doctors you can see, and how much say you have over your own healthcare. We'll break down this decision based on what really matters—your job, your family's needs, and your budget.

For most people in the U.S., employer-sponsored insurance (ESI) is the default. In fact, it's how roughly 178 million people, or about 63% of working-age adults, get their coverage. The size of the company you work for often dictates the kind of group plan you'll be offered, which directly impacts your costs and options.

Quick Look: Individual vs. Group Health Insurance

Before we get into the nitty-gritty details, this table gives you a quick, high-level look at the fundamental differences between the two types of plans. Think of it as your starting point for understanding where each one shines.

| Feature | Group Health Insurance | Individual Health Insurance |

|---|---|---|

| How You Get It | Through an employer or organization. | Purchased directly from an insurer or marketplace. |

| Cost Structure | Premiums are shared with the employer. | You pay the full premium (subsidies may apply). |

| Plan Choice | Limited to options selected by the employer. | Wide selection of plans and carriers available. |

| Portability | Coverage is tied directly to your job. | Coverage is independent and stays with you. |

| Enrollment | Annual open enrollment or qualifying life events. | Annual open enrollment or qualifying life events. |

Ultimately, the best choice depends entirely on your personal situation. To get a complete walkthrough of the decision-making process, take a look at our guide on how to choose health insurance for smart coverage.

How Group Health Insurance Actually Works

At its heart, group health insurance runs on a straightforward but powerful concept: risk pooling. Instead of scrutinizing one person's health history, an insurer agrees to cover an entire group of employees. This naturally includes a mix of people—some who are perfectly healthy and others who might have ongoing health issues.

By spreading the financial risk across a large pool of people, the insurer isn't making a bet on any single individual. They're banking on the statistical average of the entire group. This is the secret sauce that makes group plans more stable and often more affordable than what you could find on your own.

The Employer's Critical Role

With group insurance, your employer isn't just a bystander; they're the central player in the entire setup. They essentially act as the administrator, making the big decisions that shape your coverage and what you pay for it.

Here’s what your employer handles behind the scenes:

- Plan Selection: They do the legwork, researching and choosing the insurance company and the specific plans available to you.

- Premium Contribution: This is a big one. They pay a chunk of your monthly premium, which is a direct financial benefit that significantly lowers your out-of-pocket costs.

- Enrollment Management: They run the show during open enrollment and manage all the administrative paperwork tied to your plan.

Your employer’s contribution is what truly sets group coverage apart. On average, employers pay a substantial portion of the premium, making it far more manageable month-to-month than an individual plan you'd buy without a government subsidy. It's a key advantage to remember when you're weighing your options.

Eligibility and Enrollment Rules

Unlike individual insurance where pretty much anyone can apply, group coverage is tied directly to your job. The eligibility rules are usually simple but firm. Most companies require you to be a full-time employee, which often means working a minimum number of hours, like 30 or more per week.

Getting enrolled is also a time-sensitive process. You can only sign up or make changes during two specific windows:

- Initial Enrollment: This is your first shot, a period right after you're hired and become eligible for benefits.

- Open Enrollment: This is the annual window where every eligible employee can enroll, switch plans, or make other changes.

If you miss these windows, you'll have to wait until the next one rolls around unless you experience a qualifying life event. Things like getting married, having a baby, or losing other health coverage can open up a special enrollment period just for you. This structured system is in place to keep the risk pool stable all year long.

Navigating the World of Individual Health Insurance

So, you don’t have health coverage through an employer. Maybe you're a freelancer, an entrepreneur forging your own path, or you’ve retired early. Whatever the reason, individual health insurance puts you squarely in the driver's seat. This is the path you take when you buy coverage directly from an insurance company or through a state or federal marketplace.

The biggest perk? Choice. You’re not stuck with a few pre-selected plans your HR department picked out. Instead, you get to explore a whole market of options to find the one that truly fits your life and your budget.

Your Plan on Your Terms

With individual health insurance, you’re the one calling the shots. This means you can build a policy that covers what you actually need, whether that’s comprehensive medical care or more specific services. You get to choose your network type—like a PPO or HMO—and pick a "metal" tier (Bronze, Silver, Gold, or Platinum) that decides how you and the insurer split the costs.

This flexibility isn’t just local; it can be global, too. For expats and families living abroad, a type of individual coverage known as International Private Medical Insurance (IPMI) offers customizable benefits designed to manage healthcare expenses in another country.

For many people, getting this level of personalization is a game-changer. It means you can make sure your plan has strong mental health benefits, which is a top priority for so many of us. You can dive deeper into making sure your mental health needs support, too to see exactly what to look for in a good policy.

Making Coverage Affordable

It’s a common myth that individual plans are always wildly expensive. Yes, you're on the hook for the full premium without an employer kicking in, but government programs can—and do—change the entire financial picture.

The most important thing to understand in the individual market is income-based assistance. Premium tax credits and cost-sharing reductions can dramatically lower your monthly payments and out-of-pocket costs, making great coverage surprisingly affordable.

These subsidies work on a sliding scale based on your household income. This means the sticker price you see on a plan is rarely what you’ll actually end up paying. The less you earn, the more help you're likely to get, which often levels the playing field in the individual vs group health insurance cost debate for self-employed professionals and families.

Comparing Costs: Premiums and Out-of-Pocket Expenses

When you get right down to it, the financial side of health insurance is often the tie-breaker. It’s a common belief that group plans are automatically the cheaper option, but the truth is a bit more complicated than that.

The real cost isn't just what you pay each month. To get the full picture, you have to look at the combination of your premiums and all the out-of-pocket costs you might face over the year.

For group plans, the employer's contribution is a game-changer. Most employers cover a big chunk of the premium, which significantly lowers the amount deducted from your paycheck. This cost-sharing is the main reason group plans often look more affordable at first glance.

On the other hand, individual plans have their own secret weapon: income-based subsidies. If you buy your plan through the Health Insurance Marketplace, you could qualify for a premium tax credit. This can dramatically reduce your monthly payments, sometimes making them even more competitive than what you’d pay for a group plan.

Premiums vs. Total Annual Cost

It's a huge mistake to judge a plan by its premium alone. You need to consider the total financial commitment, which includes your deductible, copayments, and coinsurance. A plan with a low monthly premium might have a sky-high deductible, meaning you’ll pay a lot more out of your own pocket before the insurance company starts to help.

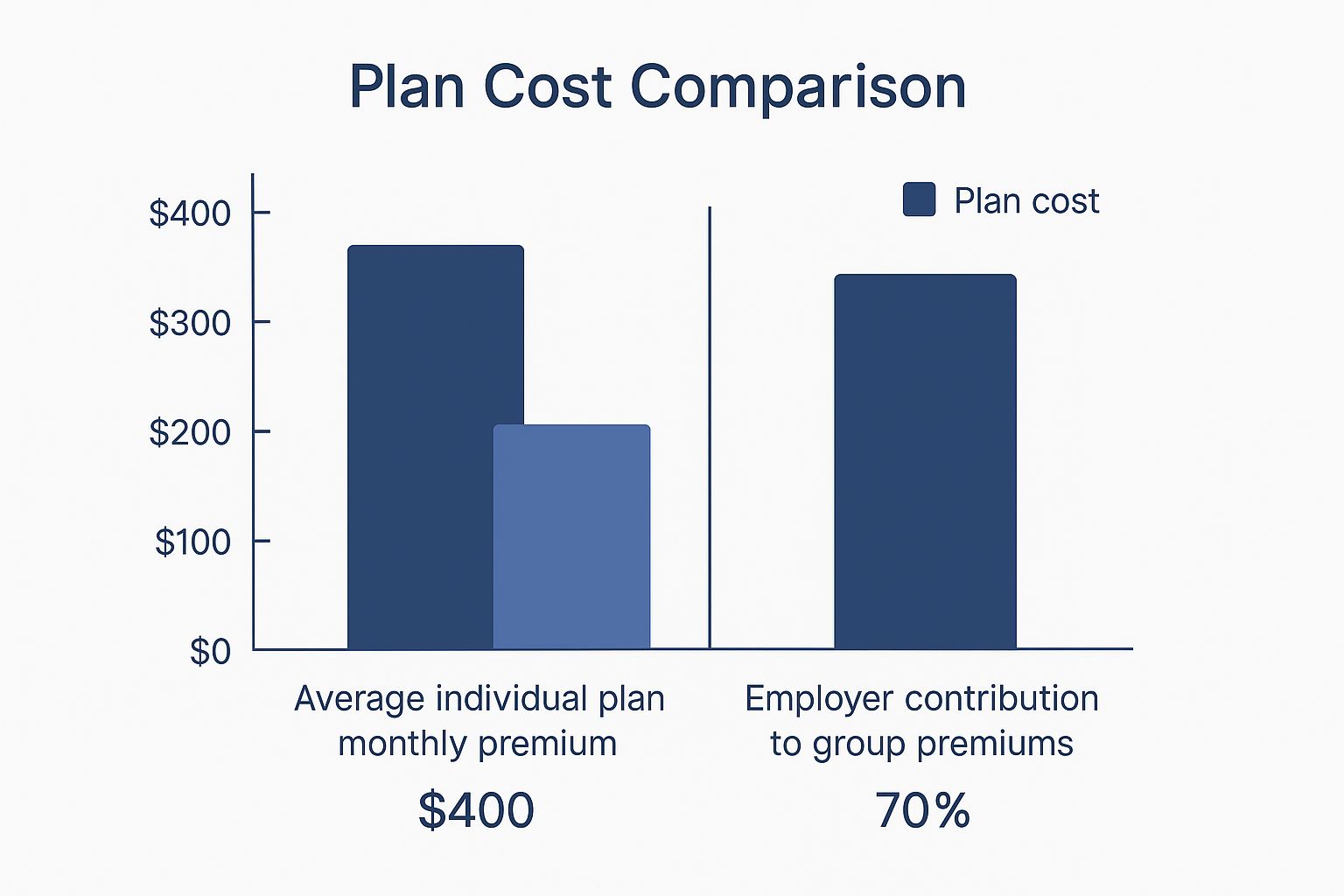

The image below gives a snapshot of how average premiums stack up initially.

This really highlights how much an employer's contribution can cut down the direct cost for employees. But remember, this is just the beginning of the cost conversation.

Let’s look at how the numbers play out in the real world. A well-structured comparison table can help clarify where the money really goes.

Cost Breakdown: Individual vs. Group Plans

This table breaks down the typical cost structures for both types of insurance, showing how different factors contribute to your total annual spending.

| Cost Factor | Group Health Insurance | Individual Health Insurance | Key Considerations |

|---|---|---|---|

| Premiums | Shared between employer and employee, often leading to a lower direct cost for you. | Paid entirely by you, but can be significantly lowered by income-based subsidies. | Don't just look at the monthly bill; subsidies can make individual plans very competitive. |

| Employer Contribution | Typically covers 50-80% of the premium, a major financial advantage. | $0. There is no employer contribution. | This is the biggest built-in savings of most group plans. |

| Subsidies | Not available. You can't get subsidies if you have an affordable group offer. | Available through the Marketplace, based on your income and family size. | Subsidies are designed to make coverage affordable for those without employer options. |

| Out-of-Pocket Costs | Deductibles and coinsurance can often be lower than individual plans. | Can vary widely. Some plans have high deductibles to keep premiums low. | Always check the plan's deductible, copays, and out-of-pocket maximum. |

Thinking through these factors is crucial. The best plan for your wallet depends heavily on your personal situation—your income, your family's health needs, and what your employer (if any) is offering.

A Real-World Cost Scenario

Let’s put this into practice and imagine a family weighing their options:

- Group Plan: Their share of the premium is $500/month. The plan comes with a $3,000 family deductible and 20% coinsurance.

- Individual Plan: After subsidies, their premium is $450/month. This plan has a $5,000 family deductible and 30% coinsurance.

Initially, the individual plan looks a little cheaper each month. But what happens if a family member needs a minor surgery that costs $8,000? The math quickly changes.

With the group plan, they’d pay their $3,000 deductible, plus 20% of the remaining $5,000 (which is $1,000). Their total out-of-pocket cost for the surgery would be $4,000.

With the individual plan, they’d have to pay their full $5,000 deductible before the insurance covers anything.

The most affordable option isn’t always obvious. It requires you to anticipate your potential healthcare needs for the year and calculate the total possible spending, not just the fixed monthly premium.

This exercise proves why looking beyond the monthly bill is so important. You have to understand the trade-offs between fixed costs (premiums) and variable costs (deductibles and copays). For a deeper look at this, you can explore the strategic choice between health insurance vs personal savings for covering medical bills. Ultimately, how much you use your health insurance and your comfort with financial risk will point you toward the right decision.

Digging Into Plan Options and Network Flexibility

When you're comparing individual and group health insurance, the monthly premium is just the tip of the iceberg. The real meat of a plan—what truly makes it valuable—is its flexibility. Can you see the doctors you trust? Are the hospitals you prefer in-network? This is where the two types of coverage really start to show their differences.

With group health insurance, your employer has already done most of the legwork. They've vetted a handful of plans, so your experience is much more streamlined. The good news? Because they're negotiating for a whole group, the options are often high-quality PPO or HMO plans with big, reliable networks.

This simplicity is a huge plus for many people. But the trade-off is that you have less say. You might not find a plan that perfectly fits your needs, like one that includes a specific specialist you’ve been seeing for years.

The Power of Choice With Individual Plans

On the flip side, individual health insurance throws open the doors to a massive marketplace of options. You're in the driver's seat, free to sift through dozens of carriers and plan types. From low-cost HMOs to more flexible PPOs, the choice is yours. This is a game-changer if you or a family member needs access to highly specialized care.

You also get to pick your "metal" tier—Bronze, Silver, Gold, or Platinum—which dictates how you and the insurance company split the costs. This level of control means you can build a plan that truly matches your health needs and your budget.

It boils down to a simple trade-off: group plans offer straightforward, robust coverage with little effort on your part. Individual plans require more homework but give you the power to customize every detail.

How These Choices Play Out in the Real World

Looking at what people actually choose in each market really highlights this difference in flexibility. The data shows that employees with group plans tend to go for more comprehensive coverage.

In fact, recent projections for 2024 show that around 71% of people in small-group plans chose high-value gold-tier coverage, and another 21.5% picked platinum. Shoppers on the individual market, however, were focused more on affordability. 46% chose bronze plans, and 44% went with silver. These numbers also reflect that the individual market often serves more older adults and people with pre-existing conditions. You can dive deeper into these health insurance market comparisons and trends.

This split makes total sense. When your employer is kicking in a good chunk of the premium, those richer plans suddenly become much more affordable. But if you’re footing the entire bill yourself, you’ll naturally use the market’s flexibility to find a plan that works for your wallet, even if that means a higher deductible.

Making the Right Choice for Your Situation

So, how do you translate all these details about individual versus group health insurance into a decision that actually makes sense for you? There's no magic "best" plan. The right choice is the one that fits your work life, your budget, and what you and your family truly need from your healthcare.

Let's walk through a few real-world scenarios to see how this plays out.

The Full-Time Employee

For most people with a full-time job, this is the easiest decision you'll make. If your company offers a group health plan and helps pay for it, that's almost always your best move, financially speaking. That employer contribution is a huge perk you simply won't find on your own.

Your main job here is to pick the best fit from the options your employer gives you. You'll want to look closely at which plan has the doctors you need in its network and what you’ll pay out-of-pocket when you actually use your insurance.

The Freelancer or Gig Worker

When you're a freelancer, contractor, or run your own one-person show, you're the one in charge of HR. Your journey will lead you straight to the individual insurance marketplace. The most important first step? Get a solid estimate of your yearly income to figure out what subsidies you can get.

For the self-employed, subsidies are the great equalizer. They can dramatically reduce monthly premiums, making high-quality individual plans far more accessible and competitive with group plan costs.

From there, it's a balancing act. You have to weigh the monthly premium against the deductible and the freedom to see the doctors you want. If keeping your specific doctor is non-negotiable, a PPO plan might be worth the extra cost. If your budget is tight, a subsidized HMO could be the perfect solution. This flexibility also lets you build a complete safety net; our guide to affordable life insurance is a great place to start thinking about that.

The Small Business Owner

As a small business owner, you have a fascinating choice to make. You could go the traditional route and offer a group plan. This is a powerful tool for attracting and keeping great employees, and by pooling everyone together, you can often get lower rates per person.

Or, you could look into a more modern approach like an ICHRA (Individual Coverage Health Reimbursement Arrangement). This lets you give your employees tax-free money to go buy their own individual plans. They get total control and flexibility, while you get predictable, fixed costs. It's an increasingly popular option because it really does offer the best of both worlds.

Frequently Asked Questions

When you start digging into the details of individual versus group health insurance, a few common questions always seem to pop up. Let's tackle some of the most frequent ones so you can navigate your choices with confidence.

Can I Have Both Group and Individual Health Insurance?

Yes, you technically can hold two health insurance plans at once, but it's rarely a good idea from a practical standpoint. When you have two plans, one is your primary coverage and the other is secondary. Your primary plan always pays first, and the secondary one might pick up some of the leftover costs.

But be warned: the "coordination of benefits" can be a real headache. You won't get paid twice for the same medical bill, and the combined coverage almost never justifies paying two separate monthly premiums.

What Happens to My Insurance if I Lose My Job?

Losing your job doesn't mean you're immediately without coverage. Thanks to the Consolidated Omnibus Budget Reconciliation Act (COBRA), you can choose to continue your old employer's group plan for a limited time—usually up to 18 months. The big catch? You're now on the hook for the entire premium, including the part your employer used to pay.

A better route for many is treating the job loss as a qualifying life event. This unlocks a special enrollment period, letting you shop for an individual plan on the Health Insurance Marketplace. This is where you might qualify for subsidies that make your coverage much more affordable.

Your options post-employment create a critical decision point. COBRA offers continuity with your existing doctors and plan, but often at a very high cost. A new individual plan from the marketplace could be significantly cheaper if you qualify for premium tax credits.

Is Individual Insurance Always More Expensive?

That’s one of the biggest myths out there. While the "sticker price" on an individual plan might look intimidating without an employer chipping in, government subsidies can completely flip the script.

Premium tax credits, which you can get through the marketplace, are specifically designed to make plans affordable based on your household income. For countless freelancers, gig workers, and early retirees, these credits can drop the monthly cost of an individual plan to a point where it’s just as competitive—or even cheaper—than what you'd pay for a group plan.

How Does Family Coverage Differ Between Plan Types?

With a group plan, your employer calls the shots on dependent coverage. Most companies will let you add a spouse and kids, but their contribution toward those premiums is often way less generous than what they cover for you as the employee.

Individual plans, on the other hand, give you total control. You can get a single family plan to cover everyone, or you could buy separate plans for different family members if it makes more sense for their health needs or your budget. This ability to mix and match is a huge advantage when you're weighing individual vs. group health insurance.

Navigating the world of health insurance can feel overwhelming, but you don't have to do it alone. At My Policy Quote, we specialize in helping you find the right coverage that fits your life and your budget. Explore your options and get a personalized quote today!