When it comes to Medicare, you’ll hear a lot of new terms. But few are as important as "creditable coverage."

Getting this one right can save you from a lifetime of penalties. So, what is it?

Think of it as a "hall pass" from Medicare. In simple terms, creditable coverage is any prescription drug plan—like one from your job or the VA—that is considered at least as good as a standard Medicare Part D plan. If you have it, you can delay signing up for Part D without getting into trouble later on.

Decoding Creditable Coverage and Why It Matters

This is especially critical if you plan to keep working past 65 or have other drug coverage when you first become eligible for Medicare.

Medicare’s goal is to make sure everyone has solid prescription drug coverage. If you decide to wait on Part D, having creditable coverage is your proof that you’re not going without. It shows you’re responsibly covered elsewhere.

What Does This Mean for You?

So, why does Medicare care so much about this? Because it protects both you and the system.

Having creditable coverage gives you three huge advantages:

- You Avoid the Penalty: This is the big one. It protects you from the permanent Part D Late Enrollment Penalty, which can add up month after month, for the rest of your life.

- You Get Flexibility: You don’t have to drop a great employer or union plan just because you turned 65. You can keep the coverage you know and trust.

- You Ensure a Smooth Transition: When you eventually do retire or lose your other coverage, you can switch over to a Part D plan without a hitch (and without a penalty).

For anyone figuring out their options as they approach 65, understanding how your current plan stacks up is a must. You can learn more in our guide on health insurance before Medicare. It's all about making these complex ideas easy to grasp, which is why we focus on simplifying complex insurance concepts for clearer communication.

Creditable Coverage At a Glance

To make it even clearer, here’s a quick summary of what creditable coverage means for your Medicare decisions.

| Concept | What It Means for You |

|---|---|

| The "Hall Pass" Rule | Your current drug plan is as good as Part D, so you can delay enrolling without a penalty. |

| Penalty Protection | It’s your ticket to avoiding the permanent Part D Late Enrollment Penalty. |

| Proof of Coverage | You must receive a notice from your plan each year confirming your coverage is creditable. |

| Seamless Transition | When your other coverage ends, you get a Special Enrollment Period to sign up for Part D. |

Ultimately, knowing your coverage is creditable gives you peace of mind. It allows you to make healthcare choices on your own timeline, not one forced on you by the calendar.

The Hidden Cost of Ignoring Creditable Coverage

Overlooking the rules around creditable coverage isn’t just a simple paperwork oversight—it’s a mistake that can permanently eat into your retirement budget. The consequence is the Medicare Part D Late Enrollment Penalty (LEP), a fee that gets tacked onto your monthly premium for as long as you have prescription drug coverage.

Think of it as a late fee on a recurring bill that never, ever goes away. For every single month you go without creditable coverage after you’re first eligible for Medicare, the penalty grows. This isn’t a one-time charge; it’s a lifelong addition to your healthcare costs, slowly chipping away at your hard-earned savings. The financial hit can be serious, much like the importance of proper planning for long-term nursing care costs down the road.

How the Penalty Adds Up

So how does this penalty actually work? It's calculated as 1% of the national base beneficiary premium for each full month you were eligible but didn’t have Part D or other creditable coverage. While 1% might not sound like much at first, it snowballs faster than you’d think.

For example, going just 24 months (two years) without creditable coverage means your future Part D premium will be permanently jacked up by 24%. And because this penalty is recalculated every year, it can keep increasing as the national base premium rises.

Let’s put some real numbers to this to see the impact.

Calculating the Lifetime Cost

Imagine someone puts off enrolling in a drug plan for 30 months and doesn't have any other creditable coverage during that time. Here’s a quick breakdown of the math:

- Penalty: 30 months x 1% = a 30% penalty

- National Base Premium (Example): Let's use an approximate figure of $34.70.

- Monthly Penalty: 30% of $34.70 = $10.41 per month

That extra $10.41 might not seem like a deal-breaker, but it adds up to $124.92 every year. Over a 20-year retirement, that single oversight would cost you nearly $2,500. As the official Medicare website explains, even a 12-month delay can lead to a significant penalty that sticks with you for life. You can read the full details about the late enrollment penalty on CMS.gov.

How to Confirm Your Plan Is Creditable

Figuring out if your current drug plan is actually creditable coverage shouldn't be a guessing game. Thankfully, it’s not. Your insurance provider is legally required to give you a straight answer.

Every year, usually before October 15, your plan has to send you a document called a Notice of Creditable Coverage. This letter explicitly states whether your prescription drug plan is, on average, just as good as a standard Medicare Part D plan.

When you get that notice, keep it somewhere safe. You'll need it as proof to avoid getting hit with a late enrollment penalty when you eventually sign up for Part D.

Finding the Proof You Need

If you've misplaced your notice or just can't find it, don't sweat it. Your first move is to get in touch with your plan administrator directly.

- For plans through work: Reach out to your HR department or benefits manager.

- For union or retiree plans: The plan administrator is who you need to contact.

- For individual plans: Just call the customer service number on your insurance card.

Ask them a direct question: "Is my prescription drug coverage considered creditable for Medicare Part D?" They have to tell you. If you need it, ask them to send another copy of the official notice for your records. For a closer look at this whole process, our guide on how to verify insurance coverage breaks down the steps even further.

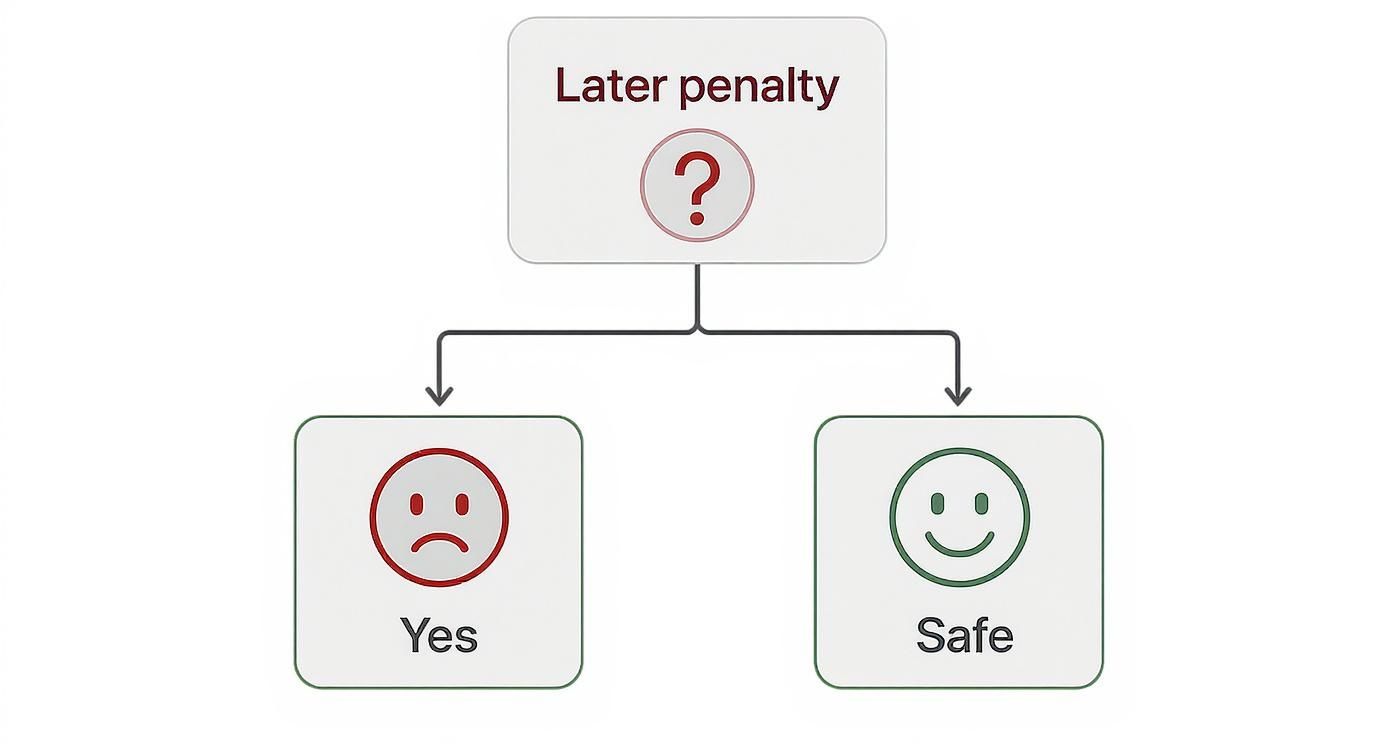

This simple visual makes it crystal clear why having creditable coverage is so important.

As you can see, knowing your status is a critical fork in the road. One path leads to costly penalties, and the other keeps your money in your pocket. Taking a few minutes to check on your plan’s status now can save you from a lifetime of paying more than you have to.

Real-World Examples of Creditable Coverage

Knowing the definition of creditable coverage is one thing, but seeing how it applies to actual insurance plans makes it all click. Let’s be honest, not all health insurance is created equal, especially when it comes to prescription drugs.

The last thing you want is to assume you're covered, only to find out your plan doesn't meet Medicare's standards. So, let's break down which types of coverage usually make the cut—and which ones might leave you exposed to penalties.

Plans That Almost Always Qualify

Some insurance plans are built to be comprehensive, and their drug coverage almost always counts as creditable. If you have one of these, you're likely in good shape, but you should still double-check the notice your plan sends you each year.

- Employer or Union Group Health Plans: Most drug plans from large employers and unions are robust enough to easily meet Medicare's requirements.

- Veterans Affairs (VA) Coverage: The prescription drug benefits you get from the VA? That’s considered creditable coverage.

- TRICARE: This health program for military members, retirees, and their families also provides creditable drug coverage.

Heads up: A common mistake is thinking any plan from a big company is automatically creditable. While it's usually true, it's not a guarantee. The only way to be 100% sure is to check that official notice from your plan.

Here's a statistic that drives the point home: in 2023, about 85% of plans from large employers (with 500+ employees) met the standard. For small employers, that number dropped to just 60%. You can see how CMS standards are evolving on OneDigital.com.

Plans That Often Don't Make the Cut

On the flip side, some plans are less likely to offer drug benefits as good as Medicare Part D. If you're covered by one of these, you need to be extra vigilant and check your plan’s details carefully.

This is especially true for plans you buy on your own, since the benefits can vary dramatically. For a closer look at how these differ, check out our guide on individual vs group health insurance.

Keep an eye on these:

- Some Individual Health Plans: A plan you bought on the health insurance marketplace might not have drug coverage that meets the creditable standard.

- High-Deductible Health Plans (HDHPs): Sometimes, an HDHP’s prescription deductible is so high that it falls short of what Medicare requires.

- Discount Cards: This is a big one. Prescription drug discount cards are not insurance and will never count as creditable coverage.

Creditable vs Non-Creditable Coverage Sources

To make it even clearer, here’s a quick comparison of common insurance sources and whether they typically qualify.

| Type of Coverage | Typically Creditable? | Key Considerations |

|---|---|---|

| Large Employer Group Plan | Yes | Almost always meets the standard, but always verify. |

| Small Employer Group Plan | Maybe | Less likely than large group plans; check your notice. |

| TRICARE / VA Coverage | Yes | Considered creditable by Medicare. |

| COBRA | Yes | Continues your former employer's group plan, so it's usually creditable. |

| Individual Health Plan (Marketplace) | Maybe | Varies by plan; you must confirm with the insurer. |

| High-Deductible Health Plan (HDHP) | Maybe | Depends on the deductible and plan structure. |

| Prescription Drug Discount Card | No | This is not insurance and offers no protection from penalties. |

Knowing where your plan stands isn't just a small detail—it's the key to avoiding a lifetime of late enrollment penalties when you eventually sign up for Part D. Always read your mail and don't be afraid to call your plan administrator to ask directly.

What to Do When Your Coverage Ends

Life doesn’t stand still. Big changes like retiring or switching jobs often mean saying goodbye to your old health plan. When that happens, a critical window opens up. Acting fast is the only way to avoid a permanent late enrollment penalty.

The moment your employer or union coverage ends, the clock starts ticking on your Special Enrollment Period (SEP). Think of it as a 63-day grace period. It’s your one shot to enroll in a new Medicare Part D plan without any negative marks on your record.

Letting that deadline pass is a mistake you’ll pay for—literally. If you go more than 63 consecutive days without either a Part D plan or another form of creditable coverage, Medicare will hit you with the Late Enrollment Penalty. That penalty gets added to your monthly premium for the rest of your life.

Your Action Plan

To make sure your transition is seamless, here are three simple steps to take as soon as you know your coverage is ending:

- Mark Your Calendar: Find the exact date your current coverage stops. Your 63-day SEP countdown begins the very next day.

- Compare Part D Plans: Start looking into the Medicare Part D plans available in your area. You’ll want to compare their costs, drug lists (formularies), and which pharmacies are in their network to find the right fit.

- Enroll Before It’s Too Late: Pick your new plan and get signed up well before that 63-day window slams shut.

A lot of people think they can just wait for the annual Open Enrollment Period. But if you lose your coverage mid-year, you must use your SEP to avoid the penalty.

Navigating insurance after a job change can feel complicated, and you might be looking at other options like COBRA for retirees. By understanding how your SEP works, you can handle this change with confidence and protect your finances for the long haul.

Common Questions About Creditable Coverage

Let's clear up a few common scenarios you might run into with creditable coverage.

What if I Keep My Creditable Plan?

If you get a notice saying your current drug plan is creditable and you're happy with it, you can relax. You don’t have to do a thing. You can safely put off enrolling in Medicare Part D without worrying about a penalty later on. Just make sure to file that notice away—you'll need it as proof when you eventually do sign up.

What Happens if I Lose My Creditable Coverage?

Life happens. Maybe you're leaving a job or your plan changes. When you lose that creditable coverage, a special window opens up for you. You get a 63-day Special Enrollment Period to sign up for a Medicare Part D plan. It’s absolutely critical to enroll during this window. If you miss it, you could face a permanent late enrollment penalty.

Is COBRA Considered Creditable Coverage?

Yes, in most cases, it is. COBRA is really just an extension of the same health plan you had with your employer, so the drug coverage is usually still considered creditable. But remember, the clock starts ticking the moment your COBRA coverage ends. That’s when your Special Enrollment Period begins, giving you a chance to switch to Part D.

Can I Have an Employer Plan and Part D at the Same Time?

You technically can, but it’s rarely a good idea. If your employer plan is already creditable, paying for a Part D plan on top of it is often just a waste of money. It also creates a confusing mess trying to figure out which plan pays first. It's almost always simpler and more cost-effective to stick with one primary source for your drug coverage.

Trying to piece all this together can feel overwhelming, but you're not in it alone. The experts at My Policy Quote are here to cut through the confusion and give you clear, straightforward advice to find a plan that actually fits your life. Explore your insurance options with us today!