Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following all your specific requirements.

Yes, you can switch from a Medicare Advantage plan to a Medigap policy. But the real question isn't if you can—it's when and how. Your ability to make the change comes down to specific enrollment periods and whether you have a "guaranteed issue right," which lets you buy a policy without getting grilled about your health history.

Understanding the Switch from Advantage to Medigap

Deciding to switch from Medicare Advantage to Medigap is a big move. It all starts with understanding how fundamentally different these two paths are. This isn’t just about the monthly premium; it’s about control, flexibility, and predictability on your healthcare journey.

Medicare Advantage (Part C) plans are your "all-in-one" option, bundling hospital, medical, and often drug coverage through private insurers. They typically rely on networks like HMOs or PPOs, which means you have to stick to their list of approved doctors and hospitals.

Medigap, on the other hand, works with Original Medicare (Parts A and B). It’s designed to fill in the financial "gaps" Medicare leaves behind, like deductibles and coinsurance. The biggest win here? Freedom. You can see any doctor or specialist in the country who accepts Medicare, no referrals needed.

Why People Consider Making a Change

Let me paint a picture for you. You've been on an Advantage plan for a few years, and everything’s been fine. Then, you're diagnosed with a condition that requires seeing a specialist regularly. But the top specialist in your area—the one everyone recommends—isn't in your plan's network.

This is a story I hear all the time. It’s one of the most common reasons people start looking at Medigap. They want the liberty to choose their own doctors without being limited by a network directory.

The numbers show just how popular both choices are. In 2025, projections suggest that over half of all beneficiaries, about 54%, will be enrolled in Medicare Advantage. At the same time, as of 2022, roughly 42% of folks on Original Medicare had a Medigap policy to go with it.

The core trade-off often comes down to this: Medicare Advantage usually has lower monthly premiums but comes with copays, deductibles, and network rules. Medigap has higher monthly premiums but gives you predictable out-of-pocket costs and total provider freedom.

To really see the full picture, it helps to understand the various senior care options available. This context helps you see where your Medicare choices fit into your bigger health and financial picture.

Our comprehensive Medicare planning guide can also give you a much deeper look into how to structure your long-term healthcare coverage. It’s a great resource for figuring out your next steps.

Medicare Advantage vs. Medigap at a Glance

To make things a bit clearer, let's break down the key differences side-by-side. Seeing them laid out like this can really highlight what matters most to you.

| Feature | Medicare Advantage (Part C) | Medigap (Medicare Supplement) |

|---|---|---|

| How It Works | Bundles Parts A, B, and usually D into one plan from a private insurer. | Works with Original Medicare (A & B) to cover out-of-pocket costs. |

| Provider Choice | Restricted to an HMO or PPO network; referrals often required. | See any doctor or hospital in the U.S. that accepts Medicare. |

| Monthly Premiums | Often low, sometimes $0. | You pay a separate monthly premium in addition to your Part B premium. |

| Out-of-Pocket Costs | You pay copays, coinsurance, and deductibles up to an annual limit. | Most out-of-pocket costs are covered, leading to predictable expenses. |

| Prescription Drugs | Usually included (MA-PD plans). | Not included. You must buy a separate Part D plan. |

| Extra Benefits | Often includes dental, vision, hearing, and gym memberships. | Does not include extra benefits. |

| Best For | Those who prefer lower premiums and don't mind network rules. | Those who want provider freedom and predictable costs. |

This table is a starting point. Your personal health needs, budget, and desire for flexibility will ultimately guide you to the right choice.

Finding Your Window to Switch Plans

When you want to switch from a Medicare Advantage plan back to Medigap, timing is everything. You can't just make a change whenever you feel like it. The whole process is built around specific, official windows of opportunity.

Knowing which one applies to you is the key to a smooth transition. If you miss your ideal window, you could face medical underwriting, and that might lead to a flat-out denial. Let's break down the main periods when you can make this important move.

The Annual Election Period (AEP)

This is the one most people have heard of. The Annual Election Period (AEP) runs from October 15th to December 7th every year. During this time, you can drop your Medicare Advantage plan and return to Original Medicare—which is the first critical step before you can even apply for a Medigap policy.

But here’s the catch: the AEP doesn't give you a guaranteed right to buy a Medigap plan. Your Medigap application will almost certainly be subject to medical underwriting. This means the insurance company will review your health history, and you could be denied coverage based on pre-existing conditions.

Medicare Advantage Open Enrollment Period (MA OEP)

Another important window is the Medicare Advantage Open Enrollment Period (MA OEP), which runs from January 1st to March 31st annually. If you’re already in an Advantage plan, this period gives you a one-time shot to make a change.

During the MA OEP, you can:

- Switch to a different Medicare Advantage plan.

- Drop your Advantage plan and return to Original Medicare.

Just like with the AEP, this period lets you leave your Advantage plan, but it does not grant you guaranteed issue rights for a Medigap policy. You’ll still have to pass medical underwriting to get approved. This is a common point of confusion, and our guide on what open enrollment means can help clear up the differences.

Your Best Opportunity: Trial Rights

The most powerful windows for switching are what we call "trial right" periods. These are special situations that give you guaranteed issue rights, meaning an insurance company must sell you a Medigap policy without asking a single health question.

Here's one of the most common trial rights in action:

- You joined a Medicare Advantage plan when you first became eligible for Medicare at 65.

- You decide within the first 12 months that it’s not the right fit for you.

In this scenario, you have a special right to leave your Advantage plan and buy any Medigap policy sold in your state. This is your "do-over" period—a golden opportunity to switch without the fear of being denied for health reasons.

While these enrollment periods are the general rule, where you live also plays a huge role. Medigap enrollment rules can vary a lot by state, with participation rates ranging from just 9% in Hawaii to 67% in Iowa back in 2023. Understanding your specific state's rules is absolutely crucial for making the right move.

How Medical Underwriting Can Derail Your Switch

When you decide it’s time to move from Medicare Advantage to Medigap, you'll run into a term that sounds pretty intimidating: medical underwriting.

Getting a handle on this process is the single most important part of making a successful switch. Why? Because outside of a few very specific situations, you don't have an automatic right to buy a Medigap policy.

Medical underwriting is just the fancy term for how insurance companies review your health history. They take a close look at your past and current health conditions to decide if they want to offer you a policy and how much it will cost. For most people trying to change plans, this is the biggest hurdle.

What Are Insurers Really Looking For?

During the application process, the insurance company will hit you with a long list of health questions. They’re trying to figure out how much of a financial risk you are to them.

If you want to get into the nitty-gritty, our guide on what underwriting in insurance really means breaks it all down.

Typically, they'll comb through your health records from the last few years, flagging conditions like:

- Cancer (within a certain timeframe, like the last 2-5 years)

- Heart attack or stroke

- Chronic Obstructive Pulmonary Disease (COPD)

- Diabetes with complications (like neuropathy or retinopathy)

- Kidney disease that requires dialysis

- Alzheimer's or dementia

- Rheumatoid arthritis

This isn't a complete list, of course, and every company plays by its own set of rules. Having one of these conditions doesn't always guarantee a denial, but it definitely makes finding coverage much more difficult.

Think of it this way: When you first signed up for Medicare at 65, you got a one-time "free pass"—your Medigap Open Enrollment Period. During that window, no underwriting was allowed. But once that window closes, you usually have to prove you're a good health risk to get approved for a policy.

For example, someone who had a heart attack two years ago would likely be turned down by most Medigap carriers. On the other hand, a person with well-managed high blood pressure might get approved, though maybe at a higher rate. It all comes down to a case-by-case evaluation.

How to Bypass Underwriting with Guaranteed Issue Rights

So, is there a way to switch from Medicare Advantage to Medigap without going through this health review? Yes, but you need what’s called a guaranteed issue right.

These are special circumstances, protected by federal law, that basically force an insurance company to sell you a Medigap policy, no questions asked about your health.

Here are a few of the most common situations that give you these rights:

- Your Advantage Plan Is Leaving Town: If your Medicare Advantage plan stops offering coverage in your county or you move out of its service area, you get a special window to buy a Medigap plan.

- You're in a "Trial Right" Period: Did you join an Advantage plan when you first turned 65? You have 12 months to switch back to Original Medicare and pick up a Medigap policy with guaranteed issue rights. It’s your one-time "do-over" window.

- Your Insurer Misled You or Broke the Rules: If you can prove that your Advantage plan provider didn't follow the rules or gave you misleading information, you might be granted a right to switch.

Knowing if you qualify for one of these protections is everything. It's the difference between a simple, guaranteed switch and a frustrating application process that could easily end in a denial letter.

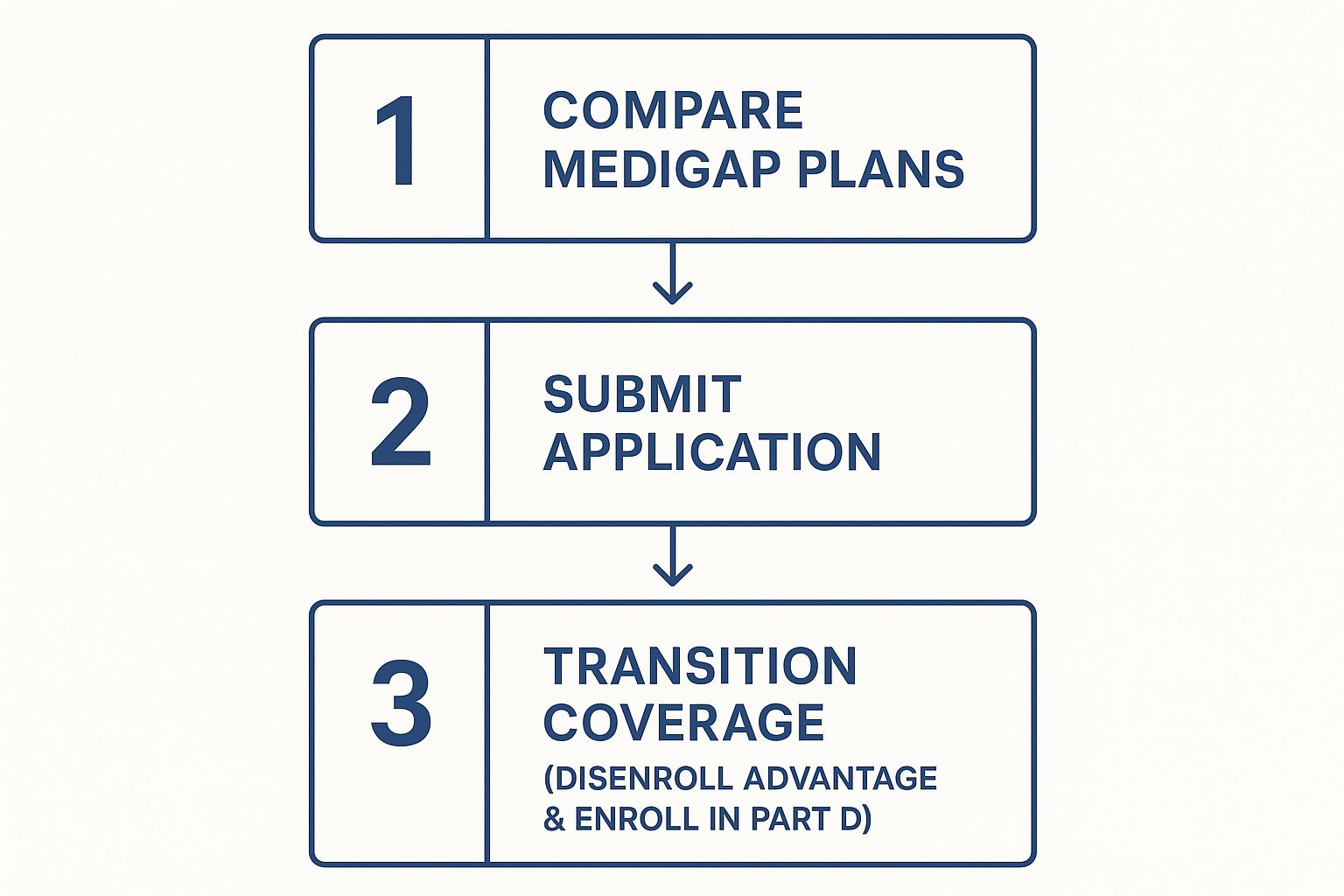

The Process for Changing Your Medicare Coverage

So, you’ve decided that switching from Medicare Advantage to Medigap is the right call. That's a big decision, and now it's time to nail down the practical steps.

The process itself isn't rocket science, but the order you do things in is absolutely critical. Getting the sequence right is the key to making sure you don't accidentally create a gap in your health coverage. Think of it as a clear path from research to enrollment.

Your first move is to dive into the Medigap policies available where you live. While Medigap plans are standardized—meaning a Plan G from one company has the same core medical benefits as a Plan G from another—the monthly premiums can be all over the map. This is why you have to shop around.

Research and Compare Medigap Plans

Start by looking at the most popular options, like Plan G and Plan N. People love Plan G because it's so comprehensive; it covers almost everything Original Medicare doesn't, other than your yearly Part B deductible. Plan N is a great alternative if you want a lower premium, but you'll have small copays for some doctor visits and ER trips.

A fantastic, unbiased place to begin your research is the official Medicare plan comparison tool.

This government site lets you plug in your zip code and see the exact Medigap plans and insurance carriers in your area. It gives you a solid, factual foundation to build on.

Once you’ve zeroed in on a plan letter you like and a few insurance companies, the next step is to apply. Remember, unless you have a "guaranteed issue right," you’ll have to go through medical underwriting. This just means the insurer will take a look at your health history before they approve you.

Crucial Tip: Do not—under any circumstances—disenroll from your Medicare Advantage plan until you have received a formal approval letter for your new Medigap policy. Canceling your old plan too soon is a common and costly mistake that can leave you completely uninsured.

Finalizing Your New Coverage

After you get that Medigap approval in hand, you have two last—but equally important—tasks to check off.

First, you need to officially disenroll from your Medicare Advantage plan. You can usually do this by calling the plan provider directly or by contacting Medicare at 1-800-MEDICARE.

Second, you absolutely must enroll in a standalone Medicare Part D plan for your prescriptions. Medigap policies don't cover drugs you pick up at the pharmacy. If you skip this step, you won't just be without drug coverage; you could also face a permanent late enrollment penalty down the road.

Following these steps in order is the only way to guarantee a smooth, seamless switch. You secure your new Medigap policy first, then you make changes to your other coverage. No gaps, no stress.

A Real-World Look at Advantage vs. Medigap Costs

When you're thinking about switching from Medicare Advantage to Medigap, you have to look past the monthly premium. It's about the whole financial picture—deductibles, copayments, and your absolute worst-case scenario.

The two plans handle money in completely different ways, and it can make a huge difference in what you spend over a year.

Medicare Advantage plans grab your attention with those low—or even $0—monthly premiums. It’s an appealing hook, but it comes with a pay-as-you-go model. You’ll be reaching for your wallet for copays every time you see a doctor, visit a specialist, or end up in the hospital.

Medigap plans, on the other hand, start with a higher, fixed monthly premium. That consistent cost buys you predictability. Once your premium and the annual Part B deductible are paid, many plans cover the rest of your approved medical bills at 100%. This structure is designed to stop the surprise bills that can pile up fast with an Advantage plan.

Putting Costs into Context

Let’s run the numbers with a real-world scenario. Imagine someone who sees a few specialists each year and has one unexpected hospital stay. How would their costs stack up?

- On a typical Medicare Advantage Plan: They might pay a $0 monthly premium. But they could also face a $45 copay for each specialist visit and a $350 daily copay for the first five days in the hospital.

- On a Medigap Plan G: They would pay a higher monthly premium but then have $0 for all specialist visits and hospital stays after meeting their one-time annual Part B deductible.

For someone with even moderate health needs, that higher Medigap premium can quickly become the more cost-effective choice. It offers peace of mind and makes budgeting a whole lot easier. This is a crucial point to understand when comparing Medicare vs. private insurance options.

To make this even clearer, let's break down a hypothetical year for a beneficiary who has a few doctor visits, sees a specialist, and has a short hospital stay.

Sample Annual Cost Breakdown

| Cost Component | Medicare Advantage Plan Example | Medigap Plan G + Part D Example |

|---|---|---|

| Monthly Premium | $0/month ($0/year) | Medigap: $180/mo, Part D: $35/mo ($2,580/year) |

| Annual Deductible | $0 (Part B deductible applies) | Part B Deductible: $240 |

| Specialist Visits (4) | $45 copay each ($180 total) | $0 after deductible |

| Hospital Stay (3 days) | $350/day copay ($1,050 total) | $0 after deductible |

| Prescription Plan | Included ($30/month copays) | Separate Part D Plan (included in premium above) |

| Total Annual Cost | $1,230 + Part B Premium | $2,820 + Part B Premium |

At first glance, the Advantage plan looks cheaper. But what if that hospital stay was longer, or you needed more frequent specialist care? The Advantage costs would climb, while the Medigap costs would remain fixed. It's all about balancing predictable premiums against unpredictable usage-based fees.

The Out-of-Pocket Maximum Safety Net

One of the biggest differences is the maximum out-of-pocket (MOOP) limit. Every Medicare Advantage plan has one, and it's meant to act as a financial safety net.

But that "safety net" can be set pretty high. In 2025, the maximum limit for in-network services on an Advantage plan is $9,350. That means in a year with serious health problems, you could be on the hook for thousands of dollars before your plan starts covering everything at 100%.

Medigap plans, especially comprehensive ones like Plan G, offer much stronger protection against catastrophic costs right from the start.

The core financial question is this: Do you prefer paying less upfront with the risk of unpredictable, higher costs when you need care, or paying a higher fixed premium for near-total cost certainty?

While Medigap premiums are higher—the average was around $217 a month in 2023—they often lead to lower total spending for people who use their medical benefits regularly.

Don't forget the extras, though. Advantage plans often bundle in dental, vision, and hearing benefits, which can be valuable. With Medigap, you'll also need a separate Part D plan for your prescriptions, which adds another monthly cost. You have to weigh the rock-solid predictability of Medigap against the bundled convenience of an Advantage plan to find what truly fits your life.

A Few Common Questions We Hear All the Time

"Will I Lose My Prescription Drug Coverage if I Switch to Medigap?"

Yes, you will—at least, the coverage that was bundled into your Medicare Advantage plan. Medigap policies are built to cover your medical bills, not your prescriptions.

So, what do you do? You’ll need to enroll in a standalone Medicare Part D plan. The timing here is absolutely critical. You want to avoid any gaps in coverage and definitely don't want to get hit with a late enrollment penalty.

To make sure you keep your drug coverage without a hitch:

- Sign up for your new Part D plan before your Medicare Advantage plan officially ends.

- Carefully compare the formularies of different Part D plans. A formulary is just the list of drugs a plan covers. You need to make sure your specific medications are on it.

- Mark down all the important dates on your calendar. Missing an enrollment window can cause big headaches later.

Remember, one of the trade-offs with Medicare Advantage is that you're often locked into their specific drug formulary. Moving to Medigap gives you the freedom to choose a Part D plan that actually fits the prescriptions you take.

Part D premiums can run anywhere from $10 to $110 a month, and the annual deductible can be as high as $590 in 2025. It’s a new expense to budget for, but it’s a necessary one.

And a pro tip: review your Part D plan every single year. Premiums and formularies change, so what worked this year might not be the best fit next year.

Tools like the official Medicare Plan Finder or a broker's quoting tool can make comparing your options a whole lot simpler.

"Can an Insurance Company Just Deny Me a Medigap Policy?"

This is a big one. The answer is: it depends on your timing.

If you’re outside of your initial Medigap open enrollment period or a special “guaranteed issue” window, then yes, an insurance company can use medical underwriting.

This means they’ll dig into your health history. Based on what they find—like pre-existing conditions—they can legally deny you coverage or charge you a much higher premium. Knowing your state’s rules on this can save you from a nasty surprise.

Think of guaranteed issue rights as your golden ticket. They let you switch from Medicare Advantage to Medigap without answering a single health question.

So, what triggers these rights? A few common situations include:

- Your Medicare Advantage plan decides to stop serving your area.

- You move out of your plan’s service area.

- You use your 12-month "trial right." This applies if you tried a Medicare Advantage plan for the first time when you turned 65 and want to switch to Medigap within the first year.

If you don’t qualify for one of these protected windows, the insurance company’s underwriters get the final say on whether you get a policy and how much you’ll pay for it.

"What if I Switch to Medigap and Don't Like It? Can I Go Back?"

You usually can. If you decide Medigap isn't for you, you can typically switch back to a Medicare Advantage plan during the Annual Election Period, which runs from October 15th to December 7th each year.

The key is to do it in the right order. Apply for the Medicare Advantage plan first. Only after you’ve been approved and have your new coverage locked in should you cancel your Medigap policy. This prevents any accidental gaps where you're left uninsured.

Just be aware, this can be a one-way street. If you go back to Medicare Advantage and later want to try Medigap again, you’ll likely face medical underwriting all over again.

Here’s a quick recap to make your switch as smooth as possible:

- Always, always, always get approved for your Medigap policy before you drop your Medicare Advantage plan.

- Line up your new Part D plan at the same time so your prescription coverage never lapses.

- Track every deadline. This ensures you have continuous benefits without any stressful gaps.

Once you understand these steps, you’ll be able to answer the question, “Can I switch from Medicare Advantage to Medigap?” with complete confidence.

Ready to find the right plan? Get a personalized quote from My Policy Quote.