Trying to make sense of your health insurance policy can feel like you're trying to learn a whole new language. Two words you’ll see everywhere are deductibles and copays, and they’re often the most confusing parts of the puzzle.

Getting a handle on how these work is your first real step toward taking control of your healthcare spending and, more importantly, avoiding those dreaded surprise bills. They’re the two main ways you and your insurance company share the cost of your medical care.

Decoding Your Health Insurance Costs

So, what’s the real difference? Think of it like this: your deductible is the amount you have to pay out of your own pocket for covered medical services before your insurance plan starts to chip in. A copay, on the other hand, is a small, fixed fee you pay for certain services, like a doctor's visit, every single time you go—whether you've met your deductible or not.

Here’s a simple breakdown:

- Deductible: This is a big-picture number, an annual threshold you have to cross. Until you’ve spent this amount on most types of medical care, you’re on the hook for the full cost.

- Copay: This is a small-picture fee. It’s that predictable $25 or $50 you hand over at the front desk for a routine check-up or when you pick up a prescription. It’s a set cost that often applies from day one.

A Simple Analogy

Let’s imagine your health coverage is like a special club membership for an amusement park. Your deductible is the one-time annual pass fee you have to pay before the park covers the cost of the big rides. You pay that fee once, and then you’re good for the year.

A copay, in this scenario, is like the small, fixed price you pay for the carnival games inside the park. You pay it each time you want to play, and it’s completely separate from that main annual pass fee.

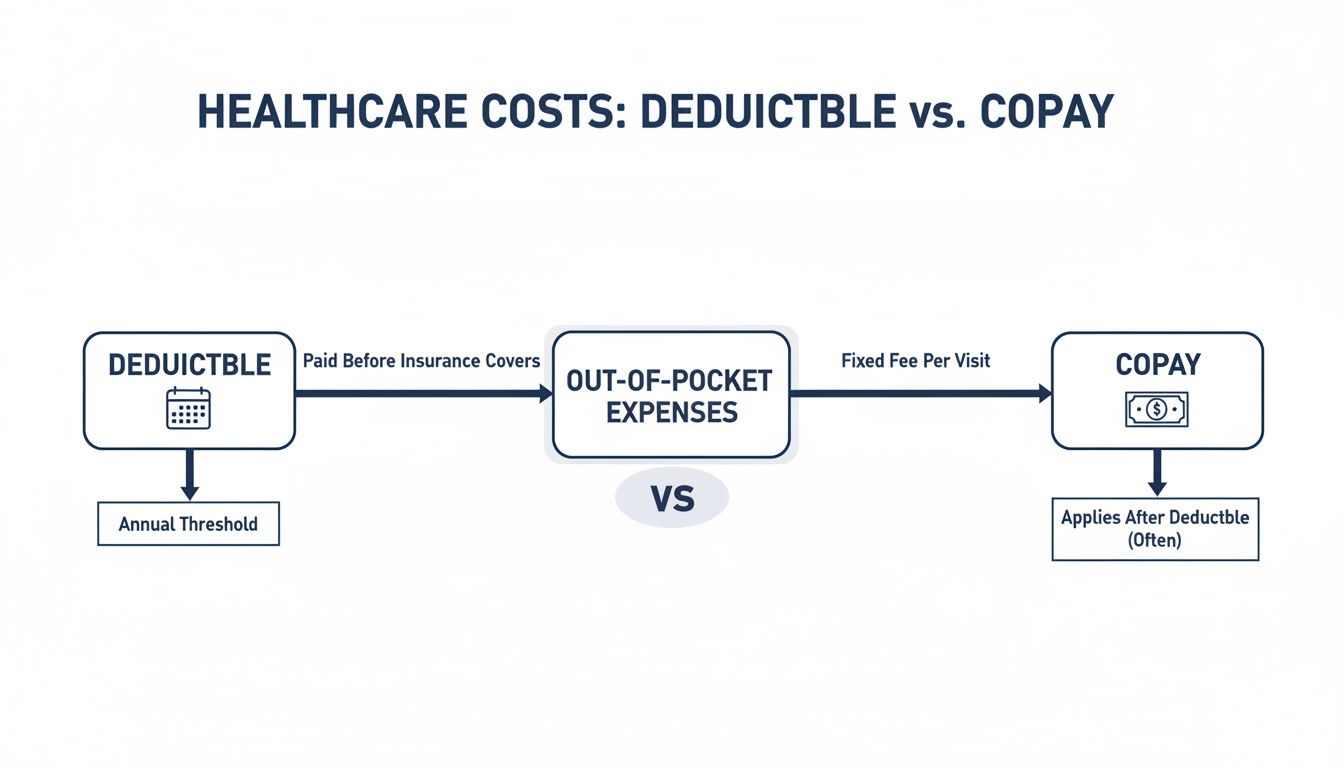

This flowchart gives you a great visual for how these two costs fit into the bigger picture of your out-of-pocket expenses.

As you can see, the deductible is a bigger financial hurdle you clear once a year, while a copay is a much smaller, more frequent cost for specific services.

To help you keep these two terms straight, here's a quick side-by-side comparison.

Deductible vs Copay At a Glance

| Feature | Deductible | Copay |

|---|---|---|

| What It Is | The total amount you pay before insurance starts covering costs. | A fixed fee you pay for a specific service or prescription. |

| When You Pay | Paid for covered services until the annual total is met. | Paid at the time of service, every time. |

| How It Works | A running total that resets each year. | A flat rate that doesn't count toward your deductible. |

| Typical Amount | Larger amounts, typically hundreds or thousands of dollars. | Smaller amounts, usually between $15 and $75. |

| Example | You pay the first $2,000 of your hospital bill. | You pay $30 every time you see your primary care doctor. |

Ultimately, understanding the relationship between your deductible and copay is what empowers you to pick a plan that truly fits your life and budget.

Of course, insurance is filled with all sorts of terminology. If you come across other terms that leave you scratching your head, our complete health insurance glossary is a great resource to have bookmarked. And while these are core concepts in the U.S., different models of cost-sharing are used all over the world. For those living abroad, exploring resources on international medical insurance for expats can shed some light on how coverage works in other countries.

How Your Health Insurance Deductible Really Works

Think of your health insurance deductible as the amount you have to pay for your healthcare before your insurance company starts chipping in. It’s like a financial starting line you cross each year. Until you’ve paid that specific amount out of your own pocket for covered services, you're handling most of the bills yourself.

Once you hit that number, a switch flips. Your insurance kicks in and begins to share a big part of the costs. This is one of the most important parts of your plan, directly shaping how much you spend both monthly and when you actually need care.

This "starting line" isn't a one-time thing. It resets every single plan year, which for most people is January 1st. Nothing you paid toward last year’s deductible carries over. On day one of your new plan, the counter goes right back to zero, and you start working toward meeting it all over again.

The Trade-Off Between Deductibles and Premiums

There’s a constant balancing act in health insurance, and it’s most obvious with deductibles and your monthly premium. Here's the deal: plans with higher deductibles usually come with lower monthly premiums. If you’re pretty healthy and don’t see the doctor often, this can be a really smart financial move.

On the flip side, a lower deductible means your insurance starts paying its share much sooner, but you'll pay a higher premium every month for that peace of mind. You’re essentially choosing between paying less now (with a lower premium) or paying less later if you get sick or injured (with a lower deductible).

Key Insight: Don’t think of your deductible as a penalty. See it as a strategic choice. It's your way of aligning your health insurance costs with your budget and what you realistically expect to need for the year.

Deductibles can be all over the map. The average annual deductible for workers with single coverage on an employer plan hit $1,886. But if you work at a smaller company, that number jumps to an average of $2,631. In fact, a full 34% of all covered workers are now in plans with deductibles of $2,000 or more for single coverage alone.

Individual vs. Family Deductibles

If you have kids or a spouse on your plan, things get a little more complex. Your plan likely has two different deductibles you need to know about.

- Individual Deductible: This is the amount each person on the plan has to meet on their own.

- Family Deductible: This is the combined total for everyone on the plan. Once the family's spending hits this number, the insurance starts paying for everyone, even if some members haven't met their individual deductible yet.

Let's say your family plan has a $3,000 individual deductible and a $6,000 family deductible. If one person has a rough year and hits their $3,000 mark, the insurance company starts covering their costs. But if the whole family's combined medical bills reach $6,000, the plan’s cost-sharing kicks in for every single person on the policy for the rest of the year. Making sure you understand the specific deductible for health insurance in your plan is the key to avoiding surprise bills.

Making Sense of Copays for Everyday Care

If your deductible is the big, once-a-year hurdle, think of copays as the predictable, everyday part of your health insurance. A copay is just a simple, flat fee you pay for a specific service. It's a lot like buying a ticket to see a movie—you pay a fixed price right at the counter, every time.

This is what makes routine healthcare feel manageable. Whether you're heading to your family doctor for a check-up or grabbing a prescription, you know exactly what you'll owe. No complicated math, no surprise percentages. Just a straightforward cost.

Why Copay Amounts Vary

You've probably noticed that not all copays are created equal. Your insurance plan will list different copay amounts for different types of care, and that's by design. The structure reflects the cost and urgency of the service you’re getting.

Here’s what you’ll typically see:

- Primary Care Physician (PCP) Visit: This is almost always your lowest copay, encouraging you to stay on top of your health. (e.g., $25)

- Specialist Visit: Seeing a specialist, like a cardiologist or dermatologist, will cost a bit more. (e.g., $50)

- Urgent Care Visit: For those times you need immediate help for something that isn’t life-threatening. (e.g., $75)

- Emergency Room (ER) Visit: This is the highest copay by far, steering you away from using it unless it's a true emergency. (e.g., $250 or more)

This system is designed to give you clear financial signals, helping you choose the right level of care for your situation.

Key Takeaway: Copays bring predictability to your daily healthcare costs. They are fixed fees you pay for specific services, and they operate independently from your annual deductible.

How Copays and Deductibles Interact

So, how do these two work together? This is where a lot of people get tripped up. In most health plans, your copayments do not count toward your annual deductible.

This means you’ll pay that flat copay for routine visits right from day one, no matter where you are with your deductible.

Let’s say you have a $3,000 deductible and a $30 copay for doctor visits. You will pay that $30 every single time you see your doctor. That payment won’t chip away at the $3,000 you still need to cover for bigger things like lab work or a hospital stay. However, your copays almost always do count toward your plan's out-of-pocket maximum for the year. To see how this plays out in more detail, our guide explains how does copay work in different situations.

How These Costs Shape Your Financial Health

Knowing the definitions of deductibles and copays is a good start, but what really matters for your budget is seeing how they work together in the real world. Think of them as the two main levers insurance companies use to manage costs. How they're balanced directly shapes what you'll actually pay for care throughout the year.

It's all about a trade-off.

A plan with a high deductible can feel great month-to-month because your premium is lower. But one unexpected trip to the ER could leave you facing a massive bill. On the flip side, a low-deductible plan gives you predictable costs but locks you into a higher payment every single month. Finding the right balance is everything.

This isn't a random setup. To keep monthly premiums from skyrocketing, many plans are designed to shift more of the initial financial burden to you when you need care. It’s a strategy to keep those monthly payments manageable, but it means you need to be prepared for upfront costs.

A Real-World Family Scenario

Let’s watch this play out for the Millers, a family of four. Their plan has a $5,000 family deductible and set copays for simple, routine stuff.

- Routine Doctor Visits: Their son gets an ear infection. The visit costs them a $40 copay right at the clinic. Simple enough. But this payment does not chip away at their $5,000 family deductible.

- Unexpected ER Trip: A few months later, their daughter takes a tumble and needs stitches. The emergency room bill comes to $2,500. Because they haven't hit their deductible yet, they have to pay that entire amount themselves. Ouch.

- Post-Deductible Spending: The Millers have now paid $2,500 toward their $5,000 deductible. For any future care that counts toward it, they only have $2,500 left to cover before their insurance starts paying a much bigger share.

This just goes to show how a single accident can totally change your financial picture, even when you have insurance. The family's predictable copays made everyday care affordable, but that big deductible meant they were on the hook for the full cost of the emergency.

The High-Deductible Plan Strategy

So, who would want a high deductible? For people who are generally healthy and have some money saved up, a high-deductible health plan (HDHP) can be a really smart move. The lower monthly premiums free up cash that you can put into a tax-advantaged Health Savings Account (HSA).

An HSA lets you save pre-tax money specifically for medical expenses—including your deductible. It turns a high deductible from a scary risk into a structured, tax-savvy way to save.

These plans reward you for being proactive. By funding an HSA, you're building a financial safety net to cover your deductible if something major happens. It’s a powerful combo: low monthly costs plus a tax-free way to prepare for the unexpected. You can learn more in our guide on what you can use your HSA for.

Ultimately, it comes down to you. Your health, your savings, and your comfort with risk will decide if the lower premiums of an HDHP are worth the trade-off.

Choosing a Health Plan That Fits Your Life

The "perfect" health plan isn't a one-size-fits-all solution. It's the one that fits you—your budget, your family's needs, and where you are in life. Understanding how deductibles and copays work together is the key to finding that perfect fit, so you get the security you need without overpaying. What works for a young freelancer is almost always the opposite of what a growing family needs.

Let's walk through a few common scenarios. This will help you build a mental framework for figuring out your own needs and making a choice you can feel good about.

For Young and Healthy Individuals

If you're young, healthy, and rarely see a doctor outside of an annual physical, your number one goal is probably keeping monthly costs down. This is where a High-Deductible Health Plan (HDHP) usually makes the most sense.

That high deductible number can look scary, but think about it: if you're not using much medical care, you're unlikely to ever have to pay it. The real wins here are the lower monthly premiums that free up your cash flow and the ability to open a Health Savings Account (HSA). An HSA lets you save pre-tax money for medical expenses, creating a tax-advantaged safety net just in case.

For Growing Families with Children

Life with kids is beautifully unpredictable. So are the healthcare needs that come with it. Between pediatrician checkups, sudden fevers, and the occasional playground injury, your family's top priority is predictability, not rock-bottom premiums.

For this stage of life, a plan with a lower deductible and clear, affordable copays is often the way to go. Yes, you'll pay a higher monthly premium. But in exchange, you get priceless peace of mind knowing a sick visit won't end with a surprise bill for hundreds of dollars. You're paying a bit more each month to make sure your day-to-day medical costs are manageable and expected.

The Right Fit: The goal isn't just to find the cheapest plan, but the one with the right cost structure for your life. Your choice in deductibles and copays should reflect how often you expect to need care.

For Adults Nearing Retirement

As you get closer to your pre-Medicare years (usually ages 60-64), your healthcare needs often become more consistent. This is the time to strike a careful balance between your monthly premium and your potential out-of-pocket costs.

While a low premium is always nice, a sky-high deductible could become a huge financial burden if you suddenly need a procedure or more regular care. Many people in this age group find a middle-ground plan—one with a moderate deductible and reasonable copays—offers the best of both worlds. It protects you from catastrophic costs without the hefty monthly price tag of a premium low-deductible plan.

It's also a great time to start thinking ahead and understanding how your benefits transition into the next chapter, like learning about federal retirement health benefits. Seeing the full picture helps ensure you're prepared for a smooth and secure retirement.

To make it even simpler, here’s a quick guide matching life situations with the plan structures that often work best.

Best Plan Type by Life Stage

| Life Stage / Persona | Typical Healthcare Needs | Often The Best Fit |

|---|---|---|

| Young & Healthy Freelancer | Low; mostly preventive care or unexpected emergencies. | High-Deductible Plan (HDHP) with an HSA. |

| Growing Family with Kids | High; frequent doctor visits, checkups, and minor illnesses. | Low-Deductible Plan with predictable copays. |

| Pre-Medicare Adult (60-64) | Moderate to high; more consistent care, potential procedures. | Moderate-Deductible Plan for a balance of costs. |

Ultimately, choosing the right plan is a personal decision based on your unique circumstances. By thinking through how you actually use—or expect to use—your healthcare, you can pick a plan that truly serves you.

A Look at the Bigger Picture: It’s Not Just You

If you've ever felt overwhelmed trying to balance monthly premiums with what you actually pay for care—like deductibles and copays—you're not alone. Far from it. This financial balancing act is part of a much larger, global trend.

Around the world, more and more countries are using direct patient payments to keep their healthcare systems afloat. That means families everywhere are facing the same kinds of tough financial choices when they need to see a doctor. This isn't just a small detail; it’s a major shift in how healthcare is funded worldwide.

Out-of-pocket costs—everything from your deductible to what you pay for a prescription—financed more than 20% of all healthcare spending in 126 different countries. Even in high-income nations, patients covered about 18.4% of the bill themselves. For others, that number is even higher, showing a real strain on personal finances when it comes to staying healthy. You can see more on this in a recent report about global healthcare funding inequalities.

Why This Global View Matters

Seeing the bigger picture helps drive home a crucial point: you have to be your own best advocate. The challenge of juggling upfront insurance costs with long-term medical needs isn't going away anytime soon. The most powerful thing you can do is become an informed, proactive healthcare consumer. It's your best defense for protecting both your health and your wallet.

By taking the time to understand how deductibles and copays work, you're not just learning insurance jargon. You're building a critical life skill for managing one of the biggest expenses we all face.

This is why digging into the details of your health plan is so important. When you carefully compare how different combinations of deductibles and copays will impact your budget, you’re on the path to finding a plan that gives you real security—not just the illusion of it. That knowledge is what empowers you to make a confident choice that truly works for you.

Still Have Questions? We’ve Got Answers.

Once you get a feel for the basics, a few practical questions almost always pop up. It’s one thing to know the definitions, but it’s another to see how they play out in the real world.

Let's clear up some of the most common head-scratchers we hear.

Does My Copay Count Toward My Deductible?

This is a big one. The simple answer is almost always no.

Think of it like this: your copay is a separate, flat fee you pay for a specific service, like seeing your doctor. It's like paying a cover charge at a concert. That payment doesn't lower the price of the merchandise inside. Similarly, your copay doesn't chip away at your annual deductible.

However—and this is important—your copays do count toward your out-of-pocket maximum. That’s the absolute most you’ll spend on covered care in a year. Your deductible is one bucket you have to fill, but the out-of-pocket max is the giant safety net that catches everything, including your copays.

What Happens After I Finally Meet My Deductible?

Hitting your deductible is a huge milestone! This is the moment your insurance plan really kicks into gear and starts sharing the costs with you. You aren't totally off the hook for payments, but your share of the bills drops way, way down.

Now, you’ll start paying coinsurance. Instead of the full bill, you’ll only be responsible for a percentage. For example, your plan might have 20% coinsurance. If you get a $1,000 hospital bill, you’d pay $200 and your insurer would cover the other $800. You'll keep paying your regular copays and your coinsurance share until you hit that all-important out-of-pocket maximum.

The Big Picture: Meeting your deductible is the turning point. It’s where your insurance shifts from being a just-in-case safety net to an active financial partner. And once you reach your out-of-pocket max for the year, your insurer covers 100% of your eligible medical costs. You're covered.

Can a Plan Have a Deductible but No Copays?

Yes, absolutely. This is actually pretty common, especially with High Deductible Health Plans (HDHPs).

These plans are built to be straightforward. You are responsible for 100% of your medical bills until you meet that higher deductible. There are no separate copays for doctor visits or prescriptions; it all just goes toward that one single number.

Once you hit it, your coinsurance kicks in. The trade-off is that these plans often come with much lower monthly premiums and are the only plans that let you open a Health Savings Account (HSA)—a fantastic tool that lets you save for medical expenses completely tax-free.

Feeling more confident about deductibles and copays is the first step. The next is finding a plan that actually fits your life.

At My Policy Quote, we cut through the confusion and make it easy to see your options side-by-side. Get a clear, no-hassle quote today and see what’s out there for you. Start your free quote at mypolicyquote.com.