The easiest way to understand the difference between term vs. whole life insurance boils down to a simple analogy: term life is like renting a home, while whole life is like owning one.

One gives you temporary, affordable protection for a specific time. The other provides permanent, lifelong coverage that also builds cash value—a financial asset for your future.

Breaking Down Term vs Whole Life Insurance

Choosing between these two isn't just a financial decision; it's a foundational step in mapping out your family's security. One is a pure safety net, designed to protect you when you need it most. The other is a long-term financial instrument. To pick the right one, you need to be crystal clear on what you want it to accomplish.

For a lot of people, the choice isn't obvious right away. It all comes down to your financial situation, your long-term goals, and the why behind your search for insurance.

Are you trying to cover a 30-year mortgage and make sure your kids can afford college if you're not around? Or are you thinking bigger, like planning your estate and leaving a permanent legacy? For a deeper look at the basics, our guide on life insurance for dummies is a great place to start.

Key Differences at a Glance Term vs Whole Life

To make it even clearer, I've put together a quick comparison. This table strips away the jargon and gets straight to the point, showing you how each policy stacks up on the features that matter most.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Policy Duration | Temporary coverage for a fixed period (e.g., 10, 20, 30 years). | Permanent coverage that lasts for your entire lifetime. |

| Cost | Significantly lower premiums, making it highly affordable. | Substantially higher premiums due to lifelong coverage and cash value. |

| Cash Value | None. It is a "pure" insurance product with no savings component. | Includes a savings component that grows at a guaranteed rate over time. |

| Primary Purpose | To cover specific, temporary financial needs like a mortgage or raising children. | To provide lifelong protection, plan for estate taxes, and build a financial asset. |

Think of this table as your cheat sheet. It highlights the fundamental trade-offs you'll be making. With term life, you're prioritizing affordability and specific-term protection. With whole life, you're investing in permanence and building an asset, which naturally comes at a higher cost.

How Term Life Insurance Delivers Pure Protection

Term life insurance is built on a simple, powerful idea: getting the most protection for the lowest cost, but only for a specific time. Think of it as "pure" life insurance. You pay a premium for a set term—usually 10, 20, or 30 years—and if you pass away during that time, your loved ones get a tax-free payout. That’s it.

There’s no complicated savings account attached or any investment component to track. This straightforward design is actually its biggest strength. It makes term life an incredibly efficient tool for covering temporary, but massive, financial risks, creating a safety net when your family needs it most.

This kind of policy is perfect when your biggest financial responsibilities have a clear finish line. For instance, if you have a 30-year mortgage or young kids who will be on their own in about 20 years, you can line up a term policy to match those timelines perfectly.

Matching the Policy to Your Needs

The real key to making term life insurance work for you is matching the policy's length and coverage amount to your specific debts and the income your family would need to replace. When you get that alignment right, you ensure your family isn't left scrambling.

You'll generally run into two main variations:

- Level Term: This is the one most people get. Your premium and your death benefit stay exactly the same for the entire term. It offers predictability and is perfect for things like replacing your income.

- Decreasing Term: You don’t see this as often anymore, but it's designed for a specific job. The death benefit slowly shrinks over time, often set up to mirror the shrinking balance of a big loan, like a mortgage.

The real value of term life is its affordability and sharp focus. It solves one problem—temporary risk—without tacking on the cost or complexity of a lifelong investment product.

Many people find that a deeper dive into a term life insurance comparison helps them see exactly which term length and type truly fits their situation.

One last thing—a super valuable feature to look for is a conversion rider. This little add-on gives you the right to convert your term policy into a permanent whole life policy later, without having to pass another medical exam. It gives you incredible flexibility, letting your coverage adapt as your life changes. It’s a smart move that keeps your options open for the future.

Whole Life as a Financial Asset—More Than Just a Policy

While term life is pure protection, whole life insurance is a different beast altogether. Think of it as a long-term financial tool, not just a safety net. It uniquely combines a permanent death benefit with a tax-deferred cash value account, which is the real game-changer in the term vs. whole life debate.

A piece of every premium you pay goes into this cash value, which grows at a guaranteed rate set by your insurer. This creates a powerful living benefit—a stash of capital you can tap into while you’re still alive, completely separate from the money meant for your loved ones.

Putting Your Policy’s Cash Value to Work

This cash value isn't just a number on a page; it's a real, liquid asset. Policyholders have a few smart ways to use these funds, giving them serious financial flexibility when life throws a curveball or an opportunity.

- Policy Loans: You can borrow against your cash value, often at a great interest rate, and you don’t even need a credit check. You don't have to pay these loans back on a strict schedule, but just remember that any outstanding balance will reduce the final payout to your beneficiaries.

- Withdrawals: Need cash? You can pull funds directly from your cash value. It's often a tax-free way to get money (up to the amount you’ve paid in premiums), but doing so will permanently lower your policy's death benefit and cash value.

A whole life policy is more than just insurance; it’s a disciplined savings vehicle with a built-in death benefit. It forces consistent savings and guarantees growth, creating a predictable financial resource for the long haul.

On top of that, many whole life policies come from mutual insurance companies, which might pay out non-guaranteed dividends. If your policy earns them, you can use these dividends to buy more coverage, pay your premiums, or just let them turbocharge your cash value growth. It's a powerful way to compound your asset over time.

This structure makes whole life a cornerstone for specific financial game plans. People use it for estate planning, setting up a fund for a dependent with lifelong needs, or even to create a stream of supplemental retirement income. When you’re thinking about whole life this way, it's also crucial to understand how life insurance proceeds are handled in an estate, especially when it comes to probate. A great next step is to explore the best whole life insurance policies to find a plan that lines up with these bigger financial goals.

A Realistic Look at the Cost of Coverage

When you stack term life and whole life insurance side-by-side, the first thing that jumps out is the price tag. And it’s not a small difference. This gap in cost is fundamental, and it’s what really shapes who each policy is for and what it’s meant to do.

Think of it this way: term life is designed for pure, affordable protection. Whole life, on the other hand, comes with a higher cost because it's doing two jobs at once—providing a death benefit and building a financial asset. The difference in your monthly payment can be massive, so it’s something you need to get right from the start.

Premiums By the Numbers

Let's put this into real-world perspective.

A healthy 40-year-old man looking for a 20-year term life policy with a $500,000 death benefit might pay around $335 a year. That’s straightforward protection for his family during his highest-earning years.

Now, for that same man and the same $500,000 death benefit, a whole life policy could cost over $7,000 annually. That’s a premium nearly 20 times higher.

The long-term impact is staggering. Over 30 years, that price difference could add up to more than $140,000. This isn’t a small budget tweak; it’s a major financial commitment that demands a serious look at your long-term income and goals.

The real reason for the cost difference is what you're buying. With term life, you're just paying for the death benefit for a specific time. With whole life, that bigger premium covers the death benefit, builds up a cash value account, and pays the higher fees for managing a policy that lasts forever.

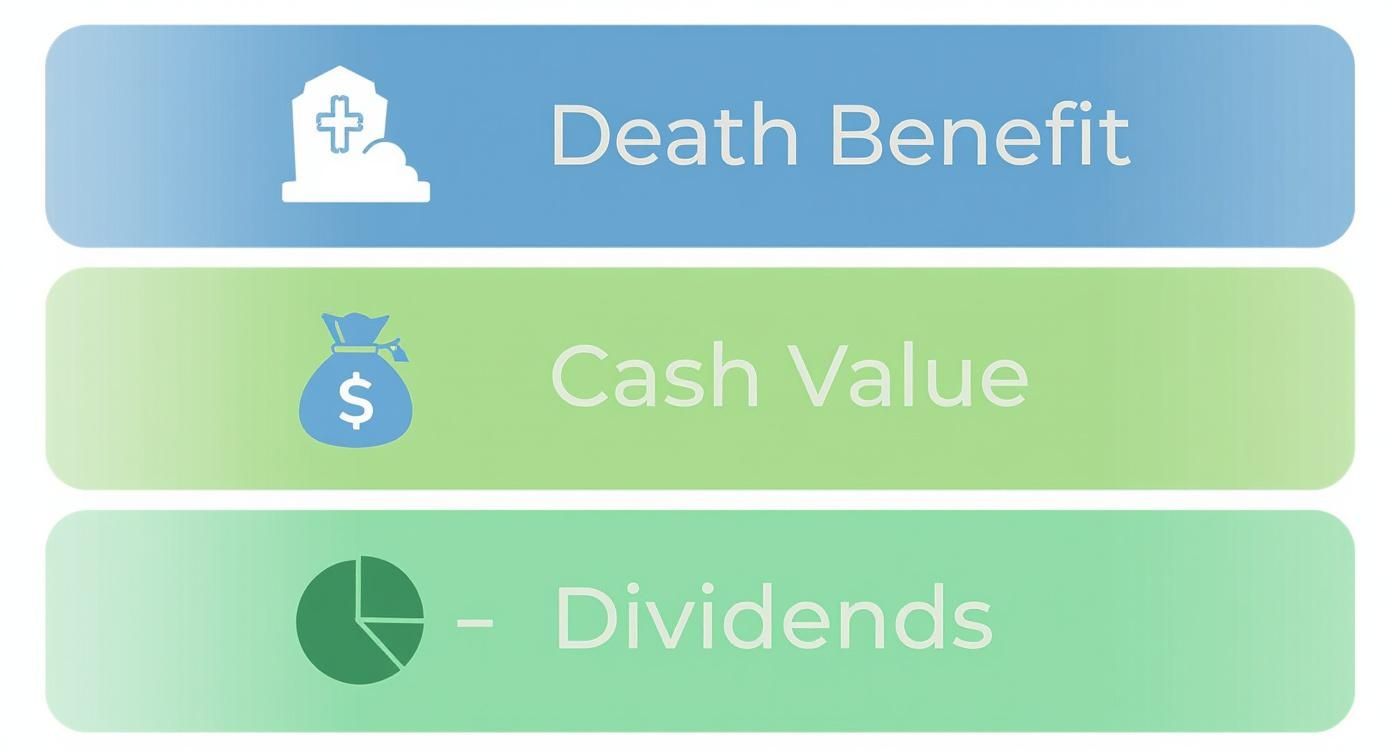

This infographic gives a great visual of how a whole life premium is divided.

As you can see, your money isn't just going to one place. It’s split between the actual insurance cost, a savings component (your cash value), and even potential dividends.

What Is an Insurance Premium Actually Paying For?

It really helps to understand where your money is going. Those monthly payments aren't just random numbers; they’re carefully calculated to cover specific risks and features.

Here's a simple way to break it down:

- Term Life Premium: This payment almost entirely covers the cost of insurance (COI). It’s what the insurer needs to cover the risk of paying out your death benefit while the policy is active. Simple and direct.

- Whole Life Premium: This payment is doing a lot more work. It’s split between a few key areas:

- It covers the cost of insurance for a policy designed to last your entire life.

- A large chunk gets funneled into your policy's cash value account, which grows over time.

- It also covers the insurer's administrative fees and other costs of managing a permanent product.

Taking a moment to understand what an insurance premium is can clear up a lot of confusion. The higher cost of whole life is a direct result of it being a more complex financial tool built for the long haul.

Which Policy Fits Your Life Stage?

There’s no single "best" life insurance policy. The real question is: what's the right financial tool for your life, right now?

A policy that makes perfect sense for a young family just buying their first home would be a terrible fit for a business owner planning their exit strategy. The right choice is always personal. It’s about your story, your goals, and what you need the insurance to do.

Let's skip the one-size-fits-all answers and look at how these policies work in the real world for different people. Seeing them in action is the best way to figure out which one lines up with your life.

For Young Families and New Homeowners

When you’re starting a family, you’re often at your most financially vulnerable. You’ve got a new mortgage, daycare costs, and the looming reality of college tuition. Your biggest need? Maximum protection for the lowest possible cost.

In this situation, term life insurance is almost always the answer.

It’s designed for this exact purpose: to provide a huge safety net for a small price. A term policy ensures your family can stay in their home, pay the bills, and keep their dreams on track during the 20 or 30 years they need that protection most.

A 2023 study confirmed just how effective this is. It found that households with only term life insurance were 3.95 times more likely to be financially secure after losing a loved one. It’s powerful proof that term delivers when families are counting on it. You can discover more insights from the study about achieving financial security.

For High-Net-Worth Individuals and Estate Planning

Once you've built significant wealth, your focus shifts. It's less about replacing income and more about protecting your legacy. Life insurance becomes a strategic tool to make sure your assets are transferred smoothly and efficiently.

This is where whole life insurance shines.

Its permanence guarantees a payout, no matter when you pass away. The cash value also grows into a stable, tax-deferred asset that can be used for opportunities or emergencies. This policy can provide the instant liquidity needed to pay estate taxes, preventing your heirs from being forced to sell off a family business or real estate just to settle the bills.

For affluent individuals, the conversation changes from "What if I die too soon?" to "How can I ensure my legacy is protected when I die?" Whole life insurance directly answers this by creating a permanent, tax-advantaged source of funds for final obligations.

For Small Business Owners

Business owners juggle a unique set of risks. You might need to secure a loan, protect against the loss of a key partner, or create a succession plan.

A term policy is often the perfect tool for securing a Small Business Administration (SBA) loan, since you only need coverage for the life of the loan.

But for bigger goals, like funding a buy-sell agreement, a whole life policy often makes more sense. The cash value can build up over time and eventually provide the funds needed to buy out a deceased partner's share, ensuring the business continues without a hitch. The best choice depends entirely on whether the goal is short-term protection or long-term strategy.

So, How Do You Actually Choose?

Figuring out the whole term vs. whole life thing isn't about finding some secret "best" option. It's about looking at your life, your goals, and your wallet—and then picking the tool that fits.

To get to the heart of it, ask yourself a few honest questions:

-

What am I really trying to do here? Am I just looking for a massive safety net for the lowest possible price while my kids are growing up? Or am I trying to build a permanent financial anchor for things like final expenses or leaving a legacy?

-

What can I realistically afford? The premiums on a whole life policy are no joke. Can I truly commit to paying them for decades without it getting in the way of other must-haves, like saving for retirement?

-

How disciplined am I with money? Do I need the "forced savings" of a whole life policy to make sure the money gets put away? Or am I the type of person who will actually take the money I save on premiums and invest it myself?

The "Buy Term and Invest the Difference" Idea

This is a classic strategy, and it’s popular for a reason. You buy an affordable term life policy and then take the money you saved and invest it.

For instance, instead of dropping $7,000 a year on a whole life policy, you could pay just $335 for term insurance. That leaves you with an extra $6,665 to invest every single year.

This approach gives you way more flexibility and the chance for much higher returns. But here's the catch: it's all on you. It only works if you have the discipline to actually invest that difference, year in and year out.

Ultimately, your choice boils down to this trade-off.

Whole life offers guarantees and a hands-off savings plan, but it comes with a hefty price tag. Term life, combined with your own investing, gives you freedom and growth potential, but it demands your active participation.

There’s no wrong answer—only the one that aligns with your budget, your long-term vision, and your own financial personality.

Frequently Asked Questions

When you dig into the insurance term vs whole life conversation, a few questions always seem to pop up. It’s totally normal. Getting these details straight is the only way to feel confident you're making the right choice for your family's future. Let's clear up some of the most common ones.

Can I Have Both Term and Whole Life Insurance at the Same Time?

You absolutely can. In fact, it's a smart strategy that many people use, often called "layering" or "laddering." It lets you blend the best of both worlds to build a financial safety net that truly fits your life.

Think of it this way: you could get a large, affordable term life policy to handle the big, temporary responsibilities—like a 30-year mortgage or getting your kids through college. At the same time, you could have a smaller whole life policy to guarantee a permanent benefit for final expenses or to leave a legacy, no matter when you pass away.

What Happens if I Outlive My Term Life Policy?

Once your policy’s term ends, the coverage just…stops. You’re no longer making payments, and the insurance company is no longer on the hook for a death benefit. It's as simple as that.

Unless you paid extra for a special "return of premium" rider, you don't get a refund for the premiums you paid. From there, you can either let the policy expire, shop for a new one (which will be more expensive since you're older), or, if your policy allows it, convert it to a permanent plan. If you're looking for more in-depth guidance, you can find additional resources on life insurance to help explore what's next.

Outliving your term policy isn't a waste of money. It’s a win. It means the insurance did its job perfectly—it kept your family safe during the years they needed that protection the most.

Is the Cash Value Part of the Whole Life Death Benefit?

This is a really important point to understand: the cash value and the death benefit are two different things. The death benefit is what your family gets. The cash value is a living benefit you can tap into while you're still here.

With most standard whole life policies, your beneficiaries receive the policy's stated death benefit when you pass away. The insurance company generally keeps the cash value you've built up. It's better to think of the cash value as an advance on the death benefit, not something extra that gets paid on top of it.

At My Policy Quote, we make finding the right life insurance simple. Compare personalized quotes in just a few minutes and start building a secure future for the people you love.