If you've recently lost your job, the first question on your mind is often about health insurance. The simple, hard truth about COBRA is this: you’ll be paying 102% of the full premium. That includes the portion you paid as an employee and the much larger share your employer was covering.

It’s no surprise that the monthly cost can feel like a punch to the gut.

The True Cost of COBRA Insurance: A Straightforward Answer

The sticker shock is real. When you were employed, your company likely paid a huge chunk of your health insurance costs behind the scenes. Now, that safety net is gone, and you’re shouldering the entire burden yourself.

Think of it like this: your employer was paying most of the rent on your apartment. Now, they've moved out, and you're responsible for the full lease, plus a 2% admin fee for the landlord. It’s the same apartment, but the cost feels completely different.

This sudden shift is why a premium that seemed manageable before can suddenly jump to a figure that feels impossible. Understanding this from the start is key to making a clear-headed decision.

Understanding the Typical Price Range

So, what kind of numbers are we talking about? While every plan is different, we can look at some general estimates to get a sense of what to expect. The final price tag depends on how robust your plan is (think a PPO vs. an HMO), where you live, and whether you’re covering just yourself or a whole family.

A low-deductible plan with a massive network of doctors will always cost more than a high-deductible plan with fewer options. The numbers can be startling, with family plans often running into the thousands each month.

To give you a more concrete idea, let's look at some projected figures. For some 2026 plans, individual monthly premiums are estimated to fall between $640 and $930. Family coverage? That can soar to anywhere from $2,113 to $3,068 per month. You can find more details about these 2026 COBRA health rates to see how costs can vary.

A Quick Look at Estimated Costs

To really visualize the potential financial hit, it helps to see the numbers laid out. This table gives a snapshot of what you might encounter.

Estimated Monthly COBRA Premium Ranges

The following table summarizes the typical monthly costs for COBRA, highlighting the significant jump between individual and family plans.

| Coverage Type | Typical Low-End Monthly Cost | Typical High-End Monthly Cost |

|---|---|---|

| Individual Coverage | $600 | $950 |

| Family Coverage | $1,500 | $2,500+ |

These figures aren't meant to scare you, but to prepare you. Now that you have a grasp of the potential cost, we can dive into why it's so expensive and—more importantly—what other, more affordable options might be available.

Why You Suddenly Pay the Full Price for COBRA

If you just got your first COBRA bill, the number at the bottom probably feels like a punch to the gut. How can the same health plan you had last month suddenly cost three, four, or even five times more?

The answer is simple, but it changes everything: your employer’s contribution is gone.

When you were employed, you and your company were partners in paying for your health coverage. A slice came out of your paycheck, but your employer paid the rest—and their part was almost always the biggest piece of the pie. Now, that safety net has vanished.

Think of it like this: your job gave you a company car and covered most of the gas. You just had to chip in a little bit each month. With COBRA, you get to keep the car, but now you’re responsible for the entire gas bill, plus a small fee to keep it registered in your name. Same car, totally different cost.

Unpacking the 102 Percent Formula

That shocking price jump isn’t random; it’s baked into the federal law that created COBRA. The law allows the plan administrator to charge you the full cost of your health plan—that’s your old contribution plus what your employer was paying—and then tack on a 2% administrative fee.

The takeaway: That "102% of the premium" figure isn't a penalty. It’s simply the total price your employer was covering for your health plan, with a tiny fee added for the paperwork involved in keeping you on it.

This is why your monthly payment can leap from $250 to well over $1,000. You were only ever seeing the tip of the iceberg. The rest was a powerful, but invisible, part of your compensation.

How the Quality of Your Plan Affects the Price

Not all health plans are built the same, and the better your old plan was, the more you can expect to pay for COBRA. The "richness" of your plan is determined by a few key things.

- Plan Type: A flexible PPO plan with a huge network of doctors is almost always more expensive than a more restrictive HMO plan.

- Deductibles and Out-of-Pocket Costs: If your plan had a super low deductible and great coverage that kicked in right away, it cost more per month. The insurance company was taking on more of the risk.

- Coverage Scope: Plans that generously cover prescriptions, specialist visits, mental health, and other therapies have a higher price tag.

If you had a top-of-the-line "platinum" or "gold" plan at your job, your employer was footing a very large bill each month. Now, that entire bill is yours.

The Geographic Cost Factor

Where you live also plays a huge role in how much COBRA insurance is. Healthcare isn't priced the same everywhere. A plan in a big city like New York or San Francisco will have a much higher base cost than the exact same plan in a small rural town.

This comes down to a few local factors:

- Provider Rates: Hospitals and doctor groups in different regions negotiate very different rates with insurance companies.

- Local Competition: The number of insurers and hospital systems in your area can drive costs up or down.

- State Rules: State-specific insurance laws can also add to the overall cost of health plans sold there.

Ultimately, the sticker shock from COBRA is really just a moment of sudden transparency. For the very first time, you’re seeing the true, unsubsidized market price of your health insurance. And that number is almost always bigger than anyone expects.

How to Calculate Your Personal COBRA Cost

General estimates are helpful, but let's be real—what you need is your number. It's time to move from theory to practice and figure out exactly what COBRA will cost you each month. The good news? This isn't complex algebra. It's just about finding two key pieces of information you already have access to.

Think of it like being a financial detective. Your mission is to uncover the full, unsubsidized price of your health plan—the one that was mostly hidden from view while you were employed. Once you find it, calculating your personal COBRA cost is surprisingly simple.

Step 1: Locate Your Total Health Premium

The single most important number you need is the total monthly premium for your health plan. This is the combined amount that both you and your employer were paying together.

Your official COBRA notice should spell this out clearly. But if you don't have it yet, you can hunt down the clues on your final pay stub or in your old benefits paperwork. Your pay stub shows your contribution (the amount deducted for "health insurance"), but that’s only half the story. The bigger piece is what your employer paid on your behalf, which you can usually find in a benefits summary or by asking your former HR department.

Step 2: Do the Simple Math

Once you have both numbers, the rest is easy. Just add them together to get the total monthly premium.

- Your Monthly Contribution + Your Employer's Monthly Contribution = Total Monthly Premium

This total is the true, undiscounted price tag of your health insurance. It’s the full amount the insurance company was getting paid every month for your coverage. If you need a refresher on the basics, our guide explains what an insurance premium is and how it all works.

Now for the final step. To get your actual COBRA cost, you’ll multiply that total premium by 102% (or 1.02). That extra 2% is a small administrative fee the plan is allowed to charge for managing your account.

The Formula: Your COBRA Cost = (Your Contribution + Employer's Contribution) x 1.02

That’s it. This simple formula cuts through the confusion and gives you a concrete number you can use for budgeting and making smart decisions.

Real-World Calculation Examples

Let's walk through a few scenarios to see how this math plays out in the real world. As you'll see, the numbers can change dramatically depending on whether you're covering just yourself or a whole family.

To make this crystal clear, here are a few examples showing how the sticker shock happens.

Sample COBRA Cost Calculation Scenarios

| Scenario | Employee Monthly Share | Employer Monthly Share | Total Monthly Premium | Estimated Monthly COBRA Cost (102%) |

|---|---|---|---|---|

| The Single Professional | $150 | $600 | $750 | $765 |

| The Couple | $300 | $900 | $1,200 | $1,224 |

| The Family of Four | $450 | $1,300 | $1,750 | $1,785 |

These examples show why knowing the employer's contribution is the key. It’s almost always the largest part of the total premium.

Once you have your number, you’re no longer in the dark. You can move beyond the initial shock and start planning your next steps with real, actionable information. Now you can accurately budget for COBRA or compare it fairly against other health coverage alternatives.

Exploring Smarter Alternatives to COBRA

While COBRA lets you keep the health plan you know, that comfort comes at a steep price. In fact, it's almost never the most affordable path forward.

Sticking with COBRA without looking at other options is a bit like re-signing your apartment lease without checking if there are better, less expensive places on the market. This is one of those moments where a little bit of shopping around can literally save you thousands of dollars.

Instead of just accepting that high COBRA premium, it's time to take control. There are several powerful alternatives out there, many of which offer huge savings. Let’s walk through your best options, one by one.

The ACA Marketplace: Your Strongest Ally

For most people, the best place to start is the Health Insurance Marketplace (you might know it as Healthcare.gov or your state’s own version). It was built specifically to help individuals and families find affordable coverage when they don't have it through a job.

Losing your employer-sponsored health insurance is what’s known as a Qualifying Life Event (QLE). This is your golden ticket. It opens up a Special Enrollment Period, which lets you sign up for a new plan on the Marketplace right away, without having to wait for the annual open enrollment window.

You typically have 60 days from the day your old coverage ends to pick a new Marketplace plan. Don't let that deadline slip by.

Key Insight: A Qualifying Life Event is what ensures you're not left without options after a job loss. It gives you immediate access to the ACA Marketplace.

But the biggest win here? Financial help. Based on what you expect your income to be for the rest of the year, you could qualify for subsidies that slash your monthly premium. These subsidies, called Premium Tax Credits, can make a top-notch plan far more affordable than COBRA.

Think about it: a family looking at a $1,800 monthly COBRA bill might find a great Marketplace plan for just $400 a month after subsidies. That’s a savings of $1,400 every single month.

Joining a Spouse's or Partner's Plan

Another fantastic, straightforward option is getting added to your spouse's or domestic partner's health plan. Just like with the Marketplace, losing your job is a QLE that allows your spouse to add you to their insurance.

This is often one of the most stable and budget-friendly moves you can make. Yes, the premium taken from your spouse's paycheck will go up, but it's almost guaranteed to be cheaper than paying 102% of your old plan's full cost through COBRA.

Your spouse just needs to let their HR department know about the change. They'll have to fill out some paperwork, usually within 30 days of you losing your coverage. It's a simple way to get great benefits without a massive financial hit.

Other Practical Coverage Solutions

Beyond the big two, a few other options might be the perfect fit for your situation. Knowing what they are gives you the full picture.

Short-Term Health Insurance: If you just need to bridge a small gap—say, you start a new job in a month or two—a short-term plan could work. The premiums are very low, but so is the coverage. These plans often don't cover pre-existing conditions and aren't ACA-compliant. Think of them as a temporary safety net, not a real long-term solution.

Medicaid: Depending on your new household income and where you live, you or your family might now qualify for Medicaid. After a job loss, your income can easily fall into the eligible range. Medicaid offers comprehensive coverage for little to no cost, and you can apply anytime. It's always worth checking to see if you qualify.

By taking a moment to compare these different avenues, you can make a choice that truly protects your health and your wallet. For a deeper dive, you can learn more about these COBRA insurance alternatives and see which one makes the most sense for you.

When Paying the High Price for COBRA Makes Sense

After looking at the sticker shock of COBRA, it’s easy to think, “Nope, not for me.” But hold on. In a few key situations, that high premium isn't just a cost—it's one of the smartest investments you can make for your health and financial future.

Think of COBRA as your "do not disturb" sign for your healthcare. Sure, other plans might be cheaper, but they often mean starting from scratch: new doctors, new network, and a brand-new deductible. Sometimes, that kind of disruption is a far bigger risk than the monthly payment.

Protecting Your Continuity of Care

The biggest reason to stick with COBRA? Continuity of care. If you or someone in your family is in the middle of a serious health issue, switching plans can be a nightmare.

Just imagine these situations:

- You're undergoing ongoing specialized treatment for something like cancer, where changing your oncologist is simply not an option.

- You're in the middle of a high-risk pregnancy and have built trust with a specific OB-GYN and hospital.

- You have a major surgery scheduled with a top surgeon you've waited months to see.

In these moments, a new insurance plan might not cover your trusted doctors. The stress of finding new specialists, transferring all your records, and fighting for treatment approvals can cause dangerous delays. The stability COBRA offers is worth every single penny here.

Leveraging Your Annual Deductible

Here’s another big one: you've already paid most or all of your annual deductible for the year. Your deductible is the cash you have to shell out before your insurance plan starts picking up the majority of the tab.

Let's say your plan has a $5,000 deductible, and by September, you've already spent $4,800 out-of-pocket. You are so close to having your insurance cover almost everything else for the rest of the year. If you switch to a new plan, that deductible counter resets to $0.

The Financial Trap: Switching plans late in the year could force you to pay thousands toward a brand-new deductible, potentially costing you far more than a few months of high COBRA premiums.

Picture this: you lose your job in October after meeting your deductible. Paying $2,000 for COBRA to cover November and December might feel steep, but it saves you from having to meet a new $5,000 deductible for any end-of-year medical needs. You just saved yourself $3,000. It's simple math where the more expensive monthly option is actually the cheaper choice overall. This is especially critical for early retirees planning their transition. To see how this works in practice, you might find our guide on COBRA for retirees helpful for budgeting.

Keeping Your Prescription Drug Coverage

Finally, if you rely on specific, and often expensive, medications, COBRA can be a lifesaver. A new insurance plan could have a completely different list of covered drugs (called a formulary).

Your essential medication might not be covered at all, or it could be bumped to a higher-cost tier, leaving you with a massive bill at the pharmacy. Sticking with COBRA guarantees your prescriptions are still covered exactly as they were before. It means no interruptions in your treatment and no surprise costs, making that high premium a predictable and necessary expense.

Understanding COBRA Rules and Timelines

Knowing how much COBRA costs is only half the battle. You also have to navigate its strict rules and tight deadlines, where missing a single step can mean losing your right to coverage entirely.

Think of COBRA like a connecting flight. You have a very specific window to get to the gate, board, and pay for your ticket. If you miss it, the plane leaves without you, and you’re stranded. Let’s make sure you catch your flight.

Who Qualifies for COBRA Coverage

COBRA isn’t for everyone. It’s a specific protection for employees at certain companies who go through a major life event. The rules are straightforward, but they are absolute.

First, your former employer has to meet two conditions:

- They must have 20 or more employees.

- They must offer a group health plan.

If you worked for a very small business, you probably won't qualify under the federal COBRA law. However, some states have "mini-COBRA" laws that cover smaller companies, so it's always worth checking.

Next, you need to have a "qualifying event." This is the official trigger that makes you eligible to keep your health plan. These events are clearly defined, but you can see a full breakdown in our guide explaining what is a qualifying event for health insurance.

The most common ones are:

- Losing your job, whether you quit or were laid off (as long as it wasn't for "gross misconduct").

- Having your hours cut, causing you to lose your health benefits.

Qualifying events also cover spouses and dependent children if they lose coverage because of a divorce, the employee's death, or a child aging out of the plan.

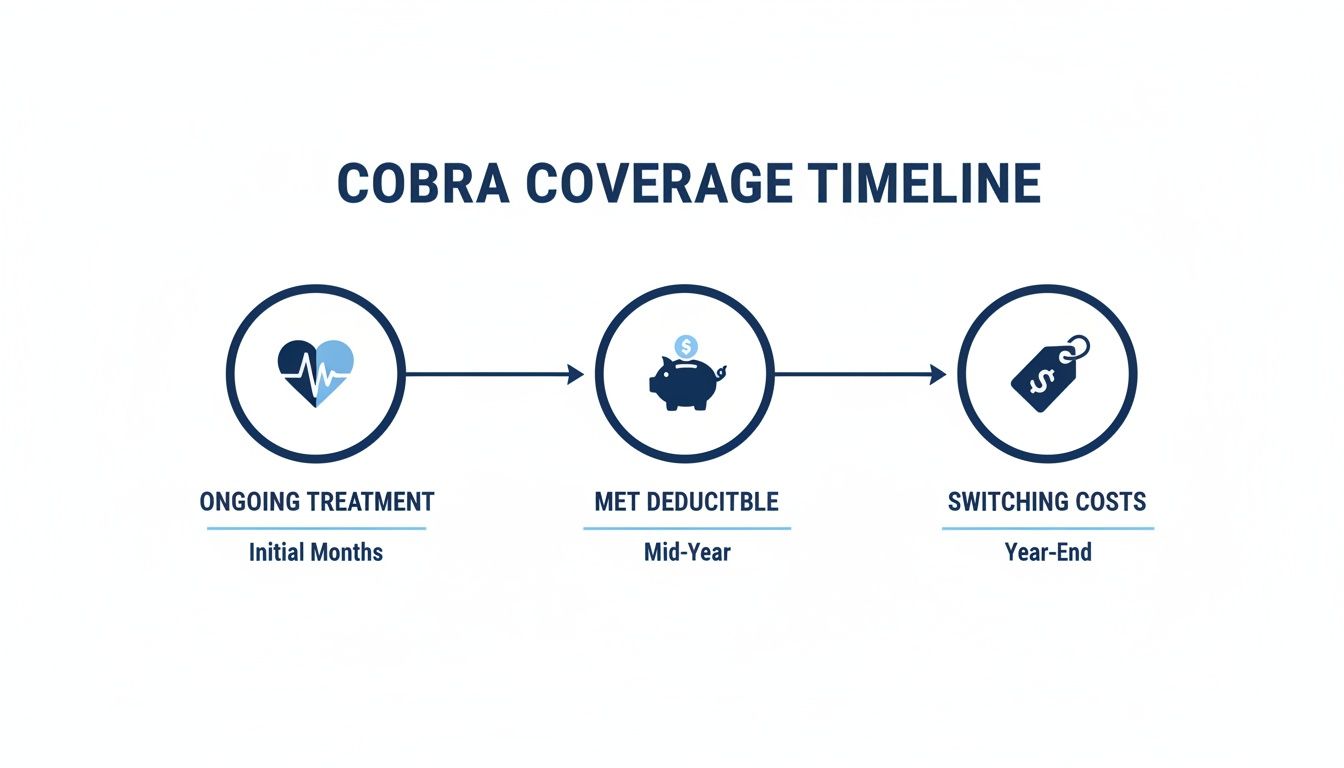

This timeline shows some of the key decision points when you’re weighing COBRA’s high cost against its benefits.

As you can see, COBRA makes the most sense when you’re in the middle of ongoing treatment or have already met your deductible for the year. Switching plans would just reset your progress.

How Long COBRA Coverage Lasts

Once you’re on COBRA, how long you can keep it depends on why you qualified in the first place. For most people, the timeline is pretty standard.

The Standard Rule: If you lost your job or your hours were reduced, you can typically keep COBRA coverage for up to 18 months. This is the most common situation and gives you a solid bridge to find new, long-term insurance.

In certain cases, though, you might get a longer safety net.

- Up to 29 Months: If someone is determined to be disabled by the Social Security Administration while on COBRA, their coverage can be extended to 29 months.

- Up to 36 Months: Spouses or dependent children may get up to 36 months of coverage if their qualifying event was the employee's death, divorce, or Medicare eligibility.

The Clock Is Ticking: Critical Deadlines

The COBRA process is all about deadlines. You can’t ignore them. If you miss one, you will lose your eligibility for good, with very few exceptions.

Here’s how the timeline breaks down:

- The Employer's Notice (14-44 Days): After you leave your job, your employer has between 14 and 44 days to notify the health plan administrator.

- Your Election Period (60 Days): Once you get that notification, a 60-day clock starts ticking. This is your window to decide whether you want to elect COBRA.

- Your First Payment (45 Days): After you say "yes" to COBRA, you have 45 days to make your first premium payment. Keep in mind, this payment is retroactive—it covers you all the way back to the day you lost your original coverage.

These deadlines are firm. If you run into complex issues or disputes, you may need to consult a lawyer to understand your rights. Watch your mail closely and act fast—it's the only way to make sure you don't accidentally give up your right to stay covered.

Got Questions About COBRA? We’ve Got Answers.

Figuring out COBRA can feel like a puzzle, especially with deadlines looming and big costs on the line. It's completely normal to have questions. Here are some simple, straightforward answers to the things people ask most.

I Quit My Job—Can I Still Get COBRA?

You sure can. Deciding to leave your job is what’s known as a “qualifying event,” and it almost always makes you eligible for COBRA.

The only real exception is if you were let go for “gross misconduct,” which is a very high legal bar and rarely ever comes into play. So, if you resigned on your own terms, you’re in the clear.

Does My Old Boss Have to Pay for My COBRA?

Nope. Your employer isn’t required to chip in for your COBRA premiums. The whole point of the law is to let you keep the plan, but you become responsible for the entire cost.

That means you’ll pay 102% of the total premium—the slice you used to pay from your paycheck, plus the much bigger chunk your employer covered. Occasionally, an employer might offer to help pay for it as part of a severance deal, but that’s a generous perk, not a legal obligation.

What Happens If I Forget to Pay My COBRA Bill?

This is a big one. Missing a payment can get your coverage terminated for good, and there are no do-overs.

You do get a grace period, which is usually about 30 days from your due date. But if you miss that deadline, your health plan will be canceled, going all the way back to the last day of the month you paid for.

Here’s the bottom line: Always, always pay your COBRA premium on time. Once you miss that grace period, the door closes permanently on your coverage.

Can My Spouse and Kids Get COBRA Even If I Don’t?

Absolutely. This is a great feature of the law. Every person covered under your old plan—you, your spouse, your kids—is considered a “qualified beneficiary.”

Each of you has an independent right to choose COBRA. So, if you find a better plan for yourself on the ACA Marketplace, your spouse and children can still enroll in COBRA to keep their doctors and coverage. It’s a flexible way to make sure everyone in the family stays protected without interruption.