At its most basic level, a health insurance claim is the bill your doctor's office sends to your insurance company after you've received care. It’s the official request for payment that turns your health insurance policy from a piece of paper into real financial help when you're sick or injured.

What Is a Health Insurance Claim, Really?

Think of it this way: you have a contract with your insurer. You uphold your end by paying monthly premiums, and they agree to cover a big chunk of your medical bills. The claim is the mechanism that activates their side of the bargain. It's the critical link between getting medical treatment and having your insurance pay for it.

This isn't just a formality; it's a formal request for reimbursement for services covered by your plan. Without this step, your insurance coverage would be nothing more than an empty promise. Getting a handle on how claims work is the first, and arguably most important, part of using your health benefits wisely.

To better understand the flow of a claim, it helps to know who the main players are and what they do. Each one has a specific role that keeps the process moving.

Key Roles in the Health Insurance Claim Process

| Participant | Primary Role | Key Responsibilities |

|---|---|---|

| The Policyholder (You) | The Insured Person | Understand your benefits, provide accurate information, and pay your share of costs (deductibles, copays). |

| The Healthcare Provider | The Care Giver | Deliver medical services and submit an itemized bill to the insurer detailing your treatments. |

| The Insurer | The Payer | Review the claim, confirm services are covered under your policy, and pay their portion of the bill. |

Essentially, each party has a job to do to ensure the bills get paid correctly. When everyone does their part, the system works smoothly.

A health insurance claim is really just a structured conversation. It’s a formal message to your insurer that says, "I used a covered medical service, and now it's time to pay the bill as we agreed."

Why Understanding Claims Matters So Much

Getting a firm grasp on the claims process is one of the best ways to manage your healthcare budget and dodge surprise medical bills. When you know how it's supposed to work, you can spot errors and confidently advocate for yourself if a claim is denied or handled incorrectly.

This knowledge is more important than ever. The global health insurance market is expected to nearly double, growing from USD 2.32 trillion in 2025 to an estimated USD 4.45 trillion by 2032. This explosive growth, driven by rising healthcare costs and needs, means the system is only getting more complex. You can learn more about the global health insurance market growth on actupool.com to see the trends for yourself.

By understanding the system, you can make sure you're getting every dollar of value from the premiums you pay. Whether you're a freelancer, a family, or an early retiree, knowing how to navigate the claims process puts you in control. If you're currently weighing your options, take a look at our guide to affordable health insurance options.

Cashless vs. Reimbursement Claims Explained

When you actually need to use your health insurance, your claim will almost always fall into one of two categories: cashless or reimbursement. Knowing the difference is a big deal because it dictates whether you'll need to pay for hospital care out of your own pocket upfront.

Think of a cashless claim as the "easy button" for hospital bills. This option is available when you get treatment at a hospital that's part of your insurer's approved network. Because the insurance company already has a relationship with these hospitals, the whole process is much smoother, which is a blessing during a stressful time.

Instead of you footing the entire bill and waiting to get paid back, the hospital bills your insurer directly. You just need to handle your share, like any deductible or copay, along with charges for things your policy doesn't cover. The hospital and insurer figure out the rest.

The Cashless Claim Advantage

The biggest plus here is the immediate financial relief. You aren't suddenly faced with a massive bill that you have to pay on the spot. This is especially helpful for planned surgeries, where you can get pre-approval from your insurer to make hospital admission a breeze. In an emergency, the hospital’s insurance desk takes over, letting you focus on what really matters—getting better.

But there's a catch: it only works at "network hospitals." This is why it's so important to check the insurer's hospital list when you compare different health insurance plans. A strong network means you'll have more options for convenient, cashless care.

On the other hand, a reimbursement claim works more like getting paid back for a business trip. You pay for all your medical care directly to the hospital first. This usually happens when you choose a hospital that isn't in your insurer's network, or if that specific hospital just doesn't offer a cashless service.

After your treatment, it's on you to collect every single piece of paperwork—original bills, receipts, doctor's notes, lab reports, and the discharge summary. You then send this mountain of documents, along with a claim form, to your insurance company for review.

The core idea of a reimbursement claim is simple: You pay first, and your insurer pays you back later.

When Reimbursement Is Necessary

While it definitely takes more effort and requires you to have the funds available upfront, the reimbursement route gives you the freedom to get care anywhere. The absolute key to a smooth reimbursement is being incredibly organized with your documents. Don't lose a single receipt!

Here’s a quick breakdown of how they stack up:

Cashless Claims vs. Reimbursement Claims

| Feature | Cashless Claim | Reimbursement Claim |

|---|---|---|

| Payment Flow | Insurer pays the hospital directly. | You pay the hospital first, then the insurer pays you back. |

| Upfront Cost | Minimal; only your deductible or copay. | You must pay the full medical bill. |

| Hospital Choice | Limited to the insurer's network hospitals. | Any hospital of your choice. |

| Paperwork | Less for you; the hospital handles most of it. | You are responsible for collecting and submitting all documents. |

| Best For | Planned procedures and emergencies at network hospitals. | Treatment at non-network hospitals or specialized clinics. |

At the end of the day, both systems are just different ways to access the benefits you're paying for. Understanding how each one works helps you prepare for any situation, so you can manage your health expenses without unnecessary stress and get the most out of your insurance coverage.

From Paper Trails to Digital Claims

To really get why today’s claims system works the way it does, it helps to rewind the clock. Not so long ago, filing a health insurance claim was a frustrating ordeal, buried under a mountain of paperwork. Picture this: your doctor fills out a multi-page form by hand, pops it in the mail, and then everyone waits. And waits. Weeks—or even months—could go by before a response came.

This old-school manual system was a recipe for delays and mistakes. A simple typo, a misplaced decimal point, or a lost envelope could bring the whole process to a screeching halt. The result was a confusing mess of long delays and communication gaps between you, your doctor, and the insurance company. It was a world of paper trails, postage stamps, and a whole lot of patience.

Thankfully, the entire process has been completely reimagined. The move from paper to pixels wasn't just a small tweak; it has fundamentally reshaped how claims are handled, making things better for everyone involved.

The Rise of the Digital Claim

The modern era of claims is all about speed, accuracy, and security—and it's all driven by technology. Instead of snail mail, your doctor's office now submits most claims electronically, often in just a few seconds. This digital leap forward is thanks to a few key breakthroughs.

- Electronic Health Records (EHRs): These are the digital versions of your medical chart. They let providers pull the right treatment codes and patient info instantly, which cuts down on human error dramatically.

- Standardized Digital Formats: Today, all insurers agree to use the same electronic formats for claims. Think of it as everyone agreeing to speak the same digital language, which helps information flow smoothly from one system to another.

- Automated Review Systems: Insurance companies use smart software to automatically scan claims for completeness, accuracy, and coverage details. This system can flag potential problems for a human to look at almost immediately.

The way a health insurance claim works has always mirrored bigger changes in healthcare and technology. Back in the mid-20th century, claims were nothing but manual paper forms, a system that caused major headaches and mistakes. But as digital submissions and automated platforms became the norm, processing times plummeted. Now, many claims get sorted out in a matter of days. You can dive deeper into how tech is pushing the industry forward in these 2025 global healthcare executive outlooks on deloitte.com.

This transition from a physical paper trail to a secure digital pathway is the single biggest reason why a modern health insurance claim is so much more efficient and reliable than its predecessor.

What This Evolution Means for You

So, what does all this mean for you, the policyholder? It means faster payments to your doctors, quicker reimbursements in your pocket, and fewer frustrating errors holding things up. The whole system is more transparent, too. Many insurers even have online portals where you can track your claim's status in real-time, from submission to payment.

Understanding this history shows that the system we have today was built for efficiency—a direct solution to the slow, error-prone ways of the past. For anyone who manages their own coverage, like freelancers or small business owners, this streamlined process is a game-changer. If that's you, our guide on health insurance for the self-employed has advice geared specifically for your situation. Ultimately, this progress helps you focus more on your health and less on the paperwork.

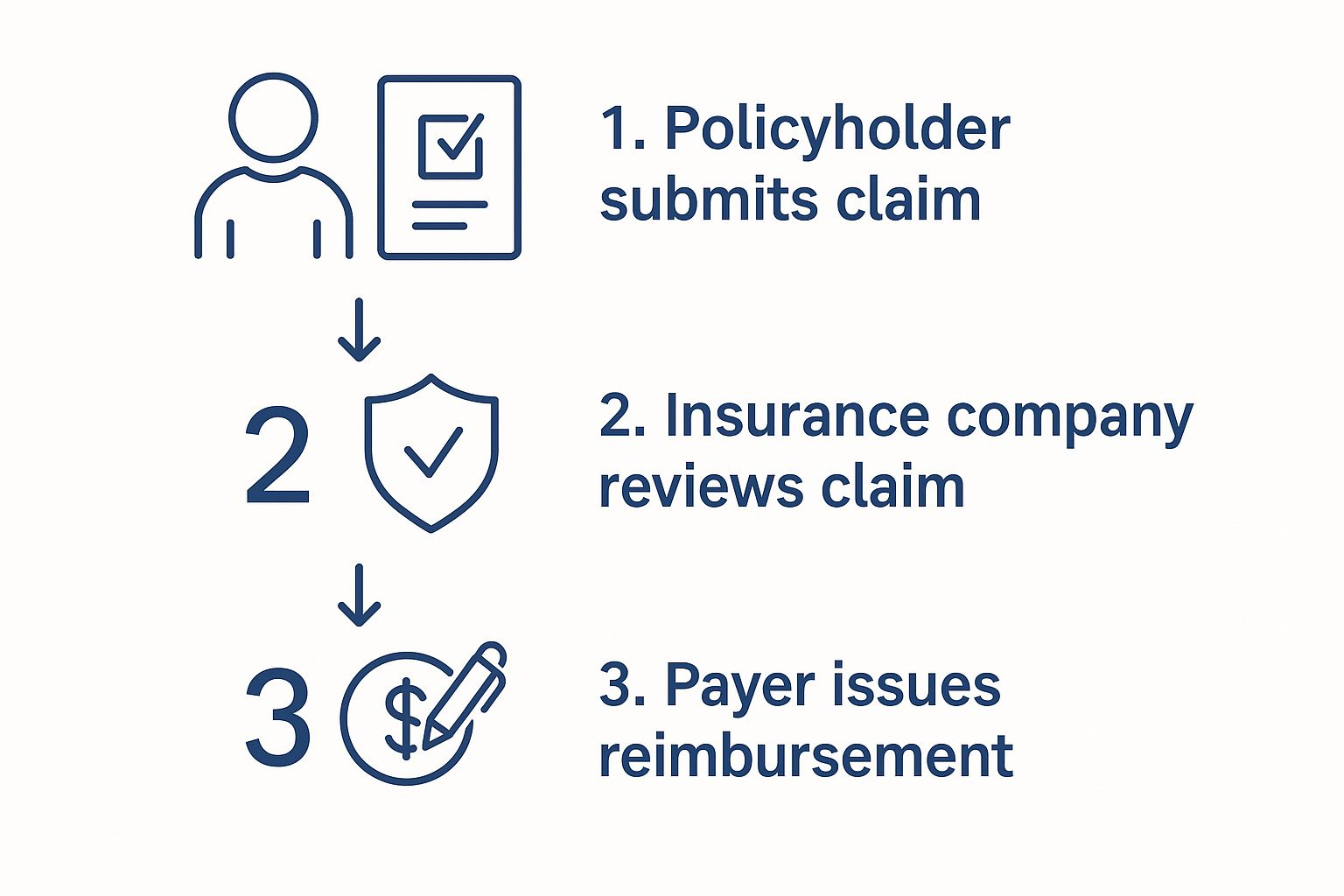

A Step-by-Step Guide to Filing Your Claim

Alright, so you understand what a health insurance claim is and the different ways it can work. But theory is one thing—actually filing a claim is where the rubber meets the road. Let's walk through the entire process, step by step, so you have a clear roadmap for both cashless and reimbursement claims. Getting this right from the start is the best way to avoid mistakes and make sure your policy works for you when you need it most.

This whole journey can really be boiled down to three main phases, which you can see here:

As the graphic shows, it all starts with you submitting the claim. From there, your insurer reviews everything, and finally, payment is made. Your role in kicking things off correctly is absolutely critical.

Stage 1: Before Your Medical Treatment

When it comes to any planned medical care, your first move should always be to get in touch with your insurer. This is non-negotiable, especially if you're hoping for a smooth cashless experience at a network hospital.

-

Secure Pre-Authorization: Before any scheduled hospitalization or procedure, you (or the hospital's staff) must get pre-authorization. Think of this as a green light from your insurance company, confirming that the treatment is medically necessary and covered under your plan. Skipping this step is a common reason for claims getting rejected down the line.

-

Confirm the Hospital is In-Network: Don't just assume. Hospital networks can and do change. Take a minute to call your insurer or check their website to confirm the facility is still on their approved list. This simple check can save you from a massive headache and an even bigger bill.

-

Understand Your Share of the Cost: Get a clear picture of what you'll be expected to pay out of pocket. Ask about your deductible, any copayments, and coinsurance amounts so you aren't caught off guard by the final costs.

Stage 2: Gathering Your Documentation

Whether you're filing for a cashless settlement or a reimbursement, paperwork is king. Your mission is to build a complete and flawless file documenting your medical care. Why? Because disorganized or missing documents are one of the biggest culprits behind delayed or denied claims.

You'll almost certainly need to have these items ready:

- A Completed Claim Form: This is the official starting point. Fill it out carefully and legibly, and double-check that your policy number and personal details are perfect.

- Original Medical Bills and Invoices: You need every single itemized bill—from the hospital, the doctors, the labs, and any specialists. Each one needs to break down the specific services you received.

- Payment Receipts: This is essential for reimbursement claims. You have to provide proof that you've already paid the bills yourself.

- The Hospital Discharge Summary: This is a crucial document that gives a complete overview of your diagnosis, the treatment you underwent, and your doctor's follow-up advice.

- All Diagnostic and Lab Reports: Keep copies of everything. This includes X-rays, blood test results, MRI scans, and any other reports related to your condition.

- Doctor's Prescription: A copy of the original prescription that authorized your treatment or medications is often required.

Pro Tip: Make copies of every single document before you submit anything. Scan them to a secure folder on your computer or make physical photocopies. If your paperwork gets lost in the mail or misplaced, this backup will be a lifesaver.

Stage 3: Submitting and Following Up

Once your document fortress is built, it's time to submit the claim and stay on top of it. The "how" depends on your insurer—some have slick online portals for digital uploads, while others still rely on physical mail.

For Cashless Claims: The hospital's insurance desk (often called the TPA desk) will do most of the heavy lifting. Once you provide your pre-authorization approval and insurance card, they typically handle the submission for you.

For Reimbursement Claims: The responsibility is all yours. You need to gather that complete file of documents and send it to your insurer. Pay close attention to the submission deadline; you usually only have a specific window of time after being discharged to get it in.

After you've sent everything off, don't just sit back and cross your fingers. Your insurer will give you a claim reference number. Use it! Track the status of your health insurance claim on their website or by calling the customer service line. A little proactivity here can help you spot and resolve potential issues early, keeping the whole process moving smoothly.

Why Claims Get Denied and How to Avoid It

You’ve done the hard part—you picked a health insurance plan and you're using your benefits. So getting a notice that your claim has been denied can feel like a punch to the gut. It's frustrating, stressful, and immediately brings up worries about how you're going to pay for your care.

The first thing to know is that this happens, and understanding why is the best way to prevent it from happening again.

Rejection vs. Denial: What’s the Difference?

Before we dive deeper, it's really important to know whether your claim was rejected or denied. They sound similar, but they mean very different things.

A rejection is usually just a temporary hiccup. Think of it like a letter getting returned because of a typo in the address. It’s often caused by a simple clerical error—your name is misspelled, a policy number is wrong, or the provider used an outdated billing code. The good news is, these are almost always fixable. Once the mistake is corrected, the claim can be resubmitted and processed.

A denial, on the other hand, is a much more firm "no" from your insurance company. They've reviewed the claim and have decided not to pay for the service based on the rules of your specific policy. It’s a formal decision, but it's not necessarily the final word. You have the right to challenge it.

To make this crystal clear, let's break down the key differences.

Claim Rejection vs Claim Denial What You Need to Know

This table shows you at a glance how to tell a rejection from a denial and what your immediate next step should be.

| Aspect | Claim Rejection | Claim Denial |

|---|---|---|

| Reason | Usually due to fixable administrative errors (e.g., typos, missing data). | Based on a final coverage decision (e.g., service not covered, lack of medical necessity). |

| Status | The claim has not been processed. | The claim has been processed and refused. |

| Next Step | Correct the error and resubmit the claim for processing. | File a formal internal appeal to have the decision reviewed. |

Knowing which situation you're in helps you take the right action without wasting time or energy.

Common Reasons Your Claim Might Be Denied

While a denial can feel personal, the reason behind it usually falls into a handful of common categories. If you know what these pitfalls are, you can often avoid them completely.

Here are the most frequent culprits:

- The Service Isn't Covered: Every plan has a list of "exclusions"—things it won’t pay for under any circumstances. These often include cosmetic surgeries or treatments considered experimental. Always check your policy documents before getting care to see what’s on that list.

- Lack of Pre-Authorization: This is a big one. Many plans require you to get their approval before you have a specific test or procedure, like an MRI or a planned surgery. If you skip this step, they can deny the claim, even if the procedure itself would have been covered.

- Out-of-Network Provider: If your plan has a network of doctors and hospitals, going outside that network for care is one of the fastest ways to get a denial. Always confirm a provider is in-network before you make an appointment.

- Filing Deadline Missed: Insurance companies have strict deadlines for submitting claims, often 90 to 180 days from the date you received the service. If you or your provider submit the paperwork too late, it's often an automatic denial.

- Lapsed Coverage: A claim will always be denied if your policy wasn't active when you received care. This can happen if a premium payment was missed. Even a brief health insurance gap in coverage can lead to uncovered medical bills.

What to Do If Your Claim Is Denied

A denial is not the end of the line. You have a legal right to appeal the decision.

Here’s a startling fact: a KFF analysis found that in 2023, insurers denied nearly one in five in-network claims. Yet, less than 1% of people who were denied actually appealed. Don't let a denial intimidate you into inaction.

Here’s your game plan:

- Read Your Denial Letter Carefully. Your insurer is required to send you an Explanation of Benefits (EOB) that details exactly why they denied the claim. This is your road map.

- Gather Your Evidence. Collect everything related to the claim: your policy documents, the EOB, your medical records, the original bills, and any notes from conversations with your doctor or insurer.

- Start an Internal Appeal. This is a formal request for the insurance company to take another look and review its decision. You typically have up to 180 days from the date you received the denial to file this appeal.

- Escalate to an External Review. If the insurance company still says no after the internal appeal, you can take your case to an independent, third-party reviewer for an unbiased look.

By staying organized and being persistent, you give yourself a much better shot at getting the denial overturned and having your benefits cover your care, just like they're supposed to.

The Bigger Picture: How Claims Shape the Insurance Industry

When you submit a health insurance claim, it's easy to see it as a simple, one-off transaction between you and your provider. But in reality, that single claim—whether for a routine check-up or a major surgery—becomes a critical piece of data in a massive financial ecosystem. It joins millions of others, and together, they directly shape how the entire insurance industry works.

A good way to think about it is to picture an insurance company’s funds as a large, shared pool of money. The premiums paid by every policyholder are the streams flowing in, while the costs of all approved claims are the streams flowing out. Your individual claim might feel like just one drop leaving the pool, but the combined total of all those drops determines how much money needs to be kept in that pool at all times.

This constant outflow means insurers are always engaged in a complex balancing act. They have to use the total volume and cost of claims to predict future healthcare spending, which is how they set premium prices for everyone next year.

How Claims Data Drives Premium Pricing

The link between the claims filed this year and the premium you'll pay next year is incredibly direct. Insurers don't just pull their prices out of thin air; they rely on sophisticated risk models that are fueled by real-world claims data. These models are constantly analyzing past claims to spot trends and forecast future costs.

A few key factors, all brought to light by claims data, have a huge impact:

- Healthcare Inflation: When claims data shows that the cost of medical procedures, prescription drugs, and hospital stays is going up, insurers have to adjust premiums upward to cover these higher anticipated expenses.

- Increased Utilization: If the data reveals that people are going to the doctor or using more healthcare services than in the past, premiums must rise to replenish the funds being paid out more frequently.

- Demographic Shifts: Claims can also highlight the financial impact of broader societal changes, like an aging population or a rise in chronic conditions, both of which lead to more frequent and more expensive claims.

You can see this playing out on a global scale. The insurance industry managed roughly EUR 7.0 trillion in worldwide premiums in 2024, and health insurance is a huge piece of that pie. Global premium income grew by 8.6% in 2024, driven in part by the rising cost and number of health claims fueled by medical inflation and new technologies. For a deeper dive, you can explore a detailed analysis of these global insurance market trends on allianz.com.

Your health insurance claim is more than just a bill. It's a piece of information that helps insurers measure risk, predict costs, and ultimately decide what everyone will pay for coverage next year.

At the end of the day, your claim is part of a massive, continuous cycle. The payments for today’s medical care become the data that sets the price for tomorrow's insurance policies. Understanding this bigger picture shows that the claims process isn't just about getting one bill paid—it's about keeping the entire system that provides health coverage for millions of people financially stable.

Got Questions? We’ve Got Answers on Health Insurance Claims

Even when you know the basics, the real world of health insurance claims always throws a few curveballs. Let's tackle some of the most common questions that pop up. Think of this as your practical, no-nonsense guide to getting through the process smoothly.

How Long Will I Be Waiting for My Claim to Go Through?

This is the big one, isn't it? The timeline for a health insurance claim really depends on the path you take—cashless or reimbursement. Knowing the difference helps you set realistic expectations.

- Cashless Claims: These are the speed demons of the insurance world. Because the hospital and your insurer are talking directly, often with a pre-approval already in hand, you can expect things to be squared away quickly. Most are settled within 24 to 48 hours after you're discharged.

- Reimbursement Claims: This route takes a bit more patience. You're the one gathering and sending in the paperwork after you've already paid. Once your insurer has everything, they generally take about 15 to 30 days to go through it all and send you the money.

Keep in mind, a really complicated case might take longer. If the clock is ticking past these typical windows, don't hesitate to check in with your insurer.

Help! I Lost My Medical Bills. What Now?

It’s a moment of pure panic: you’re ready to file for reimbursement, and the original bills are nowhere to be found. Take a deep breath—this is almost always solvable.

Your first move should be to call the hospital or clinic’s billing department right away. They deal with this all the time and can issue certified duplicate copies of your itemized bills and payment receipts. Just let them know it’s for an insurance claim, and they’ll get you what you need to move forward.

How Do I Keep Tabs on My Claim's Progress?

Wondering what's happening with your claim? Most insurers have made this part easy with online portals and mobile apps. When a claim is filed, you’ll get a unique claim reference number. Hold onto it!

Think of your claim reference number like a tracking code for a package. You can use it to log into your insurer's portal and see the status in real time—whether it's "received," "in review," or "approved."

If you’re not the techy type or your insurer’s portal isn’t great, a quick phone call to customer service with that reference number will get you the same update.

What in the World Is a Third-Party Administrator (TPA)?

You’ll often hear the term "TPA" at the hospital’s insurance desk. A Third-Party Administrator is an organization your insurance company hires to manage the claim process on their behalf. In fact, nearly two-thirds of American workers with health coverage are in plans that use a TPA.

They're the ones on the ground handling the logistics, like:

- Checking your policy to confirm you’re covered.

- Arranging pre-authorizations for cashless treatments.

- Collecting and processing all the necessary paperwork.

Essentially, the TPA is the operational partner for your insurer. They don't have the final say on paying a claim—that’s up to the insurance company—but they play a huge role in making sure everything runs as it should.

Figuring out health coverage can feel overwhelming, but you're not on your own. At My Policy Quote, we’re experts at matching you with the right plan for your life, whether you're self-employed, retiring early, or covering the whole family. Get a clear, no-hassle quote today and take control of your healthcare journey.