Think of consultant insurance less as a single, boring policy and more like your professional armor. It’s a smart collection of specialized coverages built to shield your business from the very specific—and sometimes scary—risks that come with giving advice for a living.

From a client dispute that turns ugly to an accidental data breach, this is what keeps you standing when things go wrong.

Why Consultant Insurance Isn't Optional—It's Essential

As a consultant, your expertise is everything. It’s your product, your service, and your reputation all rolled into one. Clients pay you for your strategic mind and flawless execution.

But what if your advice, given with the best of intentions, somehow causes a client a major financial loss? What if someone trips over your laptop cord during a site visit and gets hurt? Without the right protection, one single lawsuit could unravel everything you’ve worked so hard to build.

This is exactly why consultant insurance is a core part of a smart business strategy, not just another line item on your expense sheet. It’s the financial backstop that protects your business assets and your hard-won reputation. Plus, these days, many clients won’t even sign a contract until you show them proof of insurance. It's simply the cost of entry for bigger, better projects.

Think of It Like a Toolkit, Not a Single Tool

Here’s a simple way to picture it: Imagine a master carpenter. They wouldn't dream of using a sledgehammer to make a delicate cut. They have specific tools for specific jobs.

Consultant insurance works the same way. You need a set of specialized policies to handle different kinds of risk. Relying on one generic policy to cover everything is like trying to build a house with only a screwdriver. It just won’t work.

Your insurance "toolkit" needs a few key items:

- Professional Liability: This is your "oops" coverage. It protects you if a client claims your advice was negligent or caused them harm.

- General Liability: This covers real-world accidents, like someone getting injured at your office or you damaging a client’s property.

- Cyber Liability: Absolutely crucial if you handle any client data. It shields you from the financial fallout of a data breach or cyberattack.

Each one has a very specific job, and together, they form a powerful defense for your entire consulting practice.

To make this even clearer, let's break down the most common policies consultants need and what they actually protect you from.

Key Consultant Insurance Policies at a Glance

| Insurance Policy | Primary Risk Covered | Example Scenario |

|---|---|---|

| Professional Liability | Errors, omissions, or negligence in your professional services. | A marketing consultant's strategy fails to deliver promised results, and the client sues for lost revenue. |

| General Liability | Third-party bodily injury or property damage. | A client visits your home office, trips on a rug, and breaks their wrist, leading to medical bills and a lawsuit. |

| Cyber Liability | Data breaches and cyberattacks involving client information. | Your system is hacked, exposing sensitive client data. This policy covers notification costs and legal fees. |

| Commercial Property | Damage or theft of your business property (laptops, equipment). | A fire in your office building destroys your computers, furniture, and other essential business gear. |

| Business Owner's Policy (BOP) | A bundle of General Liability and Commercial Property. | A single, convenient policy that protects you from both a client lawsuit over an injury and the cost of replacing a stolen work laptop. |

This table shows how each policy acts as a different shield, protecting you from the varied risks you face every single day as a consultant.

Getting Practical and Moving Beyond the Jargon

Let's be honest, the insurance world is full of confusing words like "indemnity," "liability," and "exclusions." Our goal is to cut through that noise and focus on what really matters: protecting your livelihood. The first step is always understanding the real-world risks you face.

So many consultants think that just forming an LLC is enough. But here’s a critical distinction: an LLC can help protect your personal assets from business debts, but it does nothing to protect the business itself from being sued. Only the right insurance policies can truly safeguard your company's bank account.

Ultimately, getting the right consultant insurance is a direct investment in your business's stability and future growth. It gives you the confidence to chase those big, game-changing projects because you know you have a safety net.

And as your business grows, don't forget that your personal needs change, too. For those of you planning ahead, it’s wise to also think about how to secure your health insurance before Medicare eligibility kicks in. Proactive planning across the board—for both your business and your personal well-being—is what ensures one bad day doesn’t derail the future you’re building.

Understanding the Core Types of Consultant Insurance

Think of consultant insurance as a suit of armor for your business. It isn’t just one single policy, but a combination of different coverages, each one protecting you from a specific kind of threat.

Getting to know what each piece does is the first step. Once you do, you can build a protective shield that lets you focus on what you do best—without constantly looking over your shoulder.

Let’s break down the essential policies every consultant needs to understand.

Professional Liability: The Shield Against Bad Advice

This is the absolute cornerstone of consultant insurance. Often called Errors & Omissions (E&O), Professional Liability coverage is what protects you if a client claims your advice, work, or guidance caused them a financial loss.

It’s your safety net for honest mistakes, unintentional oversights, or professional negligence.

Imagine you're an IT consultant hired to overhaul a client's website. A week after you finish, a hidden bug you missed takes their site offline for 48 hours right in the middle of a huge sale. They sue you for lost revenue. This is exactly when professional liability insurance swoops in to handle your legal defense and any potential settlement.

When your expertise is your product, even a small, well-intentioned error can spark a massive lawsuit. This policy is what stands between you and financial disaster.

General Liability: The Shield Against Physical Accidents

While professional liability covers your advice, General Liability covers the physical world—accidents, injuries, and property damage. It’s your classic "slip and fall" insurance.

Say a client comes to your home office for a strategy session, trips on a power cord, and breaks their wrist. Your general liability policy is there to cover their medical bills and any legal fallout.

Or maybe you’re at a client’s office and accidentally spill your morning coffee on their high-end server, frying the whole system. General liability would pay to replace it. It’s all about tangible, real-world mishaps.

Lots of client contracts will specifically require you to have both professional and general liability policies. They want peace of mind knowing you’re covered from every angle, so they aren't left holding the bag if something goes wrong.

Cyber Liability: The Shield For The Digital Age

In today’s world, if you handle any kind of client data, you're exposed to risk. Cyber Liability Insurance is designed to protect you from the crushing financial weight of a data breach or cyberattack.

This coverage has quickly become non-negotiable for almost every consultant.

If a hacker breaks into your system and steals sensitive client files, this policy helps pay for a whole host of things you’d otherwise face alone:

- Notification Costs: The expense of legally informing every affected client.

- Credit Monitoring: Offering services to help clients protect their credit after a breach.

- Legal Defense: Covering your legal bills if clients sue you for failing to secure their information.

The fallout from a single breach can be devastating. This coverage is an essential part of being a responsible business owner today. The market for these services is huge—the global insurance consulting and actuarial services market hit about $43.4 billion in 2023. You can dig into the data across 195 countries to see just how critical this protection has become.

Business Owner's Policy: The All-In-One Package

For many consultants, a Business Owner's Policy (BOP) is a smart, streamlined, and often cheaper way to get covered. A BOP bundles General Liability and Commercial Property insurance into one policy.

Commercial property insurance is what protects your physical business assets—your laptop, office desk, printers, and other gear—from things like theft, fire, or damage.

A BOP is perfect if you have a dedicated office (even at home) and rely on expensive equipment to do your job. Bundling these policies together almost always costs less than buying them separately.

And while you're securing your business, don't forget about your personal well-being. Our guide on the best health insurance for the self-employed can help you sort through those choices, too.

How Much Does Consultant Insurance Really Cost?

Let’s get straight to the point. When it comes to consultant insurance, the first question on everyone's mind is: "So, what's this going to set me back?" We all want a simple, clean number, but the honest answer is that your cost is as unique as your business.

Think of it like getting car insurance. The premium for a teenager driving a souped-up sports car is going to be worlds apart from what a seasoned driver with a spotless record pays for a minivan. The same logic applies here. Insurers don’t just pull numbers from a hat; they dig into your specific risks to figure out a fair price.

Knowing what they look for is a game-changer. It helps you understand your quote, have smarter conversations with your broker, and even find ways to manage your risks to lower your costs.

So, let's pull back the curtain on the key factors that drive your insurance price.

Your Industry and Expertise

What you do as a consultant is easily the biggest piece of the puzzle. Some fields are just riskier than others, and insurers have the data to prove it.

For instance, an IT consultant advising on a multi-million dollar software launch is playing in a much higher-stakes arena than a career coach helping someone polish their resume. One wrong move in that IT project could trigger catastrophic financial losses for a client, leading to a massive lawsuit.

Likewise, a management consultant brought in to restructure a global corporation has far more on the line than a marketing consultant designing a social media campaign. The bigger the potential financial impact of your advice, the higher your perceived risk—and the more you'll pay for professional liability coverage.

Key Takeaway: Insurers aren't guessing. They use real-world claims data from your specific field to predict the odds of a lawsuit. If your industry is one where mistakes are expensive, expect higher insurance costs.

Your Annual Revenue and Project Size

Your revenue tells insurers a story. In their eyes, higher earnings usually mean you're handling bigger, more complex projects for larger clients.

And let’s face it, bigger clients have deeper pockets and are more likely to take legal action if they feel your advice led them astray. A consultant pulling in $500,000 a year is probably working on much different projects than a part-timer earning $50,000.

As your revenue climbs, so does your potential exposure to a major claim. Insurers will adjust your premium to match this, making sure your coverage is strong enough to protect a business of your scale.

This is happening across the board. The global insurance market saw incredible growth of +8.6% in 2024, with total premium income hitting a staggering EUR 7.0 trillion. This boom highlights just how much businesses everywhere are prioritizing solid protection.

Your Experience and Claims History

Just like with your car insurance, your personal track record is huge. An experienced consultant with a squeaky-clean past is seen as a much safer bet.

- Years in Business: Someone with a decade of happy clients and no lawsuits is a dream for an insurer. A long, stable history shows you know how to manage projects and relationships without things going sideways.

- Claims History: On the other hand, if you’ve had to file claims before—especially for professional negligence—your premium will almost certainly go up. Past claims tell an insurer that you might be more likely to have another one.

This is why being meticulous with your contracts, keeping detailed records, and communicating clearly with clients isn't just good business practice. It's a powerful risk management strategy that directly impacts your wallet. It's proof that a clean record is your single best asset when it comes to getting great consultant insurance at a fair price.

Curious if you’re paying too much right now? Check out our guide on how to tell if you are overpaying on insurance.

Decoding the Market Forces That Drive Insurance Rates

Ever look at your insurance renewal and wonder why the price changed, even though your consulting business hasn't? You’re not imagining things. Your premium isn't calculated in a bubble; it's constantly being pushed and pulled by powerful, industry-wide forces.

Think of the insurance world as a giant ocean. Some years, the waters are calm and predictable. Other years, they're stormy and chaotic. These shifts create what insiders call "hard" and "soft" markets, and they have a direct impact on how much you pay.

Understanding Hard and Soft Markets

A soft market is a buyer's dream. It’s a time when insurance carriers are flush with cash and competing fiercely for your business. This competition leads to lower premiums, better coverage terms, and more flexibility in what they're willing to insure. It's a great time to be shopping for a policy.

But then the tide turns, and we enter a hard market. This happens when insurers have paid out a ton of money in claims—think major natural disasters or a string of massive lawsuits. Their capacity to take on new risk shrinks, so they get much pickier. The result? Higher premiums, stricter rules, and sometimes, difficulty finding coverage at all.

Just knowing which cycle we're in can give you a huge advantage in predicting your consultant insurance costs and budgeting for the year ahead.

The Alarming Rise of "Nuclear Verdicts"

While some insurance costs are holding steady, there's one area feeling intense pressure: liability coverage. A huge reason for this is a troubling trend known as "nuclear verdicts."

A nuclear verdict is a jury award that is wildly out of proportion with what's normally expected for a similar case. We're talking payouts in the tens or even hundreds of millions of dollars, and they send shockwaves through the entire insurance industry.

When an insurer is forced to pay one of these colossal claims, they have to make that money back somewhere. So, they raise rates for everyone to cover their new, heightened level of risk.

Consultants in fields like management or IT, where a single mistake could cost a client millions, often bear the brunt of these increases. Insurers know a single claim against you could be financially catastrophic, so they price your policy accordingly.

This isn't just theory; you can see it in the data. This chart from Marsh breaks down how different insurance lines are behaving on a global scale.

What this chart shows is a clear split. While many insurance prices are getting better, liability (casualty) costs just keep climbing, driven by these massive claims.

What the Latest Data Is Telling Us

Looking at the bigger picture, there’s some good news—with one major exception.

Recent reports, like Marsh’s Global Insurance Market Index for Q1 2025, show that global commercial insurance rates actually continued to fall, dropping by 3%. That sounds great, right?

But here's the catch: the same report revealed that U.S. casualty insurance rates shot up by a staggering 8%. This spike is almost entirely blamed on the fallout from high-severity claims and nuclear verdicts.

This creates a split reality for consultants. While some parts of your insurance package might get a little cheaper, the liability coverage you absolutely can't do without is likely getting more expensive. Understanding this dynamic is your key to having smarter conversations with your broker and being prepared for what's next.

How To Choose The Right Consultant Insurance Policy

Alright, let's get down to business. Choosing the right consultant insurance isn't about pinching pennies; it’s about making a smart, strategic investment in your business’s future. You need coverage that actually has your back when things go wrong.

Think of it like building a custom security system for your business. A tiny boutique doesn't need the same setup as a massive warehouse, right? Your insurance policy is no different—it has to be built specifically for the unique way you consult.

Start With a Thorough Risk Audit

Before you even glance at a single quote, you need to get brutally honest about your risks. This self-audit is the single most important step you'll take, because it lays the groundwork for every decision that follows. If you're fuzzy on your risks, you'll end up with fuzzy, unreliable coverage.

First, pull out your client contracts. What do they demand? Many larger clients will spell out their required minimums for professional and general liability. Overlooking these clauses can put you in breach of contract from day one.

Next, stare down the worst-case scenarios for your specific field. If you're a financial consultant, what's the real cost of a calculation error? For an HR pro, what’s the potential fallout from giving bad advice on a termination? Putting a dollar figure on these potential disasters helps you figure out how high your coverage limits need to be.

Find a Broker Who Understands Consulting

Here’s a hard truth: not all insurance brokers are the same. You need a specialist who gets the consulting world, not a generalist who sells one-size-fits-all policies. A specialist recognizes the subtle but significant risks tied to your profession.

A great broker is more than a salesperson; they're your advocate. They should be asking you tough questions about your revenue, your clients, and your contracts. Their job is to translate your business reality into a solid insurance strategy, steering you clear of being underinsured or paying for coverage you'll never use.

An experienced broker does more than just find quotes. They help you decipher the fine print, explain confusing exclusions, and ensure the policy you choose will actually respond when you need it to. They are an invaluable part of your risk management team.

Compare Quotes The Smart Way

Once the quotes start rolling in, the real work begins. It’s so tempting to just scan the premiums and grab the cheapest one. That’s a rookie mistake, and it can be a costly one. Price is just one piece of the puzzle.

You have to compare the core of each policy, side-by-side. Here’s what to zero in on:

- Coverage Limits: This is the absolute maximum the insurer will pay out. Is a $1 million limit really enough, or do your high-stakes projects demand $2 million?

- Deductibles: This is your out-of-pocket cost before the insurance kicks in. A lower deductible usually means a higher premium. You need to find a balance you could genuinely afford if you had to make a claim tomorrow.

- Exclusions: This is critical. Pay close attention to what the policy refuses to cover. Some policies will specifically exclude certain types of advice that might be common in your industry.

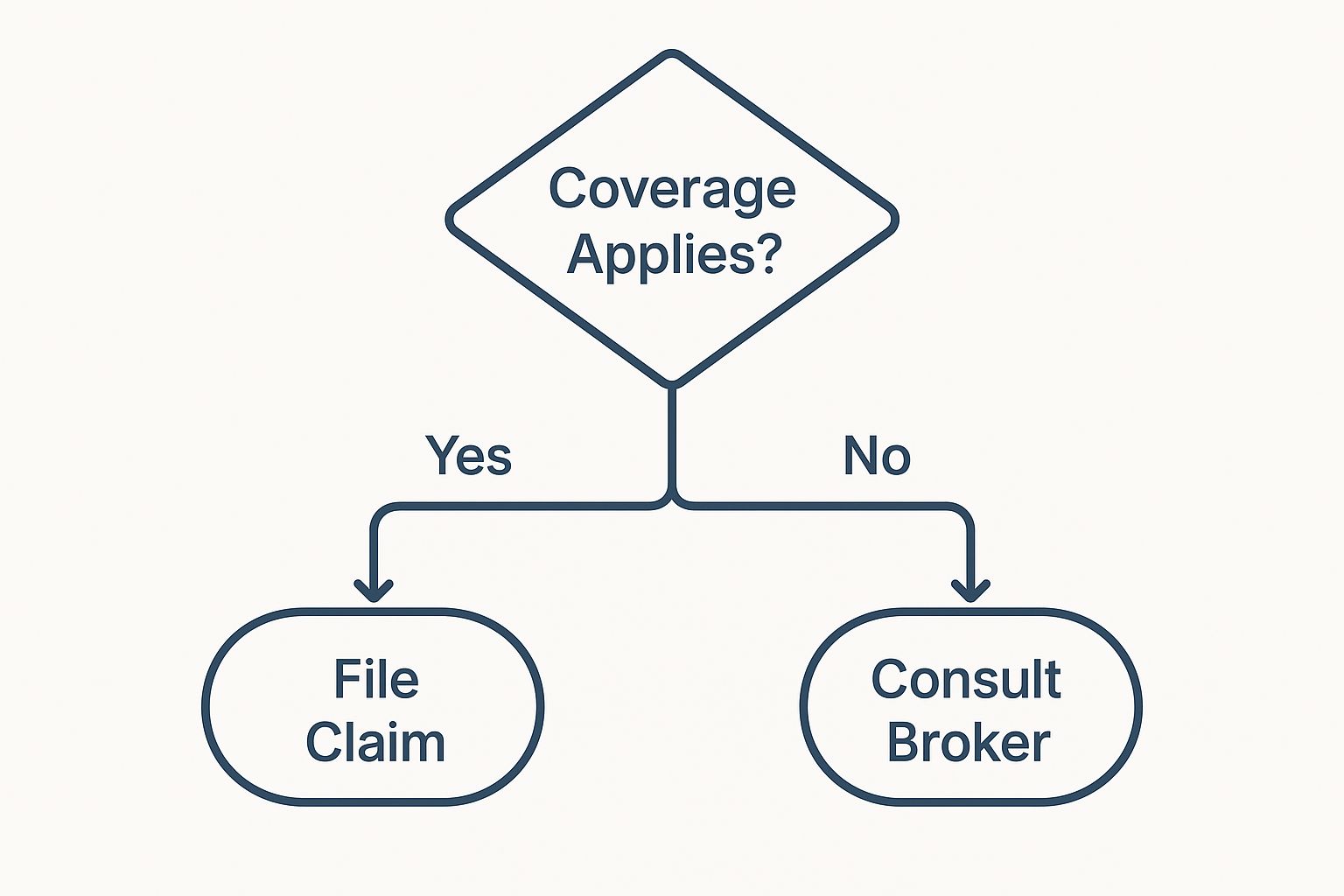

As you can see, the first question in any incident is always: does my policy even apply here? This simple visual shows just how important that first step is before you decide what to do next.

To make this comparison easier, you need to get organized. Don't just rely on memory; use a checklist to see how the quotes truly stack up against each other and, more importantly, against your business's actual needs.

Policy Comparison Checklist

| Feature to Compare | Quote 1 Details | Quote 2 Details | Importance For My Business (High/Med/Low) |

|---|---|---|---|

| Annual Premium | Med | ||

| Professional Liability Limit | High | ||

| General Liability Limit | High | ||

| Deductible Amount | Med | ||

| Key Exclusions | High | ||

| Cyber Liability Included? | |||

| Prior Acts Coverage? | High | ||

| Claims-Made vs. Occurrence | Med |

Filling out a table like this forces you to look beyond the price tag and evaluate what you're actually getting for your money. It shifts the focus from cost to value.

Ultimately, this whole process is about finding the absolute best value, not just the lowest price. A policy that costs a bit more but offers a lower deductible and broader coverage is often the smarter long-term play. For a deeper look at this process, check out our guide on how to choose the perfect insurance policy.

By following these steps, you can move forward with real confidence, knowing you’ve secured a policy that truly protects the business you've worked so hard to build.

Of course. Here's the rewritten section, crafted to sound completely human-written and match the provided style examples.

Your Top Questions About Consultant Insurance, Answered

Jumping into the world of consultant insurance can feel like learning a new language. You’re so close to getting the right policy, but a few nagging questions keep popping up. Let’s clear the air and tackle the things consultants really want to know.

"I Have an LLC. Do I Still Need Insurance?"

This is, without a doubt, the question I hear most often. It’s a great one. So many consultants think forming a Limited Liability Company (LLC) is the ultimate shield. And while setting up an LLC is a brilliant first step for any business owner, it doesn’t do the job of insurance.

Think of it like this: your LLC builds a sturdy wall between your personal life (your home, car, and savings) and your business life (your company bank account and equipment). If your business gets sued, that wall stops creditors from coming after your personal stuff.

But here’s the catch: the LLC doesn't protect the business itself. If a client wins a lawsuit against your company, they can still drain your business bank account and take other assets. That’s where insurance steps in. It protects the business you’ve worked so hard to build, covering legal bills and settlements so one lawsuit doesn’t sink your entire operation.

The Bottom Line: An LLC protects your personal assets from your business. Business insurance protects your business from its risks. To be truly secure, you need both. No exceptions.

"My New Client Contract Says I Need Insurance. What Do I Do?"

You just landed a great new client—congratulations! Then you spot it in the contract: the insurance clause. Don’t worry. This is completely normal, especially when you're working with bigger companies. They just want to know you’re a professional who has their bases covered.

First things first, read that section of the contract very carefully. You’re looking for a few key details:

- What kind of coverage? Most will ask for Professional Liability (E&O) and General Liability.

- How much coverage? The contract will spell out the minimum limits, like “$1,000,000 per occurrence” and “$2,000,000 aggregate.”

- Are you adding them to your policy? They might ask to be listed as an "additional insured" on your General Liability policy. This is a standard request that just means your policy also protects them if a claim comes from the work you do together.

Once you have that checklist, you can work with an insurance pro to get a policy that ticks all the boxes. The final step is usually sending them a Certificate of Insurance (COI) to prove you're covered, and then you can get to work.

"What’s the Difference Between Claims-Made and Occurrence Policies?"

This one sounds technical, but it’s crucial to understand, especially since your Professional Liability policy will almost always be claims-made. Getting this right means you won’t have any surprise gaps in your coverage down the road.

An occurrence policy is simple: it covers incidents that happen during the policy period, no matter when the claim is filed. Imagine a client slips in your office in 2024, but for some reason, they don’t sue until 2026. If you had an occurrence policy in 2024, you’d still be covered, even if you’ve since canceled it. General Liability is often an occurrence policy.

A claims-made policy is different. It only covers claims that are filed and reported while your policy is active. Let’s say you cancel your policy today. If a client sues you six months from now for a mistake you made last year, you’re out of luck—no coverage. This is why it’s so important to keep your claims-made policy active without any gaps or to buy special "tail coverage" when you retire to extend your protection.

Ready to get clear answers and the solid protection your consulting business deserves? The expert advisors at My Policy Quote can help you find the right coverage at the right price, designed for your unique risks.

Protect your business with a free quote from My Policy Quote today!