Choosing between a PPO and an HMO really comes down to one big question: What do you value more, flexibility or cost?

A PPO gives you more freedom to choose your doctors and see specialists whenever you want, no referral needed. But that freedom usually comes with a higher monthly price tag. On the other hand, an HMO is more structured. It keeps your premiums lower but requires you to stick to its network of doctors and get a referral before seeing a specialist.

Comparing PPO vs HMO Plan Structures

Picking a health insurance plan can feel like you're trying to crack a code. All those acronyms and rules—it’s a lot. But understanding the basic difference between a PPO (Preferred Provider Organization) and an HMO (Health Maintenance Organization) is the first real step to finding clarity. Each one is built around a totally different idea of how you should get—and pay for—your healthcare.

Honestly, the "right" choice is all about you. Do you want a huge list of doctors to choose from and the power to book a specialist appointment on your own? Or is your main goal to keep your monthly budget predictable and low? Neither plan is better than the other, but one will definitely fit your health needs, finances, and lifestyle better.

Let's break down the key differences side-by-side so you can see exactly what you're getting with each.

PPO vs HMO at a Glance

This table gives you a quick, straightforward look at how PPO and HMO plans stack up against each other.

| Feature | PPO (Preferred Provider Organization) | HMO (Health Maintenance Organization) |

|---|---|---|

| Provider Choice | Large, flexible network of doctors and hospitals. You have more options. | You must use doctors and hospitals within a specific, smaller network. |

| Specialist Referrals | No referral needed. You can see any specialist directly. | Referral required. Your Primary Care Physician (PCP) must refer you first. |

| Out-of-Network Care | Covered, but you'll pay more for it. Expect a separate, higher deductible. | Not covered, except for true, life-threatening emergencies. |

| Primary Care Physician (PCP) | Optional. You don’t need to choose one to manage your care. | Mandatory. You must select a PCP to be your main point of contact. |

| Typical Monthly Premiums | Generally higher because of the extra flexibility. | Generally lower, making them a more budget-friendly choice. |

| Claims Process | You might have to file your own claims, especially for out-of-network care. | Simpler process. The plan and your in-network doctor handle the paperwork. |

This comparison really highlights the central trade-off. With a PPO, you get a ton of freedom to manage your own healthcare journey. You can see specialists or go to out-of-network hospitals if you feel you need to. That freedom, however, comes at a price—both in your monthly premiums and potential out-of-pocket costs.

The core decision is a balance between freedom and finances. A PPO is like an à la carte menu where you pay more for choice, while an HMO is like a set menu that offers great value but with fewer options.

In contrast, HMOs are all about efficiency and coordinated care. By having you work through a primary doctor and stay within their network, they control costs much more effectively. Those savings are then passed on to you as lower premiums. This model is perfect for people who like having a trusted doctor guide their care and want to keep their monthly expenses as low as possible. As we dig deeper, you’ll see how these differences affect everything from your yearly budget to how you schedule a simple check-up.

The Big Picture: PPO vs. HMO Fundamentals

Before we get into the nitty-gritty, it's crucial to understand the core philosophy behind PPO and HMO plans. Think of them as two completely different approaches to managing your health. One is built on coordinated structure, and the other is all about flexible access.

Neither is automatically "better." But one will almost certainly fit your life, your budget, and your health needs better than the other.

An HMO is designed around one central idea: coordinated care. This model tries to manage your health and your costs by creating a streamlined, predictable system.

On the other hand, a PPO is built on flexibility and choice. It puts you in the driver's seat, letting you see the doctors and specialists you want without asking for permission first. That freedom, however, comes with a different price tag.

The HMO Model: Coordinated and Structured

The heart of any Health Maintenance Organization (HMO) is your Primary Care Physician (PCP). This is your go-to doctor, the central hub for everything related to your health, from an annual check-up to a sudden illness.

Think of your PCP as your trusted guide or even a "gatekeeper." If you need to see a specialist—like a cardiologist or a dermatologist—you start with your PCP. They’ll give you a referral, which is their professional authorization for you to see that specialist.

This system ensures your care is managed and you’re seeing the right person for your condition, which helps keep costs down. The trade-off? You have to stay within the HMO's network of doctors and hospitals for your care to be covered (except in a true emergency).

The PPO Model: Flexible and Independent

A Preferred Provider Organization (PPO) offers a totally different experience. Its main draw is the freedom to direct your own healthcare journey. You don’t have to pick a PCP, and you never need a referral to see a specialist.

Woke up with a weird rash and want to see a dermatologist? Just find one in the PPO’s network and book it. This direct access is a huge plus for people who value convenience and autonomy.

PPOs also offer a major benefit that HMOs don’t: out-of-network coverage. While you'll always pay less by staying with the plan's "preferred" providers, you have the option to see a doctor or use a hospital outside that network.

With a PPO, you are paying a premium for control. You decide which doctors to see and when, but this independence often means higher monthly premiums and potentially more complex billing if you venture out-of-network.

This flexibility is perfect if you want to keep a doctor who isn't in a specific network, or if you travel a lot and might need care in different parts of the country. Just know you'll likely face higher copays, a separate (and usually much larger) out-of-network deductible, and you might even have to file your own insurance claims.

Where the Market Stands

These structural differences have a huge impact on which plans are most common. In the 2025 health insurance landscape, HMOs are the dominant force, making up 61.9% of the market with 3,518 available plans. PPOs are next, accounting for 35.4% with 2,010 plans.

This trend shows that the HMO focus on cost control is a major draw, especially for budget-conscious self-employed professionals and 1099 contractors who prefer predictable costs over maximum flexibility. You can see more details on these 2025 health plan trends at healthworksai.com.

Getting these basics down is the first step. To go a bit deeper, check out our guide on what health insurance is and how it works. It’ll give you the foundation you need to really compare the specific features we're about to dive into.

A Detailed Comparison of Core Plan Features

To really get what separates PPO and HMO plans, you have to look past the basics. We need to dissect the features that actually hit your daily life and your wallet. The choice between them comes down to the little details—how you get care, whether you need referrals, and what your healthcare journey will truly cost.

Think of it this way: every feature is a trade-off between freedom and financial predictability. Let's put these core components side-by-side to see which one feels right for you.

Provider Networks and Your Freedom of Choice

This is the big one. It's where the two plans diverge the most. A PPO plan usually comes with a much larger network of doctors and hospitals, giving you a wider menu of choices for your care. If you live in a big city or want the ability to see top-rated specialists across different health systems, this is a huge plus.

An HMO, on the other hand, works with a more contained, local network. This smaller group of providers agrees to set fees with the insurer, which is how they keep costs down. If you're leaning toward an HMO, it is absolutely critical to check that your current doctors, go-to hospitals, and any specialists you see are in their network.

You can see this difference play out in real-world enrollment numbers. A 2025 survey showed that 46% of covered workers are in PPOs, while only 12% are in HMOs. People just tend to gravitate toward the PPO’s flexibility. It's a better fit for folks who travel or want to see a variety of providers without being locked into one system.

The Referral Process: A Gatekeeper vs. Direct Access

How you get to a specialist is another major fork in the road. HMO plans are built around a "gatekeeper" model. Your Primary Care Physician (PCP) is your quarterback, coordinating all your care. Need to see a heart doctor? You have to visit your PCP first to get a referral.

This process is designed to make sure your care is necessary and that you're seeing the right kind of specialist, which helps control costs. But it also adds an extra step—and sometimes an extra copay—before you can get specialized treatment.

PPOs offer a straight shot. If you feel you need a specialist, you just find one in your network and book an appointment. This direct access is a massive advantage for people who want more control or who see specialists often and don't want the hassle of getting a referral for every single visit.

A PPO makes you the manager of your own healthcare team—you schedule with specialists as you see fit. An HMO makes your PCP the team captain, directing the flow of your care to keep things efficient and coordinated.

Out-of-Network Coverage: The Ultimate Safety Net

Here’s one of the most important distinctions between PPO and HMO plans. PPOs give you the freedom to get care outside their network, but it’ll cost you more. You'll face a separate, much higher out-of-network deductible and coinsurance. Plus, you might have to file the claim paperwork yourself.

But this flexibility is a crucial safety net for a few reasons:

- Continuity of Care: It lets you keep seeing a doctor you trust, even if they aren't in the PPO network.

- Access to Top Specialists: If the best expert for a specific condition is out-of-network, a PPO lets you see them.

- Travel and Emergencies: It gives you coverage when you’re traveling and need non-emergency care where your network is thin.

HMOs, in contrast, offer no coverage for out-of-network care unless it's a true, life-threatening emergency. If you decide to see an out-of-network doctor for a routine visit, you will pay 100% of the bill. It's a rigid rule, but it's fundamental to how HMOs keep costs low.

For anyone looking for a middle ground, it might be worth exploring how POS plans work. They often blend features from both HMOs and PPOs. You can learn more by exploring how POS plans work in our guide.

Comparing the Full Cost Structure

HMOs might have lower monthly premiums, but that's not the whole story. To get the real financial picture, you have to look at everything together: premiums, deductibles, copayments, and coinsurance.

HMO Cost Profile:

- Lower Premiums: Your monthly payment is usually easier on the budget.

- Lower Deductibles: You often have a very low or even a $0 deductible for in-network care.

- Predictable Copayments: You can expect fixed, predictable copays for doctor visits and prescriptions.

PPO Cost Profile:

- Higher Premiums: You pay more each month for that extra freedom.

- Higher Deductibles: In-network deductibles are typically higher than HMOs, and out-of-network deductibles are way higher.

- Coinsurance: Once you hit your deductible, you’ll usually pay a percentage of the cost (coinsurance) instead of a flat copay.

When you're doing a detailed comparison of core plan features, you also need to check what services are included. For instance, is preventive dental covered by insurance? Little details like that can make a big difference for your long-term health and finances. It’s always worth digging into the fine print of any plan you consider.

Real-World Scenarios: Choosing the Right Plan for Your Life

Reading about features and benefits is one thing, but how do these plans actually perform in the real world? The true difference between a PPO and an HMO shines through when you see them in action. Let's explore a few relatable situations to help you see which plan fits your life, your budget, and what you value most in healthcare.

We'll walk through the decision process for three different people, each with their own unique needs and priorities.

The Self-Employed Professional: Balancing Costs and Access

Meet Alex, a freelance graphic designer. Alex’s income can fluctuate, so keeping monthly costs predictable is a must. At the same time, Alex has a trusted therapist who isn't in every network, creating a classic PPO vs. HMO dilemma.

The HMO Option: Alex could grab an HMO for a lower, more stable monthly premium. This would be great for budgeting. The problem? That go-to therapist is out-of-network, meaning those visits wouldn't be covered. Alex would have to pay 100% out of pocket or start over with someone new.

The PPO Option: A PPO comes with a higher monthly premium, which adds to the budget. But it offers out-of-network coverage for the therapist. While reimbursement is lower and there's a separate deductible to meet, it provides the freedom to stick with a provider who is crucial for mental well-being.

The Decision: Alex chooses the PPO. The higher premium is a calculated trade-off. For Alex, the peace of mind and continuity of care with a trusted specialist is worth the extra cost.

The Early Retiree: Managing Chronic Conditions

Now let's look at Brenda, a 62-year-old who just retired. She manages arthritis and high blood pressure, seeing a rheumatologist and a cardiologist regularly. Her top priority is coordinated, high-quality care without any surprise bills.

For anyone managing long-term health issues, care coordination is just as vital as cost. A scattered approach can lead to conflicting advice and higher expenses, making the all-in-one structure of an HMO a huge plus.

Brenda's situation is a perfect example of where a centralized model shines.

The HMO Advantage: An HMO assigns Brenda a Primary Care Physician (PCP) to act as her healthcare quarterback. This doctor coordinates everything, ensuring her specialists are on the same page and her medications are managed safely. Since everyone is in the same network, communication flows easily, and her costs are predictable and low.

The PPO Challenge: With a PPO, Brenda would have to manage all the communication between her specialists herself. While she wouldn't need referrals, she'd be responsible for making sure every doctor had her complete, up-to-date medical history. This could easily lead to communication gaps or unexpected bills from an out-of-network lab.

The Decision: Brenda goes with the HMO. The coordinated care managed by her PCP gives her confidence that her chronic conditions are being handled properly. On a fixed retirement income, the lower, predictable costs are a massive relief.

The Young Family: Focused on Routine Care

Finally, let's meet the Miller family. With two young children, their healthcare needs are mostly predictable: annual check-ups, the occasional ear infection, and maybe an unplanned trip to urgent care. Their main goal is keeping monthly premiums down while having easy access to a great pediatrician.

The Millers just need a plan that’s affordable and simple for life’s everyday bumps and sniffles.

HMO for Predictability: An HMO gives them a low premium and simple, fixed copays for pediatrician visits. They can pick a PCP for each family member, and that doctor is their first call for everything. It’s a straightforward system that works perfectly for keeping their budget in check.

PPO for Flexibility: A PPO would offer more choices for pediatricians, including some at a top children's hospital that is out-of-network for most HMOs. However, the much higher premium and deductible probably aren't worth it for their current, relatively simple healthcare needs.

The Decision: The Millers choose the HMO. It provides excellent, affordable coverage for their family's routine care. They agree that if a more specialized health issue comes up down the road, they can always re-evaluate their options during the next open enrollment period.

The True Cost of Your Health Plan: A Financial Deep Dive

When you're choosing between a PPO and an HMO, the monthly premium is just the tip of the iceberg. The real financial story unfolds when you start using your insurance—for prescriptions, specialist visits, and unexpected care. Understanding these moving parts is the only way to avoid sticker shock and truly budget for your health.

The financial DNA of PPO and HMO plans is fundamentally different, and that difference directly shapes your out-of-pocket costs and how predictable your healthcare spending will be all year long.

Looking Beyond the Premium

To get the full financial picture, you have to look at four key pieces together: the premium, the deductible, your copayments or coinsurance, and the out-of-pocket maximum. HMOs often look attractive upfront with their low premiums and simple, fixed copayments for routine visits. It feels predictable.

A PPO, on the other hand, usually comes with a higher monthly premium. After you meet your deductible, it often uses coinsurance, meaning you pay a percentage of the bill. This can feel a lot less predictable, especially if you end up needing complex or frequent medical attention.

The sticker price of a plan—its premium—is just the starting point. The true cost is revealed when you factor in how much you'll pay when you actually use your insurance.

Hidden Costs and Financial Traps

Each plan has its own unique financial risks hiding just beneath the surface. With an HMO, a delay in getting a referral to a specialist isn't just an inconvenience; it can become a real financial problem. If a condition worsens while you wait, the treatment you eventually need could be far more expensive.

For PPO members, the biggest risk is the out-of-network trap. That freedom to see any doctor sounds great, but the costs can be astronomical. Going out-of-network almost always means a separate, much higher deductible and less coverage. Even worse, there's often no cap on what you might have to pay, leaving you exposed to massive bills. To get a better handle on this, check out our guide on how deductibles in health insurance work.

How Market Trends Shape Your Price Tag

The plans available in your area—and what they cost—are also driven by huge market forces. The HMO industry is on track to hit $359.2 billion by 2026, with giants like UnitedHealth and Anthem using their market power to negotiate lower rates with in-network providers. This is how they keep costs down.

Meanwhile, PPOs still dominate the group revenue share at 49.46% in a market expected to reach $1.61 trillion by 2030. Their popularity in employer-sponsored plans shows just how much people value flexibility. You can discover more insights about these market trends on ibisworld.com.

Don't Forget About Prescription Drugs

Prescription drug coverage is a massive, and often underestimated, piece of the financial puzzle. Both PPOs and HMOs use a formulary—a list of approved drugs—but how they structure it and what you pay can be wildly different.

Key Differences in Prescription Coverage:

- Tiered Formularies: Nearly all plans group drugs into tiers. Tier 1 is for generics with the lowest copay. Higher tiers for brand-name or specialty drugs will cost you a lot more.

- Prior Authorization: Both plan types can require your doctor to get approval for expensive medications, but HMOs tend to use this tool more aggressively to manage costs.

- Step Therapy: An HMO might require you to try a cheaper, but still effective, alternative medication first before they'll cover a more expensive one. This is called step therapy.

When comparing plans, don't just see if your medication is on the list—find out which tier it's on. A plan with a low premium can quickly become a financial nightmare if your daily medication is stuck on a high-cost tier. This is one of the most important checks you can do to find a plan that actually works for your budget.

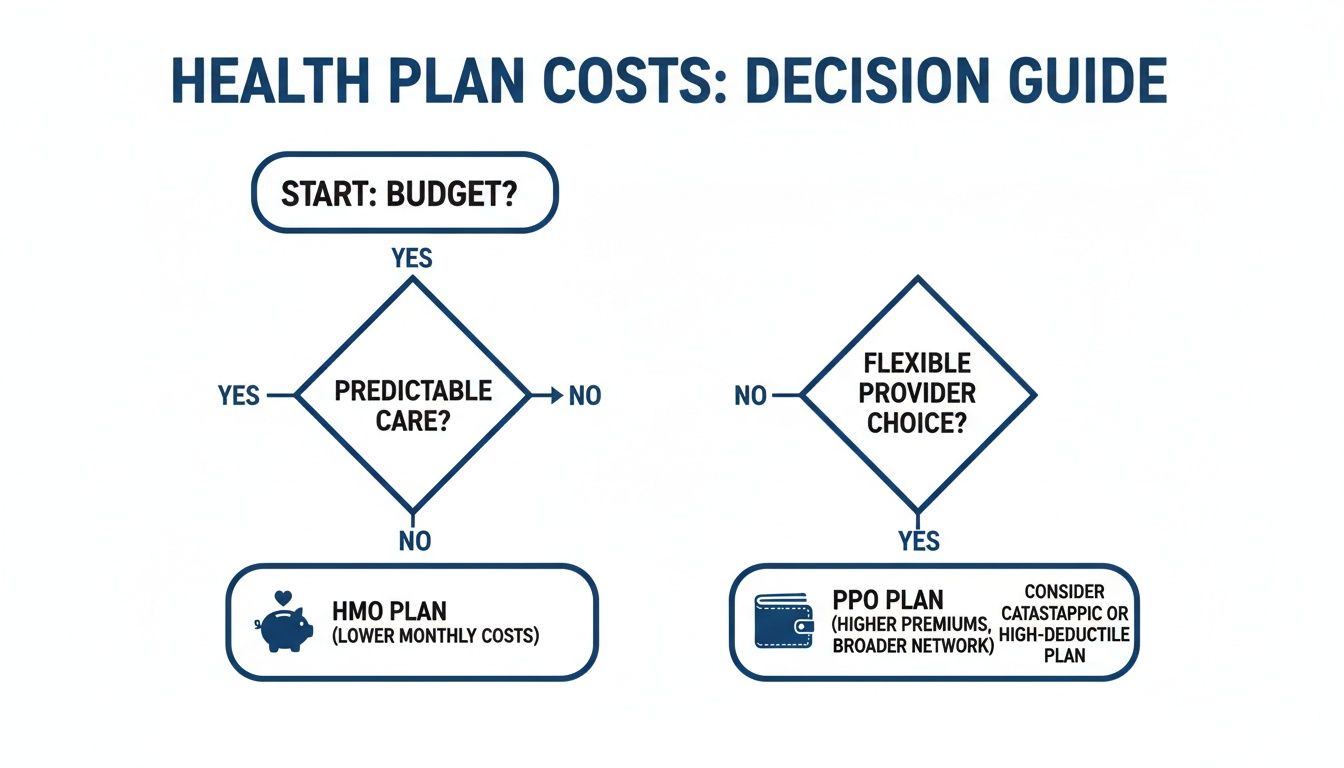

A Simple Checklist for Making Your Decision

Okay, let's cut through the noise. Making the final call between a PPO and an HMO really just comes down to what you value most. This isn't about finding the "best" plan, but the right plan for you.

Answering these questions honestly will pretty much make the decision for you.

Doctor Loyalty: Is sticking with your current doctor a dealbreaker? If you have a doctor or hospital you love and trust, you'll want to check if they're in-network. A PPO gives you a better shot, but you still have to verify.

Specialist Access: How do you feel about needing a referral to see a specialist? If you want to book an appointment directly without asking your primary doctor for permission first, a PPO is your friend.

Budgeting Style: Are you someone who needs predictable, fixed costs? Or are you okay paying a bit more each month for the freedom to choose your own providers? An HMO usually means lower, steadier premiums, while a PPO trades higher monthly payments for more flexibility.

This decision tree gives you a great visual for how to think about it.

As you can see, if you prioritize predictable spending, the path often leads to an HMO. If you need more wiggle room, a PPO is likely the better fit.

Your Next Steps

Once you have a gut feeling about which plan type fits your life, it's time to look at real numbers. Getting personalized quotes is the only way to turn this from a hypothetical choice into a real one. It’s where you see the actual premiums and what you get for your money.

Your answers here aren't just for a checklist; they're the foundation of your healthcare strategy. The best plan is the one that gives you peace of mind, fits your budget, and supports your health on your terms.

Now that you've got a clearer picture, you're ready to dig deeper. To get a better handle on how to weigh your options, you can learn more about how to compare health insurance plans in our detailed guide.

Still Have Questions About PPO vs. HMO?

It’s completely normal to have a few questions lingering even after you’ve compared the big picture. Let’s clear up some of the most common sticking points so you can feel confident in your choice.

What Happens in an Emergency with an HMO?

This is one of the biggest myths out there. Both HMO and PPO plans are legally required to cover true, life-threatening emergencies at any hospital, regardless of whether it's in-network. So if you’re having a heart attack, get to the nearest ER. Your HMO has you covered as if you were in-network.

The real difference comes after you’re stabilized. Once it's safe for you to be moved, your HMO will almost certainly require you to transfer to an in-network hospital for the rest of your care.

Can I Just Switch Between a PPO and an HMO Anytime?

Usually, no. Health insurance isn't something you can change on a whim. You typically have one shot a year during the annual Open Enrollment Period to switch from an HMO to a PPO or the other way around.

The only exception is if you have a Qualifying Life Event (QLE). These are major life changes that open up a Special Enrollment Period for you.

- Getting married or divorced

- Having a baby or adopting

- Moving to a new zip code

- Losing your previous health coverage

Do My Prescriptions Really Change That Much Between Plans?

Yes, this can be a huge deal. The differences between PPO and HMO plans go right down to their formularies—the official list of drugs they cover. It's a classic "devil is in the details" situation.

One plan might cover that brand-name medication you rely on for a small copay. Another might not cover it at all, or it could be on a super expensive tier. Before you commit to any plan, you absolutely have to check its formulary. Make sure your essential medications are covered affordably, because this can make or break your healthcare budget for the year.

Feeling ready to see what your options look like? The expert team at My Policy Quote can help you compare plans side-by-side and find the perfect fit for your life and budget. Get your personalized quote today!