Medicare Plan N is one of the most practical and popular Medigap plans out there, and for good reason. It acts as a safety net for your Original Medicare, picking up many of the out-of-pocket costs that can otherwise blindside you. What makes it unique is its clever balance: you get a much lower monthly premium in exchange for handling a few small, predictable copayments yourself.

This design makes it a top choice for people who want solid protection but don’t want to overpay for coverage they might not use.

Understanding Medicare Plan N The Basics

Think of Original Medicare (Part A and Part B) as the foundation of your health coverage. It’s great, covering a huge chunk of your hospital and medical bills. But it was never designed to cover everything. It leaves behind some pretty significant gaps—things like deductibles, coinsurance, and copayments that can add up faster than you’d think.

This is exactly where Medigap plans, officially called Medicare Supplement Insurance, step in. These are standardized plans offered by private insurance companies, and their one and only job is to fill those financial holes. If you're new to this, you can get the full picture by reading our guide on what a Medicare Supplement plan is.

A Smart Cost-Sharing Approach

Medicare Plan N is built on a simple trade-off. Instead of paying a high premium for a plan that covers every last dollar, you agree to handle a few small, defined costs yourself. This cost-sharing model is the key to understanding Plan N and why it’s so attractive.

Here’s what you’ll be responsible for:

- A small copayment of up to $20 for some doctor’s office visits.

- A $50 copayment for emergency room visits, but only if you aren't admitted to the hospital.

- The annual Medicare Part B deductible.

Once you’ve met that Part B deductible, Plan N kicks in to cover its share of your medical costs for the rest of the year. This structure gives you a fantastic middle ground—far more protection than Original Medicare alone, but with much friendlier monthly premiums than the "first-dollar" coverage plans.

Plan N is designed for the savvy healthcare consumer. If you’re comfortable with predictable, minor out-of-pocket costs in return for significant savings on monthly premiums, this plan is for you. It’s all about keeping your fixed expenses low while still having a powerful safety net for the big, unexpected medical bills.

To give you a clearer picture, here’s a quick summary of how Plan N works.

Medicare Plan N at a Glance

This table breaks down what Plan N covers and what you'll typically pay for common medical services.

| Coverage Feature | What Plan N Pays | What You Pay |

|---|---|---|

| Part A Coinsurance & Hospital Costs | 100% (up to 365 extra days) | $0 |

| Part B Coinsurance/Copayment | 100% (after your copay) | Up to $20 for some office visits, $50 for ER visits |

| First 3 Pints of Blood | 100% | $0 |

| Part A Hospice Care Coinsurance | 100% | $0 |

| Skilled Nursing Facility Coinsurance | 100% | $0 |

| Part A Deductible | 100% | $0 |

| Part B Deductible | $0 | The annual deductible amount |

| Part B Excess Charges | $0 | 100% of any excess charges |

| Foreign Travel Emergency | 80% (up to plan limits) | 20% (after a small deductible) |

This simple breakdown shows how Plan N gives you comprehensive coverage for the most significant—and potentially expensive—healthcare costs, like hospital stays, while asking you to share a small portion of routine care expenses.

Why Is Plan N So Popular?

Plan N’s popularity has been on a steady rise, especially since other plans were phased out for new enrollees. In fact, between 2014 and 2017, enrollment in Plan N jumped by a massive 20%. It’s now one of the top choices for Medicare beneficiaries, right alongside Plan G.

This trend shows a clear preference for plans that offer a smart blend of strong coverage and real-world affordability. It’s an especially great fit for healthy, active retirees who want reliable protection without paying for the most expensive premium on the market.

What Plan N Actually Covers: A Closer Look

That monthly premium for your Medicare Plan N? It’s not just another bill. Think of it as your financial shield, the thing that stands between you and the kind of medical costs that can derail a retirement. It turns unpredictable expenses into something you can actually budget for.

Let's break down exactly what your Plan N premium buys you, piece by piece.

Hospital Stays and Part A Benefits

Original Medicare Part A is your hospital insurance. When you're admitted, the costs can pile up incredibly fast. Plan N steps in to create a powerful safety net against these major expenses.

One of its biggest jobs is covering the hefty Part A hospital deductible. This is the amount you have to pay out-of-pocket for a hospital stay before Medicare even starts to pay its share. In 2024, that deductible was over $1,600 per benefit period. With Plan N, that entire cost is covered. You pay $0.

But it doesn't stop there. If you have a longer hospital stay, Plan N keeps working for you. It pays the daily coinsurance costs that Original Medicare would otherwise leave for you to handle. This gives you coverage for up to 365 extra days after your standard Medicare benefits run out—a benefit that can literally save you from tens of thousands of dollars in hospital bills.

And if you need to move to a skilled nursing facility after a qualifying hospital stay, Plan N covers that daily coinsurance, too. Your focus should be on recovery, not on worrying about crippling medical bills.

Here’s a quick rundown of what Plan N covers for Part A:

- Part A Hospital Deductible: You pay $0.

- Hospital Coinsurance: Covered for long stays.

- Skilled Nursing Facility Coinsurance: Fully covered.

- Hospice Care: Covers the Part A coinsurance or copayment.

Medical Services and Part B Benefits

Now for your everyday medical care—doctor visits, outpatient procedures, and necessary supplies. Original Medicare Part B is supposed to cover this, but it only pays 80% of the bill. You're left with the remaining 20%, and there's no yearly limit on how high that amount can climb.

This is where Plan N really proves its worth.

Once you’ve paid your annual Part B deductible, Plan N picks up that 20% coinsurance for nearly all of your medical services. We're talking everything from seeing a specialist and having outpatient surgery to getting diagnostic tests and lab work done. For a clearer picture, it helps to know what Medicare covers, like Durable Medical Equipment (DME).

Here’s a simple example: Let's say you need an MRI that costs $2,000. After you've met your deductible, Original Medicare pays its 80% ($1,600). Without a Medigap plan, you’d get a bill for the remaining $400. With Plan N, you’d just pay your small copay for the doctor's visit, and the plan would cover that $400 coinsurance. This protection is the heart of what makes the plan so valuable.

That 20% Part B coinsurance is the real wildcard. It's the gap in Original Medicare that can lead to unlimited, unpredictable out-of-pocket costs. Plan N closes that gap, giving you a crucial buffer against sky-high medical bills.

Other Important Covered Services

Beyond the big-ticket items, Plan N includes a few other key benefits that provide an extra layer of security. They're easy to overlook, but you'll be glad they're there when you need them.

These extras help round out your coverage:

- First Three Pints of Blood: If you need a blood transfusion, Plan N covers the cost of the first three pints of blood each year. Otherwise, you'd pay for this yourself.

- Foreign Travel Emergency Care: Have a medical emergency while traveling abroad? Plan N has your back, covering 80% of your emergency care costs up to the plan's limit once you meet a small separate deductible.

While Plan N is fantastic, it's famous for its cost-sharing structure. It’s important to remember what it doesn't cover: the annual Part B deductible and something called Part B excess charges. While excess charges are rare, it is a key difference between Plan N and other plans. To get the full story on this specific cost, you can learn more about Medicare Part B excess charges in our detailed guide.

Understanding Your Share of the Costs With Plan N

While Plan N is a fantastic shield against huge medical bills, it’s built on a cost-sharing partnership. In exchange for a lower monthly premium, you agree to handle a few small, predictable costs yourself. Knowing exactly what you’ll pay is the key to deciding if this plan fits your budget and lifestyle.

The first thing you’re responsible for each year is the annual Medicare Part B deductible. Think of it as the starting line. You’ll need to pay this amount out-of-pocket for your doctor visits and outpatient services before Plan N’s main benefits kick in.

Once that deductible is met, Plan N takes over most of the heavy lifting, leaving you with just a couple of minor costs to manage.

The Unique Plan N Copayment System

This is where Plan N really stands out from other plans. It uses a simple copayment system, which is the secret sauce behind its more affordable premiums.

Here’s the breakdown:

- Office Visits: You might pay a small copay of up to $20.

- Emergency Room Trips: You’ll have a copay of up to $50, but only if you aren’t admitted to the hospital.

These copays are designed to be predictable and easy to budget for, so you won’t get hit with the kind of financial surprises that can happen with Original Medicare alone. If you want a deeper look at how deductibles work, check out our guide on the Medicare deductible for 2024.

Let’s see how this plays out in the real world.

Example in Action: Meet Sarah

Sarah is a retired teacher with Medicare Plan N. She’s already met her Part B deductible for the year. In April, she sees her doctor for a check-up and pays a simple $20 copay. A few months later, she twists her ankle and heads to the ER. They treat the sprain and send her home, so she pays a $50 copay. For the rest of the year, Plan N covers her Part B coinsurance completely.

Sarah’s story shows how these small, fixed costs work. She can plan her healthcare budget without worrying about massive, unexpected bills. The math backs this up—for most people, these copays don’t add up to much over a year, which is a world away from the thousands you could owe with Original Medicare alone.

The Deal with Part B Excess Charges

There's one other cost to be aware of with Plan N: Part B excess charges. This is a major difference between Plan N and other popular options like Plan G.

An excess charge is an extra fee—up to 15% over the Medicare-approved price—that some doctors are legally allowed to bill. Plan N does not cover these charges, so if your doctor bills for them, you’d be responsible for paying.

But before you worry, let’s put this in perspective.

The reality is that Part B excess charges are rare. The vast majority of doctors in the U.S. "accept Medicare assignment," meaning they agree to take the Medicare-approved amount as full payment. They legally cannot bill you for an excess charge.

On top of that, several states have laws that flat-out prohibit doctors from billing for excess charges, so it’s a non-issue for residents there.

While it’s something to know about, it's a manageable risk for most people, especially if you just confirm that your doctor accepts Medicare assignment beforehand. This calculated risk is a big reason why Plan N can offer such attractive, lower premiums.

How Plan N Compares to Other Popular Options

Choosing your Medicare path can feel like standing at a crossroads. You’ve got signs pointing in a few different directions, and it’s hard to know which way to go. Plan N is a fantastic option, but it doesn't exist in a vacuum. To really know if it’s the right fit for you, we need to see how it stacks up against its main competitors: the very similar Plan G and the totally different world of Medicare Advantage.

Getting this comparison right is everything. It’s the difference between picking a plan that feels like a perfect partner and one that leaves you with unexpected bills and headaches down the road. Let's put them side-by-side to see where each one truly shines.

Plan N vs Plan G The Sibling Rivalry

Think of Plan N and Plan G as close siblings—they share most of the same DNA but have slightly different personalities. Both give you rock-solid, comprehensive coverage for the big gaps in Original Medicare, like the hospital deductible and that 20% coinsurance for doctor services.

The real difference boils down to just two specific costs:

- Part B Excess Charges: Plan G covers these; Plan N doesn't. Excess charges are an extra 15% that some doctors are legally allowed to bill on top of the Medicare-approved amount.

- Copayments: Plan N requires small copays for certain visits—up to $20 for a doctor's office visit and up to $50 for an ER trip. After the deductible, Plan G has no copays at all.

Because Plan G covers these extra bits and pieces, its monthly premium is almost always higher than Plan N’s. The choice really comes down to a simple trade-off: are the monthly premium savings from Plan N worth the small risk of an excess charge and the certainty of a few minor copays?

For many people, the answer is a clear yes. Excess charges are pretty rare—and even banned in several states—so the lower monthly premium on Plan N often leads to real savings over the year. Our deep dive into Medigap Plan G can give you even more detail to help weigh your options.

When comparing Plan N and Plan G, just ask yourself this: "Do I want to pay a little more every month for total predictability, or would I rather save on premiums and handle small, occasional costs myself?" Your answer points directly to your plan.

Medigap Plan N vs Medicare Advantage The Philosophical Divide

Comparing Plan N to a Medicare Advantage (Part C) plan isn't like comparing siblings. It’s more like comparing two completely different philosophies on how to get your healthcare. It’s a classic choice between freedom and structure.

Plan N is a supplement that works with Original Medicare. You keep your red, white, and blue card, and Plan N fills in the gaps. This setup gives you the freedom to see any doctor or visit any hospital in the entire country that accepts Medicare—no networks and no referrals needed. This freedom is the heart and soul of the Medigap philosophy.

Medicare Advantage plans, on the other hand, are an alternative to Original Medicare. Private insurance companies bundle everything—Parts A, B, and usually D (prescriptions)—into one neat package. These plans almost always operate with provider networks, like an HMO or PPO. To keep costs low, you have to use their doctors and hospitals, and you'll often need a referral to see a specialist.

While Medicare Advantage enrollment reached 55% of beneficiaries in 2025 (that’s about 34.1 million people), Plan N has become a go-to choice for the other 45% who prioritize the flexibility of Original Medicare. This makes it especially appealing for those aged 60-64 planning ahead or anyone who wants stability that isn't tied to an employer's health plan. You can see more data on these trends by reviewing the latest Medicare Payment Advisory Commission report.

This core difference in how they're built leads to wildly different experiences.

Plan N vs Plan G vs Medicare Advantage A Feature Showdown

To make it simple, let's break down the key differences between your three main choices. This table should help you quickly see which approach aligns best with what you value most in your healthcare coverage.

| Feature | Medicare Plan N | Medicare Plan G | Typical Medicare Advantage Plan |

|---|---|---|---|

| Doctor Choice | Total freedom to see any doctor nationwide that accepts Medicare | Total freedom to see any doctor nationwide that accepts Medicare | Restricted to the plan's local or regional network (HMO/PPO) |

| Referrals | Never needed to see a specialist | Never needed to see a specialist | Often required for specialists in HMO plans |

| Out-of-Pocket Costs | Predictable: Part B deductible, then small copays for some visits | Ultra-predictable: just the Part B deductible for the year | Varies: includes copays, coinsurance, and a yearly maximum |

| Monthly Premium | You pay for Part B + the Plan N premium | You pay for Part B + the Plan G premium (usually higher than N) | May have a $0 premium, but you still pay for Part B |

| Extra Benefits | Does not include perks like dental, vision, or drug coverage | Does not include perks like dental, vision, or drug coverage | Often bundles in benefits like dental, vision, hearing, & gyms |

So, what’s the bottom line?

If you value maximum freedom, nationwide coverage, and predictable costs for major medical events, Plan N is an incredibly strong contender. But if you prefer an all-in-one plan, are comfortable staying within a network, and want extra benefits like dental and vision included from the start, then a Medicare Advantage plan might be a better fit for your lifestyle.

Is Medicare Plan N the Right Choice for You?

Choosing a Medicare plan isn't about finding the single "best" option out there—it's about finding the one that fits your life perfectly. Instead of just rattling off features, let’s look at how Medicare Plan N actually plays out for different people.

By walking through a few real-world scenarios, you can see which one feels most like you. This helps connect the dots between the plan’s technical details and what you actually need, moving you from simply understanding Plan N to knowing if it’s the right partner for your healthcare journey.

The Healthy and Active Retiree

Meet David. He’s a recently retired teacher who loves spending his time hiking and traveling. He's in great health and usually only sees a doctor for his annual check-up. David wants solid protection in case of a major, unexpected health event—like a bad accident or a serious illness—but he doesn’t want to shell out the high monthly premiums that come with first-dollar coverage.

For someone like David, Plan N is practically a perfect match.

- Lower Premiums: The money he saves each month compared to Plan G is significant. That leaves more in his budget for what he really loves, like his travel fund.

- Predictable Copays: Since he rarely gets sick enough to need a doctor, the possibility of a $20 copay every now and then is no big deal.

- Major Medical Security: He can relax knowing that if he ever ends up in the hospital, the massive Part A deductible and that scary 20% Part B coinsurance are completely taken care of.

David's approach is smart and simple: save money on premiums every single month and feel confident that he can handle the small, occasional out-of-pocket costs himself.

The Savvy Self-Employed Professional

Now, let's consider Maria, a freelance graphic designer who has managed her own health insurance for years. As a business owner, she’s a pro at weighing costs against benefits. She needs reliable, straightforward coverage without the restrictive networks that could limit her choice of specialists.

Plan N's structure clicks with her financial mindset. The freedom to see any doctor who accepts Medicare is a huge plus, and the cost-sharing model is a calculated trade-off she's happy to make. The lower premium feels like a smart business decision, and she can easily budget for the occasional copayment.

For someone who's self-employed, every dollar counts. Plan N gives them the freedom and strong coverage they need without making them pay for benefits—like coverage for excess charges—that they will probably never use. It's a pragmatic and financially sound choice.

Who Should Think Twice About Plan N?

While Plan N is a fantastic choice for many, it isn't a one-size-fits-all solution. For some people, other plans might be a much better fit for their health needs and personal preferences.

You might want to look at a different plan if you:

- Want Absolute Predictability: If the idea of paying a copay for any doctor visit makes you uneasy and you'd rather pay nothing out-of-pocket besides your deductible, Plan G is likely a better choice.

- Live Where Excess Charges Are More Common: These charges are rare overall, but if you live in one of the handful of states that allow them and you don't want to ever worry about that bill, the higher premium for Plan G could be worth the peace of mind.

- Have Chronic Health Conditions: If you know you'll be seeing doctors frequently to manage an ongoing condition, those $20 copays could start to add up. In that case, it's crucial to do the math and compare the total annual cost of Plan N (premiums + all potential copays) versus Plan G's higher, all-inclusive premium.

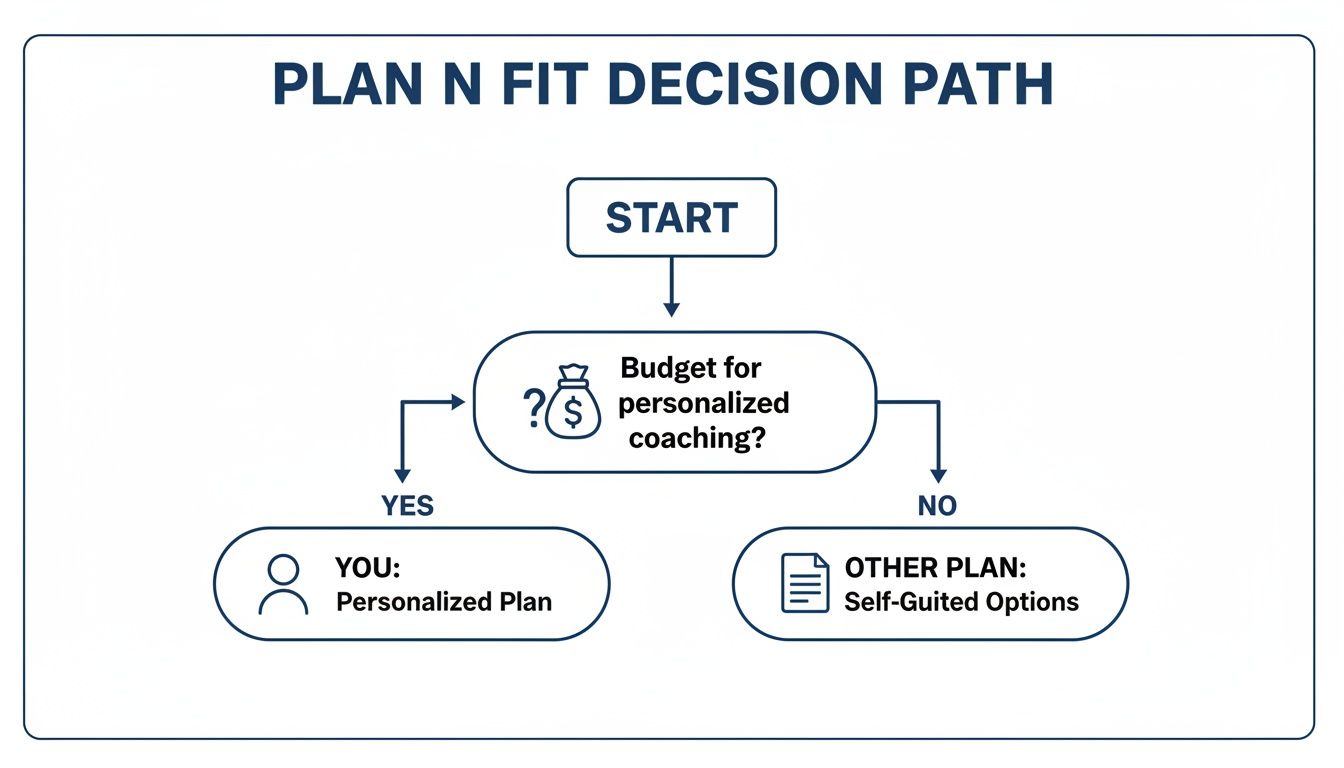

Enrolling in Plan N: Your Step-by-Step Guide

So, you’ve decided Plan N's blend of solid coverage and lower premiums feels right for you. Great choice. Now comes the enrollment part, and getting the timing right here is everything. It can make all the difference. Your best friend in this process is the Medigap Open Enrollment Period.

Think of it as your one-time, golden ticket. This is a six-month window that kicks off the very first day of the month you are both 65 or older and signed up for Medicare Part B. During this period, insurance companies are not allowed to use your health history against you. That means they can't deny you a policy or jack up your rates. It’s your guaranteed pass to get any Medigap plan you want, including Plan N.

Your Four Steps to Enrollment

Once you're in that Open Enrollment window, the process itself is pretty simple. But here’s the key thing to remember: while the benefits of Plan N are standardized by the government—meaning a Plan N from one company is the same as a Plan N from another—the prices are not. That makes shopping around absolutely critical.

Here’s a simple roadmap to get you started:

- Confirm Your Eligibility: Your most important date is the start of that six-month Medigap Open Enrollment Period. Know when yours begins and ends, because this is the easiest, no-questions-asked time to enroll.

- Research Insurance Companies: Dozens of highly-rated carriers offer Plan N. You'll want to look for companies with a long history of financial stability and a good reputation for customer service.

- Compare Quotes: This is where you save real money. Since the coverage is identical, your goal is to find the lowest premium from a company you trust. Working with an independent broker can be a huge help here, as they can pull quotes from multiple carriers for you all at once.

- Complete Your Application: After you’ve picked a company, the application is straightforward. Your agent can walk you through the paperwork, which usually only takes a few minutes.

This decision tree gives you a quick visual for thinking about whether Plan N's cost-sharing approach fits your style.

The flowchart really just highlights that if you’re okay with small, predictable copayments in return for a lower monthly bill, Plan N is a very logical path to take.

Remember, the single biggest mistake you can make is assuming all Plan N policies cost the same. Shopping around can save you hundreds, or even thousands, of dollars over the life of your policy for the exact same coverage.

A Few Final Questions on Plan N

Even after you've done your homework, a few questions always seem to pop up. Let's tackle the most common ones head-on, so you can feel completely confident about whether Plan N is the right fit for you.

Do I Have to Pay the Plan N Copay for Every Single Doctor Visit?

Not at all. This is a common point of confusion, but the answer is a relief. The up-to-$20 copay is specifically for diagnostic office visits—the ones where you're trying to figure out what's wrong.

It does not apply to the preventive care that keeps you healthy in the first place. You typically won't pay a dime for services like:

- Your annual wellness visit

- Flu shots and other routine vaccinations

- Many types of cancer screenings

The copay is also not for things like standalone lab work or physical therapy. It’s tied directly to certain office and ER visits, not every interaction you have with the healthcare system.

What Exactly Are Part B Excess Charges, and Should I Lose Sleep Over Them?

Excess charges are an extra 15% that some (but not all) doctors are legally allowed to bill on top of the standard Medicare-approved amount. Plan N is one of the few Medigap plans that doesn't cover these, which is a key difference from Plan G.

But here’s the good news: you really shouldn't lose sleep over them.

These charges are actually quite rare. Why? First, the vast majority of doctors in the U.S. "accept Medicare assignment." This is just a formal way of saying they agree to take the Medicare rate as full payment and legally cannot tack on an excess charge. Second, many states have outlawed them completely. It's a factor to be aware of, but for most people, it's a non-issue.

Will My Monthly Plan N Premium Go Up Over Time?

Yes, it’s best to expect and budget for gradual increases in your monthly premium. Private insurance companies set the rates for Medigap plans, and they adjust them over time to keep up with inflation and rising healthcare costs.

Most Medigap policies, including Plan N, are "attained-age rated." This just means your premium is based on your current age and will tick up a little as you get older. It’s a normal and expected part of how this coverage works.

This model helps keep the initial premiums more affordable when you first enroll. While your rate will climb, the increases are usually gradual and manageable for most budgets.

Feeling confident about your Medicare choices is our top priority. At My Policy Quote, we make it easy to compare quotes from top-rated insurance carriers to find the best rate for your Plan N policy. Our licensed agents provide unbiased guidance to help you secure the right coverage at the right price. Visit us at https://mypolicyquote.com to get your free, no-obligation quotes today.