Ever heard of a health plan that acts like a last-resort safety net? That’s catastrophic health insurance in a nutshell. It’s a unique type of plan built for a very specific purpose: to protect you financially from a true medical disaster.

These plans come with very low monthly premiums but an extremely high deductible. They’re the bare-bones option for people who want a shield against worst-case scenarios—like a major accident or a sudden, severe illness—but don’t anticipate needing much routine medical care.

Unpacking The Basics Of Catastrophic Health Insurance

Think of it like car insurance that only covers a total wreck. You wouldn't file a claim for a routine oil change or a new set of tires, but you'd be incredibly relieved to have it if you were in a serious collision.

A catastrophic health plan works the same way. It isn't meant for your annual flu shot or a sprained ankle. It’s designed to kick in and save you from six-figure medical bills after a sudden hospitalization or a life-altering diagnosis. The trade-off is simple: you pay less each month in exchange for covering almost all of your medical costs out-of-pocket until you hit a very high annual deductible.

What Does "High Deductible" Really Mean?

The deductible is the amount you have to pay for your own medical care before your insurance company starts chipping in. With a catastrophic plan, we’re not talking about a few hundred dollars. We’re talking thousands.

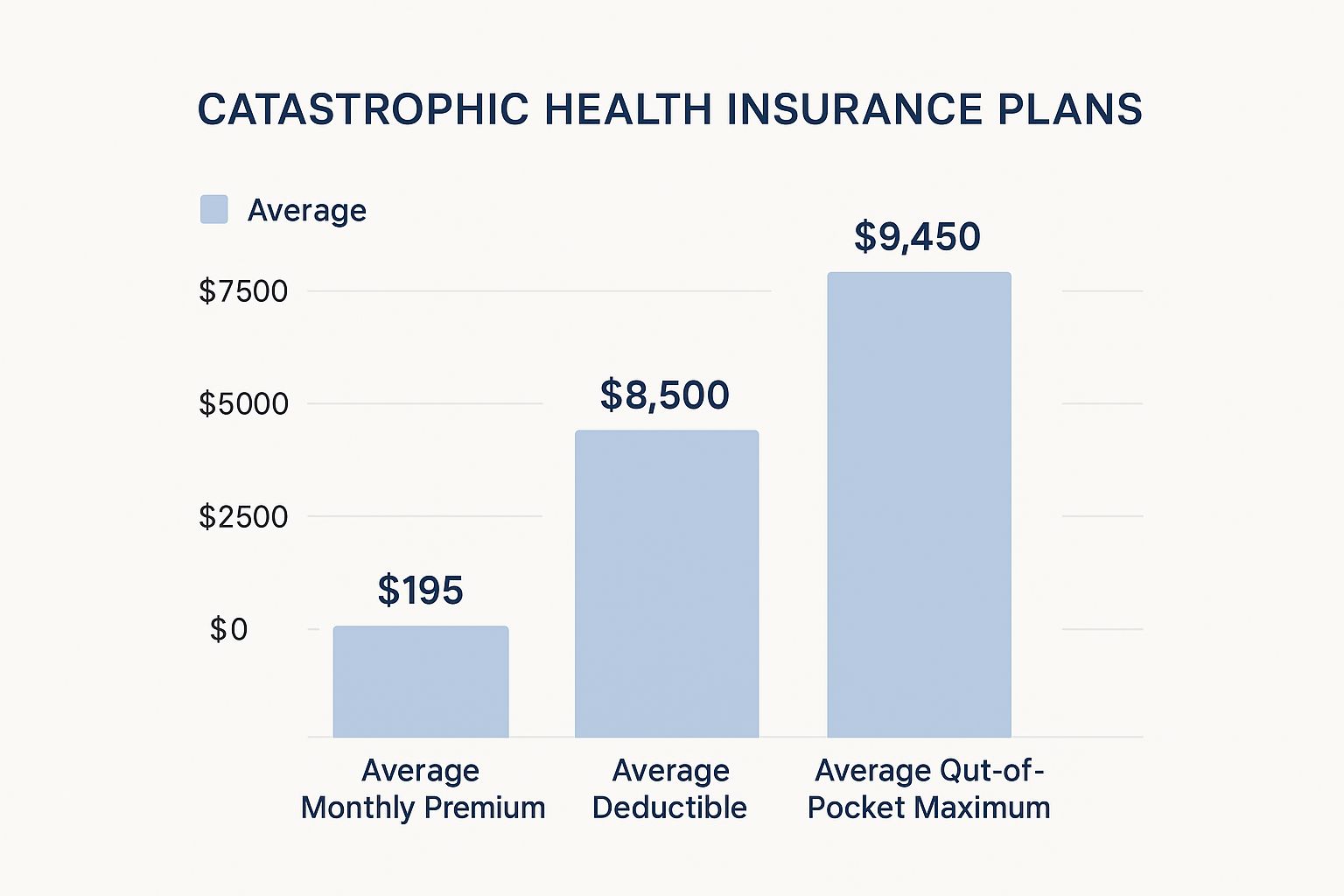

The Affordable Care Act (ACA) sets this high bar each year. For 2024, the deductible for a catastrophic plan is $9,450 for an individual and a whopping $18,900 for a family.

This means you are on the hook for every single dollar of your medical bills up to that massive number. But once you've spent that much, your plan steps in and covers 100% of your essential health benefits for the rest of the year.

Catastrophic Health Insurance At A Glance

To make it even clearer, here’s a quick summary of what you can expect from one of these plans.

| Feature | Typical Characteristic | What This Means For You |

|---|---|---|

| Monthly Premium | Very low, often cheaper than Bronze plans. | Your monthly budget gets a break, but you take on more financial risk for medical care. |

| Annual Deductible | Extremely high (e.g., $9,450 for an individual). | You'll pay for nearly all medical services out-of-pocket until you meet this amount. |

| Routine Care | Not covered until the deductible is met. | Doctor visits for minor illnesses or injuries will be paid for entirely by you. |

| Preventive Care | Covered at 100% before the deductible. | You can still get your annual check-up, certain screenings, and vaccinations for free. |

| Primary Care Visits | First three visits are covered for free. | You have some access to a primary care doctor without dipping into your pocket. |

| Emergency Protection | Kicks in after the deductible is met. | Protects you from financial ruin in the event of a major accident or severe illness. |

Basically, it's a high-risk, high-reward setup designed for specific situations.

Key Features Of A Catastrophic Plan

While the coverage feels minimal before you meet that deductible, these plans do have a few required benefits to give you a baseline of care. If you’re considering this path, it’s vital to understand what you’re getting. You can dive deeper into the specifics in our complete guide to catastrophic health insurance plans.

Here are the highlights:

- Low Monthly Premiums: This is the biggest draw. The monthly cost is usually much lower than other Marketplace plans, even Bronze ones.

- Protection from Major Expenses: This is the core purpose. They put a hard cap on what you’d have to pay in a true medical emergency, stopping you from going bankrupt.

- Essential Preventive Care: Even before your deductible is met, catastrophic plans cover certain preventive services at no cost to you. This includes things like health screenings, vaccinations, and your annual wellness visit.

- Three Primary Care Visits: The plans also cover your first three primary care visits of the year for free, giving you at least some access to basic care without cost.

These plans were introduced with the Affordable Care Act back in 2014 for very specific groups—mainly young adults under 30 or people who qualify for a hardship exemption. While the low premiums are tempting, that sky-high deductible means they aren't the right fit for most people.

Who Can Actually Get a Catastrophic Plan?

Unlike most other health plans you’ll find on the Marketplace, catastrophic health insurance isn't an open-door policy. It’s more like a private club with a very specific guest list. These plans were designed as a safety net for a very narrow group of people, and the rules are strict about who gets in.

So, how do you get on the list? There are really only two ways to qualify for a catastrophic plan. You have to meet one of these two conditions to be eligible.

The Age Requirement

The most straightforward path is based on your age. If you are under 30 years old when you sign up, you’re generally good to go.

The logic here is pretty simple: younger people are, on average, healthier and less likely to need constant medical care. For a young adult, the low monthly premium is a huge plus, offering a backstop for a major, unexpected medical disaster without the high cost of a more comprehensive plan.

As long as you’re 29 or younger, you'll see catastrophic plans as an option when you shop for coverage on the Health Insurance Marketplace. The moment you hit 30, though, this option disappears.

Getting In Through an Exemption

What if you're 30 or older? You're not necessarily out of luck, but the path is a bit more complicated. You’ll need to qualify for what’s called an “exemption.” These are special circumstances, recognized by the government, that let you bypass the age limit.

There are two main types of exemptions:

- Hardship Exemptions: These are for people who’ve recently hit a rough patch in life, making it nearly impossible to afford typical health coverage.

- Affordability Exemptions: This one’s for folks whose income is too low to afford the other health insurance plans available to them.

It's crucial to understand that these exemptions aren't automatic. You have to apply for one through the Health Insurance Marketplace. Only after you get an official approval notice can you enroll in a catastrophic plan.

Let’s take a closer look at what situations might get you an exemption.

Common Hardship and Affordability Scenarios

The government keeps a specific list of what qualifies as a "hardship," and it's all tied to significant life challenges. The official source for applying is always HealthCare.gov.

This screenshot from HealthCare.gov shows the portal where you can start the process of applying for health coverage and seeking exemptions.

This is your first stop. Navigating this site is how you’ll formally find out if your situation meets the government's strict criteria.

You might qualify for a hardship exemption if you've recently gone through something like:

- Homelessness

- Facing eviction or foreclosure in the last six months

- Getting a shut-off notice from a utility company

- Filing for bankruptcy

- Being a victim of domestic violence

- Piling up substantial medical debt that you can't pay

An affordability exemption, on the other hand, is all about the numbers. You can get one if the cheapest plan available to you—whether from the Marketplace or your job—would cost more than a certain percentage of your household income. That percentage changes each year, but the goal is to make sure nobody is completely priced out of having at least some form of health protection.

The High-Stakes Financial Trade-Off

Choosing catastrophic health insurance is a calculated bet. You’re betting on your own good health, hoping you won't face any major medical bills. The insurance company is betting on the exact same thing.

At its core, this is a dramatic trade-off. You get the immediate relief of a super-low monthly premium. In exchange, you accept a massive financial risk: a sky-high deductible that you have to cover all on your own.

Think of it like having access to a huge emergency fund you can't touch. The small monthly premium is your access fee. But for everyday things—a check-up for a nasty cold, a routine prescription—that fund is locked tight. It only opens up when a true crisis hits, like a serious accident or a sudden hospitalization.

Only after you’ve paid thousands of dollars out of your own pocket does the plan finally kick in to save you from financial ruin. It makes your monthly budget look fantastic, but you’d better have a solid savings account to back it up.

Decoding Your Financial Responsibility

The heart of this trade-off is the deductible. It’s the mountain of medical bills you have to climb and pay for yourself before your insurance starts sharing the cost. For 2024, that mountain is $9,450 high for an individual plan.

That number isn't a suggestion; it's a hard stop. Until your own medical spending hits that mark, your plan pays for virtually nothing besides a few specific preventive services. Every single doctor’s visit, lab test, and prescription comes straight out of your wallet.

Let's break it down with a real-world example:

- The Scenario: You slip and break your arm, landing you in the emergency room.

- ER Visit & X-rays: $2,000

- Follow-up with an Orthopedic Specialist: $400

- Physical Therapy (6 sessions): $1,200

- Your Total Bill: $3,600

In this situation, you would be on the hook for the entire $3,600. Your catastrophic plan wouldn't pay a dime because you’re still nowhere near your $9,450 deductible. You'd still have another $5,850 to go before your coverage for most services even begins.

This is the high-stakes part of the deal. You are effectively self-insuring for everything except the absolute worst-case scenarios. The low premium is your reward for taking on that huge upfront risk.

The Out-of-Pocket Maximum: Your Financial Shield

While that deductible sounds terrifying, it isn't an endless pit of spending. Every ACA-compliant plan, catastrophic plans included, has a built-in safety net called the out-of-pocket maximum. This is the absolute most you will have to pay for covered services in a single year.

For catastrophic plans, the deductible and the out-of-pocket maximum are usually the same exact number. For 2024, that’s $9,450 for an individual.

Once your spending on in-network care hits that limit, your plan pays 100% of the costs for covered benefits for the rest of the year. This is what truly makes it "catastrophic" coverage—it puts a hard cap on your financial liability and protects you from a million-dollar hospital bill. This critical feature is often where people start wondering if they are overpaying for insurance; you can learn more by reading our guide on how much you could be overpaying on insurance.

What You Get Before Meeting The Deductible

Okay, so the financial picture isn't completely bleak before you hit that massive deductible. The Affordable Care Act requires all health plans, even catastrophic ones, to provide certain essential benefits at no cost to you.

These perks are designed to keep you healthy and catch problems early, making them incredibly valuable when you’re on a high-deductible plan.

Free Services Included with Catastrophic Plans:

- Three Primary Care Visits: You get your first three visits with a primary care doctor (PCP) each year completely free. This lets you get help for minor issues without getting hit with a bill right away.

- Preventive Care Services: A whole range of preventive services are covered at 100%. This is a huge benefit that many people don't even realize they have.

These free services often include things like:

- Annual wellness check-ups to get a baseline on your health.

- Important immunizations like the flu shot.

- Screenings for high blood pressure, cholesterol, and certain types of cancer.

Understanding this financial trade-off is everything. You're agreeing to handle all routine and moderate medical costs yourself in exchange for a low premium and a firm safety net for a true catastrophe.

How Catastrophic Plans Compare To Other Options

Picking a health plan can feel like wandering through a maze blindfolded. You know there's an exit, but every path looks the same. To really get a handle on catastrophic health insurance, we need to put it side-by-side with the more familiar options on the Health Insurance Marketplace—the Bronze and Silver "metal" tiers.

Think of it like this: your health plan is a financial agreement between you and the insurance company. With plans like Bronze or Silver, the insurer agrees to start helping out with costs relatively early. But a catastrophic plan is different. It’s a much more hands-off arrangement.

Your insurer basically stays on the sidelines for all your routine checkups and minor medical bills. In exchange, you get the lowest possible monthly premium. They only jump in when a true medical disaster strikes. It’s a very specific tool for a very specific job.

Catastrophic Plans Vs. Bronze Plans

On the surface, catastrophic and Bronze plans look like twins. Both have low monthly premiums and high deductibles, which is why they appeal to young, healthy people who don’t expect to see a doctor very often.

But there’s a massive difference hiding in plain sight: subsidies.

Bronze plans are open to everyone, and—this is the important part—they’re eligible for premium tax credits. For someone with a qualifying income, a subsidy could slash the monthly cost of a Bronze plan, making it even cheaper than a catastrophic plan.

Key Takeaway: A subsidized Bronze plan can often be a much better deal than an unsubsidized catastrophic plan. Before you decide, always check if you qualify for subsidies. You might unlock better coverage for less money.

Plus, even though both have high deductibles, the deductible on a Bronze plan is almost always lower than the sky-high one on a catastrophic plan. That means your insurance safety net kicks in sooner if you have an accident or get sick.

The Silver Plan Advantage: Cost-Sharing Reductions

Now let’s talk about Silver plans. They have a secret weapon that catastrophic plans just can’t compete with: cost-sharing reductions (CSRs).

These are extra subsidies, only available on Silver plans for people with lower incomes. They don't just lower your premium; they dramatically reduce your deductible, copayments, and out-of-pocket maximum.

If you qualify, a Silver plan with CSRs can feel like getting Gold or Platinum-level coverage for a Silver-level price. It's a benefit you absolutely cannot get with a catastrophic plan, making a Silver plan the obvious winner if you're eligible.

This image really highlights the trade-off you make with a catastrophic plan. You're swapping that low monthly bill for a much bigger financial responsibility if something goes wrong.

It’s a stark visual reminder: that low premium comes with a very high wall to climb before your insurance starts paying.

Health Plan Showdown: Catastrophic vs. Bronze vs. Silver Plans

When you’re weighing your options, especially if you’re self-employed, seeing the details laid out clearly is crucial. It’s worth exploring all 5 health insurance options for the self-employed to get the full picture.

The choice often boils down to a bigger question about how you want to manage risk and your finances. It's a debate between health insurance vs personal savings and which is better for handling unexpected medical costs.

To make it simple, let's break down the key differences in a table.

| Feature | Catastrophic Plan | Bronze Plan | Silver Plan |

|---|---|---|---|

| Typical User | Healthy individual under 30 or with an exemption. | Healthy individual of any age seeking low premiums. | Individual or family qualifying for subsidies (especially CSRs). |

| Monthly Premium | Lowest possible. | Low, but usually a bit more than Catastrophic. | Moderate, but can be very low with tax credits. |

| Deductible | Extremely high ($9,450 in 2024). | High, but usually lower than Catastrophic. | Lower than Bronze, and can be very low with CSRs. |

| Premium Subsidies | No, you cannot use subsidies. | Yes, eligible for premium tax credits. | Yes, eligible for premium tax credits. |

| Cost-Sharing Reductions | No, not eligible for CSRs. | No, not eligible for CSRs. | Yes, eligible if your income qualifies. |

| Out-of-Pocket Maximum | Very high, same as the deductible. | High, but caps your total spending for the year. | Moderate, and can be significantly lower with CSRs. |

The takeaway here is pretty clear. While a catastrophic plan has the lowest sticker price, it offers the least help and demands the most from your wallet before it kicks in. For most people, a subsidized Bronze or Silver plan provides a much safer and more balanced financial solution.

The Real-World Impact Of Medical Disasters

To really get why catastrophic health insurance exists, you have to think bigger than a single medical bill. Imagine a massive hurricane is about to hit the coast. The storm causes billions in damage, but when the dust settles, insurance only covers a fraction of that cost.

That massive gap between the total damage and what insurance actually pays? It's called the "insurance protection gap." It’s a financial shockwave that rips through entire communities, leaving families and local businesses to handle the fallout all on their own.

A severe health crisis, like a pandemic or a major multi-person accident, works the same way. It's not just about one person—it overwhelms hospitals, drains public resources, and triggers financial devastation that spreads like wildfire.

The Personal Financial Shockwave

When a major health crisis hits you personally, it creates your own private version of that protection gap. A sudden critical illness or a bad accident can rack up medical bills that climb into the hundreds of thousands of dollars. Without the right protection, something like that can erase a lifetime of savings in just a few months.

This is the exact nightmare scenario that catastrophic health insurance is built to stop. It's a safety net—a backstop—that says, "Yes, the initial costs will be high, but there's a hard limit on how bad the financial damage can get."

A single serious accident can be the difference between a manageable financial challenge and complete bankruptcy. The goal of this coverage is to build a firewall against that worst-case outcome, protecting your long-term financial stability.

By putting a cap on your total out-of-pocket expenses for the year, the plan stops a personal health disaster from turning into a lifelong financial one. It closes your personal protection gap.

The Broader Economic Strain

Now, let's zoom back out. This idea of an insurance protection gap isn't just a theory; it’s a global economic problem. For example, global economic losses from natural disasters hit hundreds of billions of dollars every year, but insured losses cover only a tiny part of that. This problem is getting worse as health emergencies tied to large-scale events become more common. You can learn more about these challenges by reading the full research on natural catastrophe trends.

The same logic applies directly to our public health system. When huge numbers of people are hit with medical bills they can’t possibly pay, the ripple effects are massive:

- Hospital Strain: Unpaid medical debt forces hospitals to absorb huge losses. This can lead to service cuts, staff layoffs, and even closures, which hurts the whole community's access to care.

- Increased Debt: Widespread medical debt grinds local economies to a halt because people have no money left to spend on everyday goods and services.

- Systemic Risk: A major health crisis can push public health systems to the brink, forcing massive government bailouts that taxpayers end up funding.

Catastrophic health insurance plays a small but vital role in this big picture. By giving individuals a baseline of financial protection, it helps lower the number of people completely bankrupted by medical costs. In turn, that eases the financial load on the entire healthcare system and the wider economy, making it a critical piece of the puzzle.

Is A Catastrophic Health Plan The Right Choice For You?

Choosing health insurance isn't just about picking a plan. It's a huge financial decision, and with a catastrophic health insurance plan, the stakes are even higher. This is about taking an honest look at your health, your bank account, and how much risk you’re truly comfortable with.

Making the wrong choice here can be incredibly costly. But the right one? It's an affordable safety net that gives you peace of mind. To figure out if this high-deductible plan fits your life, you need to see past the tempting low monthly payment and ask yourself some tough questions.

Who Is A Great Fit For Catastrophic Coverage?

Some people are a perfect match for a catastrophic plan's unique design. It’s built for those who are essentially betting on their good health and have the cash on hand to handle routine medical bills without breaking a sweat.

Think about a catastrophic plan if this sounds like you:

- You are young and generally healthy. You almost never see a doctor outside of an annual check-up and don't have any chronic conditions that need regular care or medication.

- You have a robust emergency fund. This is critical. You must have enough saved to comfortably pay the entire high deductible—$9,450 for an individual in 2024—without falling into debt.

- Your primary goal is preventing bankruptcy. You’re not looking for a plan to cover your sniffles or sprains. Your main worry is a true medical disaster, like a serious accident or a sudden, severe illness, and you want a financial backstop.

This plan is for the financially prepared minimalist who wants protection from the absolute worst-case scenario. It's a calculated risk that pays off when you stay healthy and have savings to back you up.

Who Should Absolutely Avoid This Plan?

Just as there’s an ideal person for this plan, there are also people for whom it would be a financially dangerous mistake. For them, the massive out-of-pocket costs would become unmanageable in a heartbeat, wiping out any savings from the low premium.

You should steer clear of catastrophic coverage if you:

- Manage a chronic condition. If you have an ongoing health issue like diabetes, asthma, or heart disease, you'll be paying for every single appointment, test, and prescription out-of-pocket until you hit that massive deductible.

- Do not have significant savings. If getting a $9,450 medical bill would be a financial nightmare, this plan is not for you. That high deductible isn't just a number; it's a very real and significant risk.

- Qualify for subsidies on the Marketplace. If your income makes you eligible for premium tax credits or cost-sharing reductions, a subsidized Bronze or Silver plan will almost always give you better coverage for a similar—or even lower—final cost.

Deciding on a health plan involves forecasting different financial outcomes and managing risk, a bit like how experts use Monte Carlo simulation financial models to map out possibilities. At the end of the day, a catastrophic plan is a specialized tool. It provides incredible value for the right person but can create serious hardship for the wrong one. Be honest with yourself about your health and your finances to make the smartest choice.

Still Have Questions? Let's Clear Them Up

Even after you've got the basics down, a few specific questions always pop up about catastrophic plans. Let's tackle the most common ones so you can feel completely confident in your understanding.

What if I Have a Chronic Illness?

Technically, you can enroll in a catastrophic plan even if you're managing a chronic condition. But honestly? It's a huge financial gamble.

These plans are built to protect you from worst-case scenarios, not day-to-day care. This means you'll be paying for every single doctor’s visit, every lab test, and every specialist appointment out of your own pocket until you hit that massive deductible. For someone with ongoing health needs, those costs can snowball into an unmanageable mountain of debt, making the low monthly premium feel like a distant memory.

Are My Prescriptions Covered?

This is a big one. With a catastrophic plan, prescription drug coverage is practically nonexistent until your deductible is met. While a few preventive medications might be covered, you should plan on paying the full cash price for most of your prescriptions.

If you rely on daily or monthly medications, this is a dealbreaker. You’d be on the hook for the entire cost of those drugs, which could easily add up to thousands of dollars long before your insurance ever starts to help.

It’s a critical detail. The cost of your medications alone could make a catastrophic plan far more expensive over the year than a more traditional, comprehensive plan.

Can I Use Subsidies to Lower the Premium?

No, and this is a crucial point. Catastrophic health plans are not eligible for premium tax credits (subsidies) or cost-sharing reductions (CSRs). These financial aids, which you find on the Health Insurance Marketplace, are specifically for making more comprehensive plans affordable.

This distinction can change everything. For many people, a subsidized Bronze or Silver plan could actually have a lower monthly payment than an unsubsidized catastrophic plan. It's just one piece of the financial puzzle when planning for your future; if you're looking at the bigger picture of personal finance protection, our guide on term life insurance comparison offers some really valuable perspective.

Always compare the final price you'd pay for a subsidized "metal" plan against the full price of a catastrophic plan. You might be surprised to find that much better coverage is actually the more affordable option.

At My Policy Quote, we cut through the confusion to help you find coverage that fits your life and your budget. Ready to see your options? Visit https://mypolicyquote.com and get the protection you deserve today.