So, you’ve done it. You’ve achieved the dream of retiring early, trading in the 9-to-5 for a life of your own making. But as you close the door on your career, a new one opens: how do you handle health insurance before Medicare starts at age 65?

It’s a critical question, and you’re not alone in asking it. Your main early retiree health insurance options come down to three key paths: ACA Marketplace plans, COBRA, and private insurance. Each one works differently, and the right choice for you depends entirely on your situation.

Charting Your Course Through the Pre-Medicare Gap

Leaving the workforce before you turn 65 means walking away from the employer-sponsored health insurance that most of us rely on. Suddenly, you're faced with a gap in coverage that you're responsible for bridging. It can feel like you've been handed a map to a new city, written in a language you don't quite understand. But with a little guidance, it’s completely manageable.

And this journey is becoming more common than ever. The old days of companies offering generous health benefits to their retirees are quickly vanishing.

In fact, data from 2022 shows that only 12% to 21% of people aged 65 and older still receive retiree health benefits from a former employer. That’s a massive drop from decades past, highlighting just how important proactive planning has become.

This shift means the responsibility now falls squarely on your shoulders. The good news? There are clear, established pathways designed to get you covered.

Your Main Insurance Pathways

Let's break down your core choices. Don't worry about the jargon; think of these as different tools for different jobs. Each one is built to serve a specific need, timeline, and budget. Once you understand their purpose, you can see which one aligns with your retirement vision.

Here are the three primary routes you’ll be looking at:

- ACA Marketplace Plans: For many early retirees, this is the best and most affordable option. These plans are income-based, which means you might qualify for significant government help (called premium tax credits) to lower your monthly payments. The key is to manage your retirement income carefully.

- COBRA Coverage: Think of this as a temporary bridge. COBRA lets you keep the exact same health plan you had with your old employer for up to 18 months. It provides perfect continuity, but there’s a catch: you have to pay 100% of the premium, plus a small administrative fee. It gets expensive, fast.

- Private & Short-Term Insurance: These plans are bought directly from an insurance company. A full private plan might give you a wider choice of doctors but comes without any financial subsidies. Short-term plans are a different beast entirely—they're low-cost, bare-bones policies meant only for true emergencies and carry some significant risks.

To give you a bird's-eye view, we've put together a quick comparison table. Use it as a starting point to see how these options stack up before we dive into the details.

Quick Comparison of Early Retiree Health Insurance Options

This table gives a high-level summary of your main choices. It's a great way to quickly see which path might be the best fit for your circumstances.

| Insurance Option | Best For… | Typical Duration |

|---|---|---|

| ACA Marketplace | Retirees who can manage their income to qualify for subsidies. | Annually, renewable |

| COBRA | Retirees who need short-term coverage and want to keep their exact doctor/plan. | Up to 18 months |

| Private Insurance | Retirees with higher incomes who want broader network choices. | Annually, renewable |

| Short-Term Plans | Healthy retirees needing a temporary, low-cost catastrophic bridge. | 3-12 months |

As you can see, there isn't a single "best" answer—only the one that's best for you. Learning how to secure your health insurance before Medicare is one of the most important steps you'll take in this new chapter. This guide is here to give you the clarity you need to make a confident decision for your future.

Tapping into the ACA Marketplace for Early Retirement

For most people finding their way through the pre-Medicare years, the Affordable Care Act (ACA) Marketplace is the single most powerful tool you have. It can transform health insurance from a crushing expense into something you can actually manage. But here’s the key: you have to know how to use it strategically.

This isn't just about picking a plan from a list. It's about getting your financial life in sync with the Marketplace rules to unlock its true power. For an early retiree, it all boils down to two things: getting your timing right and carefully managing your income.

How to Get In: Your Special Enrollment Period

First off, you don't have to sit around and wait for the annual Open Enrollment period. Leaving a job and losing that employer-sponsored health plan is a big deal, and the government recognizes that. It’s considered a Qualifying Life Event (QLE).

This QLE triggers what’s called a Special Enrollment Period (SEP), which is your personal 60-day window to hop onto the Marketplace and enroll in a new plan. Think of it as an express lane that lets you bypass the usual lines. Missing this 60-day window is a rookie mistake you can't afford to make—you'd have to wait for the next Open Enrollment, potentially leaving you uninsured for months. You have to act fast once your old coverage ends.

The Real Secret to Affordability: Your MAGI

Here’s where the magic really happens for early retirees. The ACA offers Premium Tax Credits (PTCs), which are basically subsidies that can slash your monthly insurance premiums. The size of your subsidy comes down to one number: your Modified Adjusted Gross Income (MAGI).

This is where early retirement gives you an incredible advantage. Unlike your working years, you now have a ton of control over your annual income. By being smart about how and when you pull money from your retirement accounts, you can directly influence your MAGI. And by influencing your MAGI, you control how much you pay for health insurance.

So, What Counts as MAGI? For most retirees, your MAGI is your Adjusted Gross Income (AGI) from your tax return, plus any tax-exempt interest and some non-taxable Social Security benefits. It includes income from pensions, traditional IRA or 401(k) withdrawals, capital gains, and any part-time work. Critically, qualified withdrawals from a Roth IRA do not count.

By keeping your MAGI within certain levels compared to the Federal Poverty Level (FPL), you can qualify for huge subsidies. For many, this is the difference between a premium over $1,000 a month and one that’s just a few hundred. It’s a game-changer.

Choosing Your Plan: Understanding the Metal Tiers

Once you're browsing the Marketplace, you’ll see plans broken down into "metal tiers": Bronze, Silver, Gold, and Platinum. These names have zero to do with the quality of doctors or hospitals. It's all about how you and the insurance plan split the costs.

- Bronze Plans: These have the lowest monthly premiums but the highest costs when you actually need care (like your deductible). They’re a fantastic fit for healthy retirees who just want a safety net for a major medical disaster and prefer low fixed costs. Many are also compatible with a Health Savings Account (HSA).

- Silver Plans: These are the middle-of-the-road option with moderate premiums and deductibles. But Silver plans have a superpower for people with lower MAGIs: Cost-Sharing Reductions (CSRs). If your income falls below 250% of the FPL, a Silver plan will also lower your deductible, copays, and out-of-pocket maximum, making it an incredibly valuable deal.

- Gold & Platinum Plans: These plans come with the highest monthly premiums but the lowest costs when you see a doctor or fill a prescription. They’re best for retirees who know they’ll be using medical services regularly and want predictable, low expenses for each visit.

Putting It All Together: A Tale of Two Retirees

Let's see how this plays out for two hypothetical 60-year-olds.

Retiree A: Healthy & Prefers Low Premiums

- Health: Great health, no ongoing conditions, rarely needs prescriptions.

- Financial Strategy: Manages retirement withdrawals to keep her MAGI around $40,000 (that's 276% of the FPL for one person). This gets her a nice premium tax credit, but she’s too high for the extra cost-sharing help.

- Plan Choice: She goes with a Bronze plan. Her subsidy makes the already low premium even more affordable. She then puts money into an HSA to cover her high deductible with tax-free dollars if she needs it. Her goal? Keep monthly costs rock-bottom and have catastrophic protection.

Retiree B: Manages Chronic Conditions

- Health: Deals with hypertension and arthritis, which means regular specialist visits and prescriptions.

- Financial Strategy: He intentionally keeps his MAGI lower, at $35,000 (about 241% of the FPL).

- Plan Choice: He smartly chooses a Silver plan. Because his income is under that 250% FPL line, he gets both the premium subsidy and those powerful cost-sharing reductions. His deductible plummets from thousands of dollars to just a few hundred, and his copays are much smaller. His goal? Predictable costs for the frequent care he knows he’ll need.

As you can see, the ACA Marketplace isn't a one-size-fits-all deal. It's a flexible system that rewards smart financial planning, making it one of the most essential early retiree health insurance options you can find.

When to Use COBRA as a Strategic Bridge

When you first leave your job, the thought of keeping your exact same health plan feels like a lifeline. That’s the simple promise of COBRA—it lets you continue your familiar employer-sponsored coverage for up to 18 months. But that continuity comes with a serious case of sticker shock.

Think of it this way: your old health plan was like a great apartment where your employer paid almost all the rent. With COBRA, you get to stay in that same apartment, but now you’re on the hook for 100% of the rent yourself, plus a 2% administrative fee just for the privilege. That sudden leap in cost can be jarring, often jumping to hundreds or even thousands of dollars every month.

Because of this, COBRA is rarely a smart long-term solution for early retirees. But that doesn’t mean it’s useless. Used as a short-term, strategic tool, it can be one of the most brilliant early retiree health insurance options in very specific situations. It's all about knowing exactly when to play that card.

The Perfect Scenario for the Deductible Reset

Let's paint a picture. Imagine you retire in October after a year of managing a major health issue. You’ve already paid your plan’s $5,000 annual deductible, and you might have even hit your out-of-pocket maximum. For the rest of the year, your medical costs are now either minimal or completely covered.

But if you switch to a brand-new ACA Marketplace plan on November 1st, the clock resets. Your deductible and out-of-pocket maximum drop back to zero. All of a sudden, you'd have to pay another $5,000 or more before that new plan really kicks in.

This is where COBRA becomes your secret weapon. By choosing COBRA, you keep your old plan, and your deductible stays met. You can finish out the year getting the care you need without facing huge new bills—other than that high monthly premium, of course. You're basically paying a premium to protect the financial progress you already made on your deductible.

Bridging a Short Coverage Gap

Here's another time when COBRA makes perfect sense: bridging a very short gap in coverage. Maybe you retired in November and have already found an excellent ACA plan that starts on January 1st. You just need to cover yourself for December.

While the COBRA premium will feel high for that one month, it’s often the simplest and cleanest solution. It saves you the headache of signing up for a short-term plan or scrambling for other coverage just to fill a 30-day window. You pay the premium, stay covered without a lapse, and then move smoothly to your new, more affordable plan in the new year. It’s a clean, efficient fix.

The 60-Day Election Window: A Strategic Advantage

One of COBRA’s most powerful features is that it’s retroactive. You have a full 60 days after your employer coverage ends to decide if you even want it. This gives you a "wait and see" period. If you stay healthy for 59 days with no medical bills, you can just let the window close and sign up for an ACA plan instead. But if you have a medical emergency on day 45, you can elect COBRA, pay the back-premiums, and get covered as if you never had a gap.

Timelines You Cannot Miss

This strategic flexibility is powerful, but it comes with deadlines that are set in stone. If you miss them, you lose your right to COBRA coverage for good.

- Election Deadline: You have 60 days to sign up, starting from the date you get your COBRA election notice or the date your coverage ends—whichever is later.

- Payment Deadline: Once you elect, you have 45 days to make that first premium payment. After that, payments are usually due monthly.

Understanding these timelines is the key to making a smart decision. While the high cost of COBRA can be scary, its power to provide seamless, short-term coverage makes it an incredibly valuable tool in the right circumstances. For those looking for other options, exploring a variety of COBRA insurance alternatives can help you find the most cost-effective path forward for your new life.

Diving Into Private and Short-Term Insurance Plans

Once you step outside the world of the ACA Marketplace and COBRA, you’ll find another set of early retiree health insurance options: private plans sold "off-exchange" and short-term insurance. They both promise flexibility, but it’s crucial to look closely. One might be a safe harbor, but the other could be a serious trap.

These two types of plans couldn't be more different. One provides solid, compliant coverage but without any financial assistance, while the other is a flimsy safety net that’s loaded with risk. Picking the wrong one can have major consequences for your health and your retirement savings.

Understanding Off-Exchange Private Plans

So, what exactly are "off-exchange" private plans? These are policies you buy directly from an insurance company or through a broker, completely separate from the government Marketplace. The good news is they are still required to be ACA-compliant. That means they have to cover essential health benefits and can't turn you away for pre-existing conditions.

Here’s the catch: because you're not buying them on the Marketplace, these plans are not eligible for premium tax credits or cost-sharing reductions. This is a massive distinction. You’re on the hook for the entire premium, which can be a hefty bill to pay each month.

So, who are these plans actually for? They typically appeal to a very specific type of person:

- High-Income Retirees: If your retirement income is too high to get ACA subsidies but you still want reliable, comprehensive coverage, this might be a fit.

- People Focused on a Specific Network: Sometimes, an off-exchange plan offers a wider network of doctors and hospitals than what's on the local Marketplace. If keeping your specific doctor is your number one priority, this could be an attractive route.

Ultimately, an off-exchange plan is a trade-off. You might get a better network, but you give up any shot at the financial help that makes ACA plans affordable for most early retirees.

A Cautious Look at Short-Term Insurance

Now let’s talk about short-term health insurance, an option that requires extreme caution. Think of these plans as temporary, bare-bones coverage designed only for a true catastrophe. They’re cheap for a reason—they aren't ACA-compliant and aren't considered real health insurance.

Key Takeaway: Short-term plans can legally deny you coverage for pre-existing conditions. They often use a tactic called post-claims underwriting, where they dig into your medical history after you file a claim and can refuse to pay if they find any link to a condition you had before you signed up.

This is the single biggest risk. You could pay premiums for months, thinking you're covered, only to find out your claim is denied right when you need the help most. These plans also routinely leave out coverage for essential benefits many of us depend on.

Common things they don't cover include:

- Prescription drugs

- Maternity care

- Mental health services

- Preventive care like your annual check-up

That low monthly premium looks tempting, but the potential for financial ruin is huge. For most people planning their retirement, the risks are simply not worth the savings. If you're curious about all the fine print, you can check out our guide on short-term health insurance.

The Financial Reality of the Insurance Market

Finding affordable coverage is already a challenge, and it's getting tougher. The entire U.S. health insurance industry is under a lot of pressure, with medical costs projected to climb by over 10% in many areas through 2025. This is driven by everything from general inflation to new, expensive medical treatments.

This environment makes it harder and harder for early retirees to bridge the gap with good, affordable coverage until they turn 65 and qualify for Medicare. You can discover more about these insurance market dynamics on S&P Global.

At the end of the day, while private and short-term plans are out there, they really only work for a small number of people. For the vast majority of early retirees, the financial safety net and comprehensive coverage you get from the ACA Marketplace is still the safest and most dependable choice.

How To Choose Your Best Health Insurance Plan

So, you've got a handle on the main health insurance options for early retirees, from the income-savvy ACA Marketplace to the stop-gap coverage of COBRA. Now comes the important part: moving from just knowing the map to actually charting your own course.

Here’s the thing: there's no single "best" plan for everyone. The right choice is deeply personal. It's the one that fits your life, your health, and your budget. This decision really boils down to three things: your health needs, your retirement finances, and how much risk you’re comfortable taking on. Get this right, and you can finally stop stressing about healthcare and start enjoying the freedom you’ve worked so hard for.

Start With a Personal Health Inventory

Before you even glance at a single insurance plan, you need to get crystal clear on what you actually need. Think of it like taking stock of your pantry before a big grocery run. If you don't have a list, you're just guessing.

Grab a notebook and jot down a few things for the upcoming year:

- List Your Prescriptions: Write down every single medication you and your spouse take, along with the dosage. Every plan has a different list of covered drugs (a formulary), and you need to be sure your must-haves are on it and affordable.

- Confirm Your Doctors: Who are your non-negotiable doctors, specialists, and hospitals? Make a list. As you compare plans, you’ll need to check if they are in-network to keep your costs from skyrocketing.

- Anticipate Your Medical Needs: Be honest with yourself. Are you managing a chronic condition that needs regular check-ins? Do you have a knee replacement or another big procedure on the horizon? A little foresight here is everything.

This simple inventory acts as your personal filter. It helps you instantly weed out plans that won't work, saving you a ton of time and future frustration.

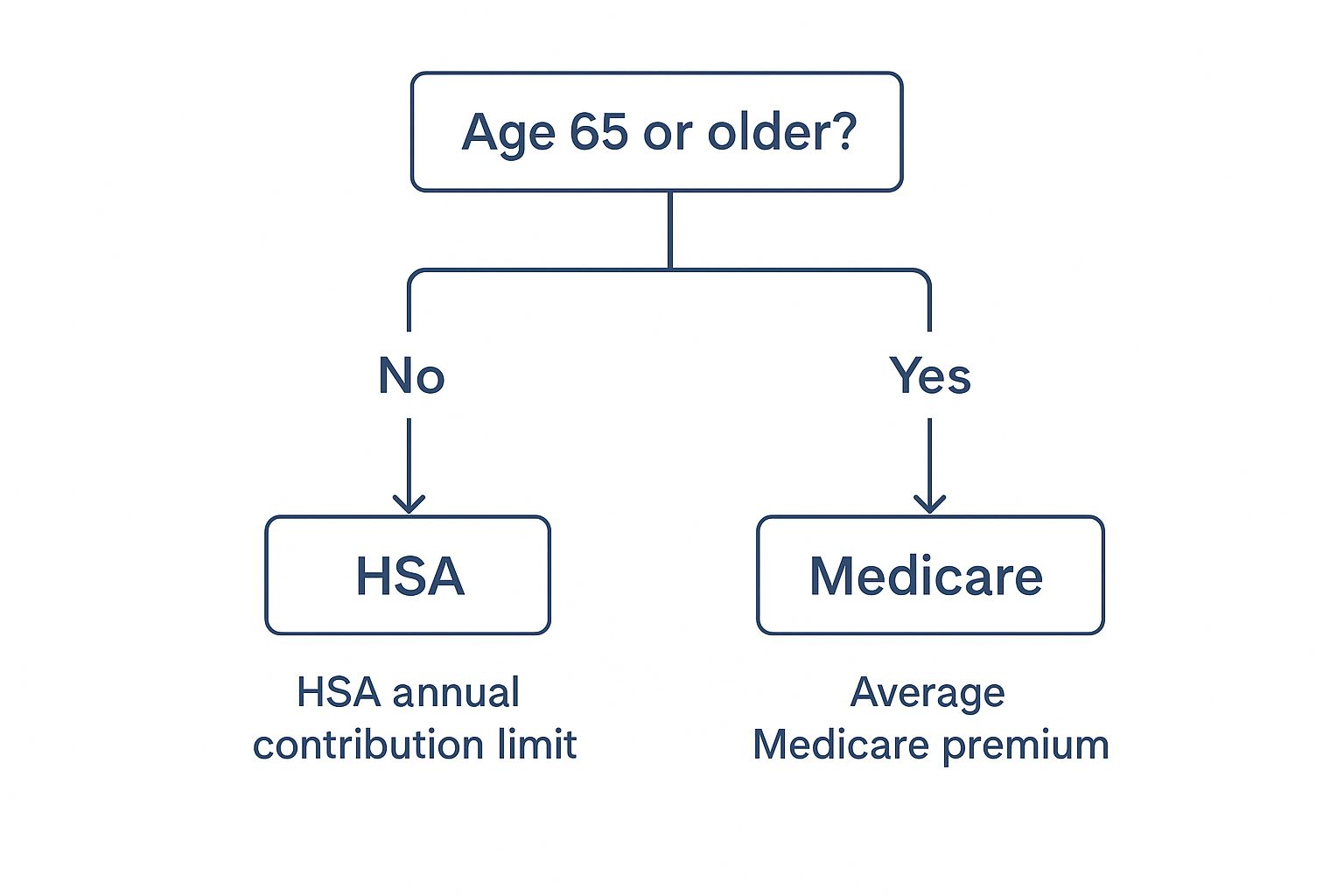

This decision tree offers a simple visual to find your starting point.

As you can see, your age is the first major fork in the road, pointing you toward entirely different insurance systems.

Weighing Costs Against Your Financial Risk

Next up, it’s time to crunch the numbers. And this is about way more than just the monthly premium. You have to look at the total potential cost—your deductible, your copays, and that all-important out-of-pocket maximum. Your comfort level with financial risk plays a huge role here.

Are you the kind of person who would rather pay a higher, fixed premium each month for the peace of mind of knowing your costs will be low when you need care? Or do you prefer a low monthly bill, accepting the risk that you might face a high deductible if a medical emergency pops up?

The Big Picture: Choosing a plan is a balancing act between fixed costs (premiums) and variable costs (deductibles, copays). A low-premium Bronze plan might save you money every month, but a single hospital stay could mean paying thousands out-of-pocket before your insurance fully kicks in.

Feature Comparison Across Retiree Health Insurance Types

With your health inventory and budget in hand, it's time for a direct comparison. This table breaks down the key features of your main early retiree health insurance options to help clarify the trade-offs.

| Feature | ACA Marketplace Plan | COBRA | Short-Term Plan |

|---|---|---|---|

| Best For | Long-term, affordable coverage, especially with managed income. | Short-term continuity; keeping your exact doctors/plan. | Healthy individuals needing a temporary catastrophic bridge. |

| Subsidies | Yes, premium tax credits and cost-sharing reductions available. | No, you pay 100% of the premium plus a 2% fee. | No, these plans are not eligible for any financial assistance. |

| Pre-Existing | Covered, cannot be denied or charged more. | Covered, as it's a continuation of your old plan. | Not covered, can lead to claim denials or cancellation. |

| Risk Level | Low. Comprehensive coverage with consumer protections. | Moderate. High cost is the main risk; coverage is solid. | High. Major risk of uncovered claims and coverage gaps. |

Seeing the options laid out like this makes the trade-offs clear. If affordability and solid protection are your top priorities, the ACA Marketplace is almost always your strongest bet. But if you just need to cover a two-month gap and have a major surgery scheduled with your current doctor, COBRA’s high price tag might be worth it.

Making this choice can feel overwhelming, but it becomes much simpler when you break it down into these manageable steps. For more guidance, you might find our article on how to choose health insurance for smart coverage helpful. By carefully thinking through your needs and comparing your options, you can make a confident decision that protects both your health and your retirement savings.

Frequently Asked Questions

Once you’ve gone through the main health insurance options for early retirement, a bunch of “what if” questions usually pop up. It’s totally normal. After all, everyone’s situation is a little different.

Think of this section as the final check-in. We're here to tackle those lingering questions so you can step into this new chapter of your life feeling confident and prepared.

Can I Use My HSA to Pay for Health Insurance Premiums?

Yes, but it's a bit tricky. The rules are very specific.

You can absolutely use your Health Savings Account (HSA) funds, completely tax-free, to pay for COBRA premiums. This is a huge win and can make the high cost of COBRA much more manageable.

But for ACA Marketplace plans or other private insurance, it's a different story. You generally cannot use HSA funds for those premiums. Don't let that discourage you, though. Your HSA is still a powerhouse tool for covering all your other medical expenses—like deductibles, copays, and prescriptions—under any plan you choose.

What Should I Do If My Income Changes Mid-Year on an ACA Plan?

This one is critical: report any significant income changes to the ACA Marketplace as soon as they happen. Don't put it off until tax season. Your subsidy eligibility is tied directly to your income, and keeping it current is the best way to protect yourself from financial surprises.

If your income goes up, your premium tax credit might shrink. Reporting it right away adjusts your monthly bill, so you won’t get hit with a nasty bill from the IRS when you file your taxes.

On the flip side, if your income drops, you might qualify for an even bigger subsidy or powerful cost-sharing reductions. Reporting that change means you start saving money immediately.

Think of it this way: The Marketplace is designed to be flexible, but it can’t help you if it doesn’t have the right information. Proactive reporting is your best friend here.

Is It Better to Join My Working Spouse's Health Plan?

For a lot of early retirees, this is the simplest and most affordable path. When you leave your job, you trigger a Qualifying Life Event. This opens up a Special Enrollment Period for your spouse—usually 30 to 60 days—to add you to their company’s plan.

This route often gets you excellent coverage at a reasonable group rate. But always run the numbers first.

Calculate the exact cost to add you to your spouse's plan. Then, compare that against what you’d pay for an ACA Marketplace plan after subsidies. Sometimes, if your household income qualifies for major financial help, the Marketplace can still come out cheaper. A little homework here can save you a lot.

We know these decisions can feel heavy, but you don't have to figure it all out on your own. The experts at My Policy Quote are here to help you compare plans and find the perfect fit for your new life. Get your personalized quote today!