Shopping for life insurance isn't just about finding the cheapest monthly premium. It’s about digging deeper to find the right protection. That means getting honest about your family's financial needs, understanding the real differences between policies like term and whole life, and making sure the company you choose will be there for the long haul.

Finding the Right Policy Starts with Knowing What to Look For

Let's be real—choosing a life insurance policy feels like a huge task. But when you cut through the noise, it really boils down to a few key decisions. This guide will help you compare policies based on what actually matters for your family's security, moving way beyond that initial price tag. The goal is simple: find solid protection that doesn't break the bank.

A good policy should fit seamlessly into your broader financial risk management strategy. It’s not just a payout; it's a promise to secure your family's future when things get uncertain. That promise is only as good as the fine print, so you need to know exactly what you’re buying.

The global life insurance market has seen explosive growth, jumping from $1.9 trillion in 2017 to over $3.1 trillion today. What does this mean for you? More options, better pricing, and modern features are now available. This competitive market puts you in the driver's seat—if you know what to look for.

Key Comparison Points

To keep things simple, focus your search on these core areas:

- Policy Type and Term Length: Are you looking for temporary coverage (term) or lifelong protection (permanent)? If you have a 30-year mortgage, you need a term that lasts at least that long. Match the policy to your biggest financial responsibilities.

- Coverage Amount (Death Benefit): Will the payout be enough to clear debts, replace your income for a few years, and fund big goals like your kids' college tuition? Don't guess here.

- The True Cost: Look past the premium. A smarter way to compare is by calculating the cost-per-thousand dollars of coverage. This gives you a true apples-to-apples view of what you're paying for.

- Insurer Financial Strength: This is a big one. Check the company's stability with ratings from agencies like A.M. Best. A policy is only as good as the insurer's ability to pay claims decades from now.

One of the biggest mistakes people make is comparing a term life quote from one company to a whole life quote from another. They are completely different products. Always compare like with like to get a true sense of value.

To help you stay organized, here’s a quick rundown of the essential factors to consider.

Key Factors for Comparing Life Insurance Policies at a Glance

This table breaks down the core elements you should evaluate when you have a few different life insurance quotes in front of you.

| Comparison Factor | What to Look For | Why It Matters |

|---|---|---|

| Needs Assessment | Income replacement, debt payoff, future goals | Ensures your coverage amount is sufficient, not just a guess. |

| Policy Type | Term, Whole, Universal Life | Matches the coverage duration and features to your life stage. |

| True Cost | Premium, cost-per-$1,000, internal fees | Reveals the actual value beyond the monthly payment. |

| Insurer Financial Health | A.M. Best, Moody's, S&P ratings (A-rated or higher) | Guarantees the company can fulfill its long-term promise. |

Think of these factors as your personal checklist. Running each policy option through this framework will give you the clarity and confidence to make a smart, informed decision for your family.

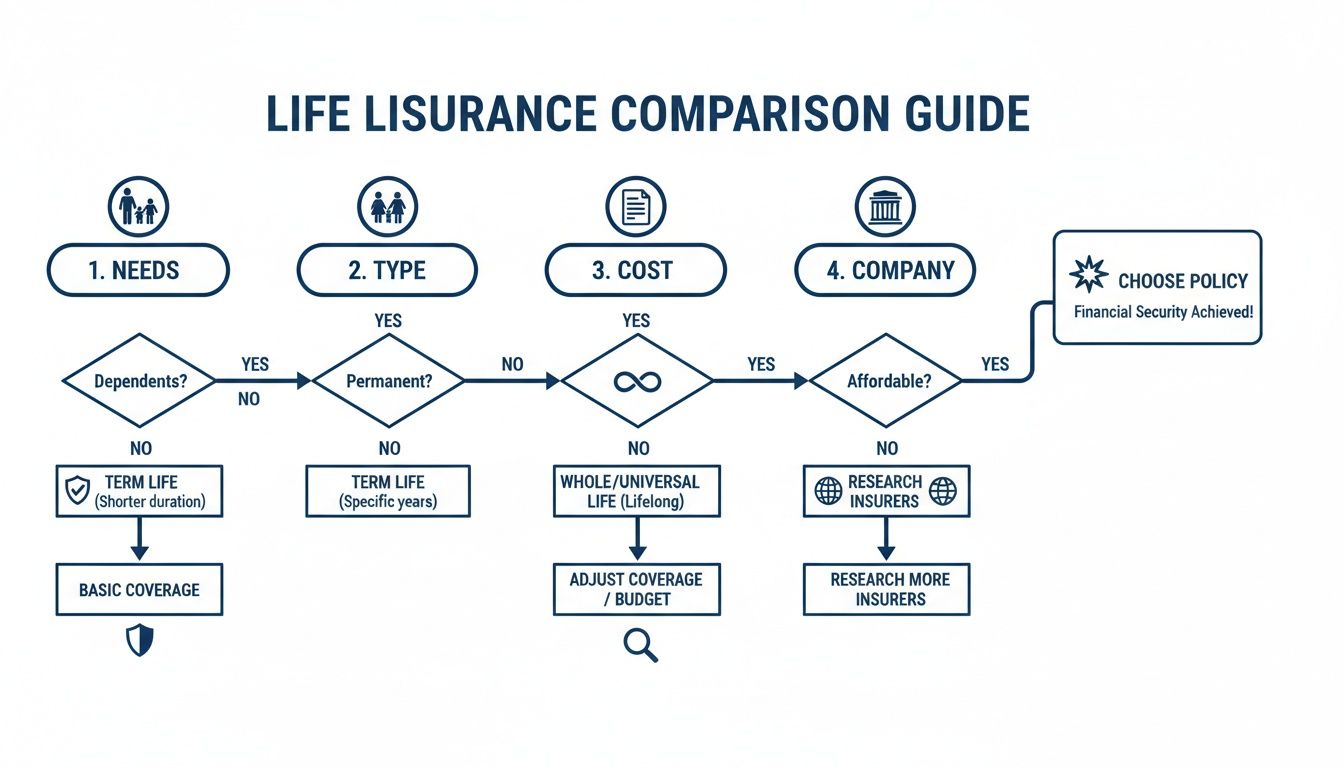

Matching Your Life Stage to the Right Policy Type

Before you can even start comparing life insurance policies, you have to know what you’re comparing. The insurance world basically breaks down into two big categories: policies that last for a set time (term life) and policies that cover you for your entire life (permanent life).

Picking the right one from the get-go is the most important move you'll make. It’s about aligning the policy with what your family actually needs.

Trying to compare a 20-year term policy to a whole life policy is an apples-to-oranges game. It just won't give you a clear sense of value because they're built for completely different jobs. Your current life stage—whether you're buying a home, paying for college, or planning your legacy—is your best guide.

This flowchart lays it out perfectly. Notice how choosing the type of policy comes way before you ever look at a price tag or an insurance company's name.

The whole point is to match the policy to your real-life financial situation first. Everything else comes second.

For Temporary Needs, Term Life Insurance Is King

Term life is as straightforward as it gets. You get protection for a specific period—say, 10, 20, or 30 years. If you pass away during that time, your family gets a tax-free payout. If you outlive the term, the policy just ends. No payout, no fuss.

This makes it the perfect tool for covering financial responsibilities that have an expiration date.

- A Young Family with a Mortgage: Picture a couple in their early 30s with two small kids and a brand new 30-year mortgage. Their biggest worry? Making sure the house is paid off and the kids are supported until they're independent. A 30-year term policy gives them a huge amount of coverage for a surprisingly low premium, lining up perfectly with their biggest debts.

- Covering Business Loans: Think of a small business owner who just took out a big 10-year loan to expand. A 10-year term policy is a smart move. It ensures their partners or family won't get stuck with that debt if something happens to them before it’s paid off.

Key Takeaway: Term life is all about getting the biggest financial safety net for the lowest possible cost during the years you need it most. For the vast majority of families, it’s the cornerstone of their protection plan.

When Permanent Coverage Makes Sense

Permanent life insurance—like Whole Life and Universal Life—is designed to last your entire life, as long as you pay the premiums. But here's the twist: unlike term, these policies also build cash value over time, and that growth is tax-deferred.

This combo of lifelong coverage plus a savings-like feature makes it a fit for more complex, long-term goals. If you want to get into the nitty-gritty, you can explore our guide on the different types of life insurance explained.

Whole Life Insurance for Predictability

With whole life, you get guarantees across the board: the premium will never go up, the death benefit is locked in, and the cash value growth is guaranteed. That predictability is a huge draw for certain situations.

Real-World Scenario:

Imagine a 55-year-old who wants to leave a guaranteed inheritance for her grandkids and cover her final expenses without it becoming a problem for her kids. A whole life policy gives her a permanent death benefit that will be there no matter when she passes. The fixed costs and guaranteed growth offer total peace of mind for legacy planning.

Universal Life for Flexibility

Universal life (UL) is another permanent option, but its main feature is flexibility. You can often adjust your premium payments and even the death benefit amount as your life changes. It’s a great feature, but it also adds complexity since the policy's growth is often tied to changing interest rates.

Real-World Scenario:

A 45-year-old executive is already maxing out her 401(k) and other retirement accounts. She might use a UL policy for more than just the death benefit—it can act as another retirement savings vehicle. She can take advantage of the tax-deferred cash value growth and has the freedom to adjust her payments if her income changes.

By figuring out which of these stories sounds most like yours, you can narrow down your options and start comparing policies that are actually built to help you reach your goals.

Looking Beyond the Premium to Find the True Cost

The monthly premium is the first number everyone latches onto. It's easy to understand, and let's be honest, it's what hits your bank account every month. But focusing only on that number is one of the biggest mistakes you can make when buying life insurance.

It’s like comparing two cars just by their monthly payments without looking at the sticker price or fuel efficiency. You’re missing the real story. The true cost isn’t just about the premium; it’s about the value you get for every single dollar you spend.

Calculating Your Cost-Per-Thousand

To get a real, apples-to-apples comparison, you need to standardize the cost. The best way to do that is with a simple metric called cost-per-thousand.

This little calculation strips away the confusion of different coverage amounts and tells you exactly how much you're paying for each $1,000 of death benefit.

Here’s the formula:

- Step 1: Calculate the annual premium (monthly premium x 12).

- Step 2: Divide your total coverage amount by $1,000.

- Step 3: Divide the annual premium by the result from Step 2.

Let's put it into practice. Say you're looking at two different 20-year term policies.

- Insurer A offers a $500,000 policy for $30 a month.

- Insurer B offers a $750,000 policy for $40 a month.

Insurer A looks cheaper at first glance, right? But is it the better deal? Let's do the math.

Sample Cost-Per-Thousand Comparison

Here’s a breakdown of how these two policies stack up when you look at their true cost.

| Insurer | Annual Premium | Coverage Amount | Cost Per $1,000 of Coverage |

|---|---|---|---|

| Insurer A | $360 ($30 x 12) | $500,000 | $0.72 ($360 / 500) |

| Insurer B | $480 ($40 x 12) | $750,000 | $0.64 ($480 / 750) |

Turns out, Insurer B is actually the better value. Even though the monthly premium is higher, you're only paying $0.64 for every $1,000 of protection. Insurer A costs $0.72. This is the kind of insight that empowers you to make a smarter financial choice.

What's Driving Your Rates?

The premium an insurer offers you is a direct reflection of how much risk they think they're taking on. Several factors play a huge role in this calculation.

- Age: This is the big one. The younger and healthier you are, the less you'll pay. Period.

- Health: Insurers will look at your medical history, any chronic conditions like diabetes or high blood pressure, and even your family's health history.

- Lifestyle: Do you smoke? A smoker can expect to pay two to three times more than a non-smoker. Do you have high-risk hobbies like skydiving? That'll raise your rates, too.

- Policy Riders: Adding extra features like a waiver of premium or an accelerated death benefit is great for flexibility, but each one will add a little to your monthly cost.

A word of caution: Be brutally honest on your application. Hiding a medical condition or that you smoke might get you a lower quote upfront, but it’s grounds for the insurer to deny a claim later—leaving your loved ones with nothing. It’s just not worth the risk.

And if you're looking at permanent policies like whole or universal life, things get even more complex. You have to factor in internal fees, management costs, and the interest credited to your cash value. These moving parts all impact how your policy performs over time. Our guide on how much life insurance costs dives deeper into this.

By looking past the sticker price and using tools like the cost-per-thousand calculation, you get a much clearer picture of what you're actually buying.

Looking Beyond the Death Benefit: Riders and Living Benefits

When you're comparing life insurance policies, it’s easy to focus on one thing: the death benefit. But the best policies today are built to deliver real, tangible value while you’re still living.

These extra features, known as riders and living benefits, can transform a standard policy into a flexible financial safety net. Ignoring them is one of the most common mistakes people make. They might seem like minor details, but when life throws a curveball, they can be absolute game-changers.

What Are Riders, and Why Do They Matter?

Think of riders as optional upgrades for your policy. They let you customize your coverage to fit your unique worries and life situations. While some might add a small amount to your premium, the protection they offer is often worth far more.

Here are a few of the most impactful riders to look for:

- Accelerated Death Benefit (ADB): This is one of the most powerful riders out there, and it’s often included at no extra cost. If you're diagnosed with a terminal illness (usually with a life expectancy of 12-24 months), the ADB lets you access a big chunk of your death benefit—tax-free—while you're still alive.

- Waiver of Premium: What happens if you become totally disabled and can't work? This rider is a lifesaver. It keeps your life insurance from lapsing by waiving your premium payments during your disability.

- Critical Illness Rider: This feature lets you tap into your death benefit if you're diagnosed with a major illness like a heart attack, stroke, or invasive cancer. You can use the money for anything—medical bills, replacing lost income, or just giving yourself some breathing room.

Pro Tip: When you’re looking at two policies with similar premiums, always check which living benefit riders are included automatically versus those that cost extra. A slightly more expensive policy might be a much better deal if it comes packed with a robust set of riders at no additional charge.

The Hidden Power of Cash Value

If you're considering a permanent policy like whole or universal life, the cash value is another powerful living benefit. A portion of every premium you pay goes into a tax-deferred savings account that grows over time.

This isn't just money sitting there; it's a financial tool you can actually use.

You can take out loans against your cash value for pretty much any reason—a down payment on a house, your kid's college tuition, or even to supplement your retirement income. The best part? You generally don't have to pay these loans back, though any outstanding balance will be deducted from the final death benefit. It's a source of liquidity that term policies just can't match.

Want to dive deeper into how these add-ons work? You can check out our guide on what is a rider on life insurance to learn more.

How Technology is Changing the Game

The life insurance world is changing fast, thanks to technology. Things like AI-driven underwriting, digital platforms, and wellness plans that reward you for healthy habits are reshaping what policies can offer.

This means newer policies often come with more personalized pricing and much better digital access than older ones. You can get a sense of where things are headed by looking at the global forecast for the life insurance market.

So, as you compare policies, remember to look beyond the basic numbers. Dig into the riders, understand the living benefits, and think about how cash value could fit into your financial goals. That deeper look is the key to finding a policy that truly protects you and your family—both today and tomorrow.

How to Vet an Insurance Company’s Financial Health

A life insurance policy is a long-term promise. You're paying premiums today for a payout that might not happen for 10, 20, or even 50 years. This makes the company's financial stability just as critical as the policy's premium.

Think about it: the cheapest policy on the market is completely worthless if the company behind it goes under before your family needs it. Verifying an insurer’s financial health isn't just a smart move; it’s a non-negotiable part of comparing policies.

Cracking the Code on Financial Strength Ratings

Luckily, you don’t need to be a Wall Street wizard to figure this out. Independent rating agencies do all the heavy lifting for you, digging into an insurer’s balance sheet, cash flow, and overall business health. While it's always useful to know how to analyze financial statements, these ratings give you a reliable shortcut.

The main agencies to look for are:

- A.M. Best: This is the gold standard for the insurance world. Their top ratings are A++ (Superior) and A+ (Superior).

- Moody's: This agency rates a company's ability to meet its long-term financial obligations. Look for grades like Aaa (Highest Quality) and Aa (High Quality).

- Standard & Poor's (S&P): Another major player. S&P’s top scores are AAA (Extremely Strong) and AA (Very Strong).

You can almost always find these ratings for free right on the insurer’s website or by checking the agency's site directly.

Rule of Thumb: Stick with companies that have an 'A' rating or better from at least two of these major agencies. Anything in the 'B' range is a serious red flag that points to potential instability down the road.

More Than Just Numbers—Customer Service Matters

Financial strength tells you if a company can pay a claim. But what about its willingness to pay it fairly and without a fight? This is where an insurer's customer service reputation comes into play, and it’s a huge piece of the puzzle.

A company with perfect ratings but awful customer service can turn an already devastating time for your family into an absolute nightmare. You need an insurer that will be responsive, compassionate, and helpful when your loved ones need them most.

Using the NAIC Complaint Index

The National Association of Insurance Commissioners (NAIC) tracks customer complaints and boils them down into a simple complaint index. It’s a powerful, objective way to see how an insurer actually treats its policyholders.

Here’s how to read it:

- A score of 1.0 means the company gets an average number of complaints for its size.

- A score below 1.0 is great—it means fewer complaints than expected.

- A score above 1.0 suggests the company gets more complaints than its peers.

You should aim for insurers with a complaint index score that’s consistently at or below the 1.0 national average. A high score is a clear warning sign of potential headaches with claims, communication, or service in general.

This two-pronged approach—checking both financial ratings and customer service records—ensures the promise made to you is backed by financial muscle and a genuine commitment to policyholders.

Common Mistakes to Avoid When Comparing Policies

You’ve done the work, you’ve got the quotes, and it feels like you're at the finish line. But this is where some of the costliest mistakes happen. It’s surprisingly easy to fall into a few common traps right when you’re about to make a final decision.

Let’s be clear: avoiding these slip-ups is the last crucial step to make sure the policy you choose actually does its job for your family.

Comparing Apples to Oranges

One of the most frequent errors I see is people trying to compare wildly different types of policies. For instance, putting a quote for a 20-year term policy next to one for a whole life policy just doesn't work. It's a classic apples-and-oranges scenario.

Term life is built for temporary, high-coverage needs, while whole life is designed for lifelong protection and building cash value. They serve completely different purposes and will, of course, have completely different price tags. You have to compare like with like.

Focusing Only on the Lowest Premium

It’s so tempting to just grab the cheapest quote and call it a day. But that's a shortcut you might regret. The lowest premium almost always comes with trade-offs you won’t see until you need the coverage most.

Why is it so cheap? Maybe it’s missing critical riders, like a waiver of premium or an accelerated death benefit. Or worse, the low price is from an insurer with a shaky financial strength rating. A life insurance policy is a decades-long promise. Saving a few bucks a month isn’t worth the risk of picking a company that might struggle to pay your family’s claim down the road.

Key Insight: A slightly higher premium for a policy from an A-rated insurer with robust living benefits is often a far better value than the cheapest option from a less stable company. The peace of mind is worth the marginal cost.

Overlooking Global Market Differences

It's also worth remembering that the life insurance world looks different depending on where you are. For example, a place like Hong Kong has a 79% life insurance ownership rate, which fuels a super-competitive market. In contrast, growth in places like Germany has been slower.

What does this mean for you? It means that product features, availability, and even pricing can change a lot based on regional economic factors. It's a small detail, but you can see how it plays out in this global insurance report from Allianz.com.

Getting Drowned in Too Many Quotes

In an effort to be thorough, it’s common to request quotes from a dozen or more companies. This usually backfires and leads to "analysis paralysis." The sheer amount of information is overwhelming, and you end up not making a decision at all.

A much smarter strategy is to be more focused.

- Narrow it down: Start by picking just three to five highly-rated insurance companies.

- Ask for identical quotes: Request the exact same policy type, term length, and coverage amount from each one.

- Compare the details: With a manageable number of options, you can actually dig into the costs, riders, and company reputations without getting lost.

Finally, and this is a big one, don't bend the truth on your application. Trying to get a lower rate by being less than honest about your health or lifestyle is a form of fraud. If the insurer finds out, they can legally deny the claim, leaving your family with nothing. Honesty really is the best policy here.

To learn more, check out these common mistakes when buying life insurance.

Your Questions, Answered: The Final Steps in Comparing Life Insurance

Even with all the research done, it’s natural to have a few last-minute questions as you get ready to make a decision. Let’s tackle some of the most common ones that come up when you’re on the home stretch.

How Many Quotes Should I Really Compare?

Getting quotes can feel like a part-time job, but you don't need dozens to make a smart choice.

A good goal is to compare quotes from at least three to five different, well-regarded insurance companies. This gives you a solid feel for the market without sending you into analysis paralysis. Too few, and you might miss a much better deal. Too many, and it all just becomes a blur of numbers.

Just be sure you're comparing apples to apples—the same policy type and coverage amount—to get a clear picture.

Should I Use an Independent Agent or Go Straight to the Company?

This really comes down to how you prefer to shop and how complex your situation is.

Going directly to an insurer is simple and fast, but you're only seeing their products. It’s like only visiting one store at the mall—you might find something good, but you don’t know what else is out there.

An independent agent or broker, on the other hand, works with a bunch of different insurers. They can shop the market for you, often finding options you wouldn't have discovered on your own. For anyone with a unique health history or specific needs, a good agent is worth their weight in gold.

What if My Health Gets Better After I Buy a Policy?

Life happens, and sometimes for the better! If you’ve made a significant health improvement—like quitting smoking for a year or losing a lot of weight—you might be able to lower your premiums.

You can ask your current insurer for a "reconsideration" of your health rating, usually after one or two years. They'll review your new status and potentially offer you a better rate.

Another option is to simply apply for a new policy elsewhere. If you get a better offer, you can accept it and then cancel your old policy once the new one is officially in place.

At My Policy Quote, we do the heavy lifting for you, bringing quotes from top insurers right to your screen. You get clarity, not confusion.

Find the peace of mind your family deserves. Start your free comparison today at https://mypolicyquote.com.