Let's be honest, health insurance can feel confusing and rigid. But what if there was a way to get the coverage you actually need, on your own terms, with your employer’s help?

Enter the Individual Coverage Health Reimbursement Arrangement (ICHRA).

Forget the one-size-fits-all group plan. Think of an ICHRA as a tax-free allowance from your employer, specifically for your health insurance. Your company sets aside funds for you, and you get to go out and shop for a health plan that fits your life.

A Modern Twist on Health Insurance

The ICHRA completely flips the old model of employee benefits. It shifts the power from the employer choosing a single, often restrictive plan, to a model of defined contribution.

Here’s what that means: Instead of defining the plan for everyone, your employer defines the contribution—the specific dollar amount they’ll reimburse you for health insurance costs.

This puts you squarely in the driver's seat. You can pick a health plan from the individual market that truly works for you. Need a specific network of doctors? A lower deductible? More robust coverage for your family? You get to choose. It’s a system built for real life, a world away from the take-it-or-leave-it group plans of the past.

Why is Everyone Talking About ICHRA?

The buzz around ICHRAs isn't just hype. It’s a direct response to the frustrations of the traditional insurance market.

Launched back in 2020, ICHRAs took off because businesses and their teams were desperate for better options. With the average annual premium for employer-sponsored family coverage hitting a staggering $26,993, companies needed a smarter, more predictable way to manage costs. The ICHRA gave them exactly that, all while empowering their employees with real choice.

This setup is a specific type of Health Reimbursement Arrangement (HRA), which is just a formal name for an employer-funded health benefit plan. If you want to dive deeper, you can learn more about the different types of HRAs available and see how they stack up. At its heart, though, an ICHRA is designed to do one thing really well: reimburse you for your individual health insurance premiums.

The big idea is refreshingly simple: employers provide the funds, and employees choose the plan. This disconnects your health insurance from your specific job, giving you the freedom to take your coverage with you and control your own healthcare journey.

The Key Players and Pieces

To really get how an ICHRA works, it helps to see how the pieces fit together. It’s a straightforward partnership between you and your employer.

- Your Employer’s Part: The company decides on a monthly allowance for you and your colleagues. This money is offered completely tax-free.

- Your Part: You go out and buy a qualifying individual health insurance plan that meets your needs, often right from the ACA Marketplace or a private exchange.

- Getting Reimbursed: Once you show proof that you’ve paid for your plan, your employer reimburses you up to your allowance limit. Simple as that.

This table breaks it down even further.

ICHRA at a Glance Key Components

| Component | Role or Function | Key Takeaway |

|---|---|---|

| Employer Allowance | The employer sets a fixed, tax-free monthly amount for each employee. | Predictable costs for the business, clear budget for the employee. |

| Individual Plan | The employee selects and purchases their own health insurance policy. | Puts the employee in control of their coverage, network, and costs. |

| Reimbursement | The employee submits proof of payment, and the employer reimburses them. | A simple, tax-free way to fund the employee's chosen plan. |

Everyone wins. Employers get predictable, manageable costs, and employees finally get the freedom to pick a health plan that truly fits their personal health and financial situation. It’s a smarter, more human way to handle healthcare.

How an ICHRA Works From Start to Finish

Reading a definition is one thing, but seeing how an ICHRA actually works is another. Let’s leave the jargon behind and follow the journey of Sarah, a small business owner, and her new employee, Tom. This simple story shows how an ICHRA moves from an abstract idea to a real-world, flexible health benefit.

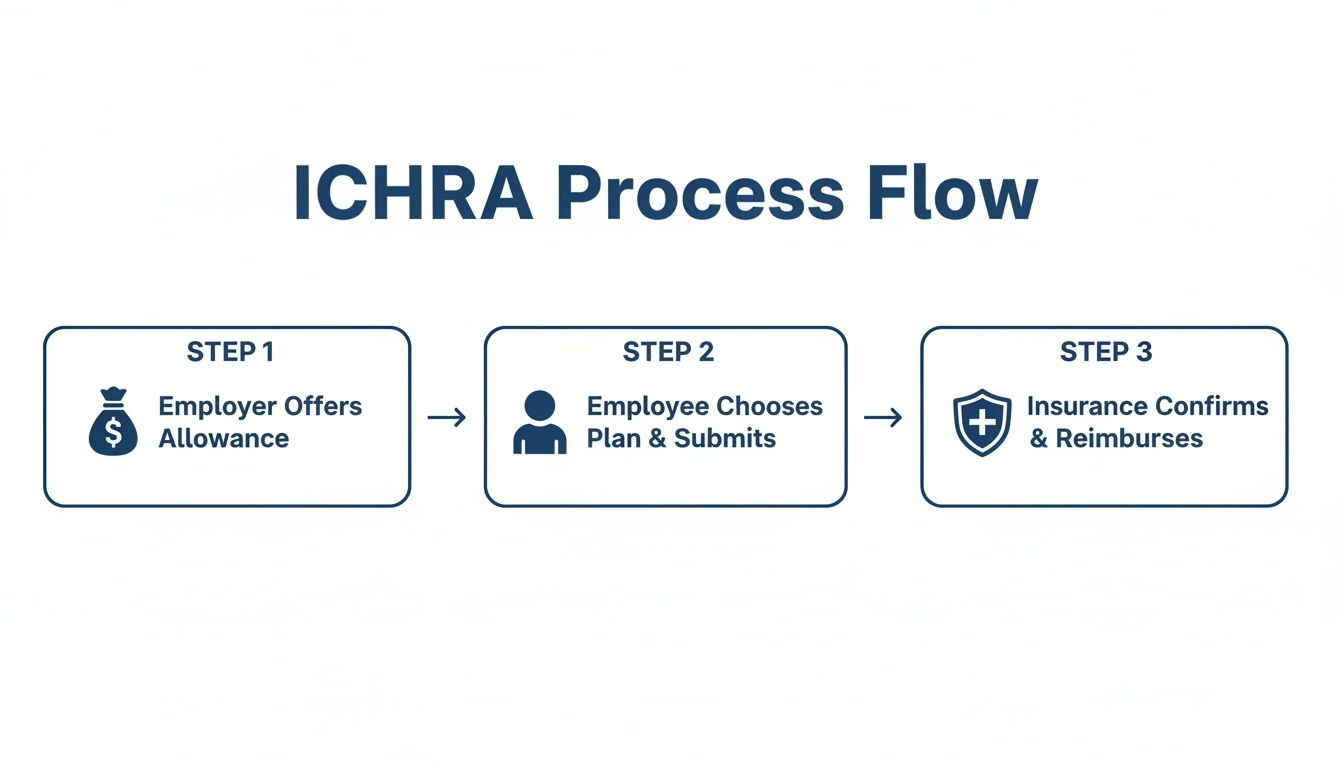

The entire process is built on choice. The employer sets the budget, and the employee picks the plan that works for them. It’s that straightforward.

This visual sums it up perfectly. The employer provides the funds, the employee chooses their insurance, and the system handles the tax-free reimbursement.

Stage 1: The Employer Sets the Allowance

It all starts with Sarah. She runs a growing consulting firm and is tired of the rigid, expensive group health plans. Instead, she decides to offer an ICHRA.

After looking at her budget, Sarah decides on a monthly allowance that’s both competitive and predictable. For example, she offers $500 per month for single employees and $1,100 per month for those with families. Just like that, her health benefit costs are fixed, with no surprise rate hikes next year.

Stage 2: The Employee Receives the Offer

Next, Tom joins the team. During his onboarding, he gets a formal notice explaining the ICHRA. The document clearly states his $500 monthly allowance and lets him know these funds are available for any qualifying individual health plan he chooses.

This isn’t just a piece of paper. It’s his ticket to shop for coverage that actually fits his life, using his employer’s contribution.

An ICHRA shifts the employer's role from being a plan administrator to a benefits facilitator. They provide a meaningful health benefit without making the healthcare decisions for their employees.

This offer is also a big deal because it qualifies Tom for a special enrollment period (SEP). This means he can shop for a plan on the marketplace right away, without having to wait for the annual Open Enrollment window.

Stage 3: The Employee Shops for a Plan

Now, the control is in Tom's hands. He takes his $500 monthly allowance to the Health Insurance Marketplace. Instead of being stuck with one or two pre-selected company plans, he can browse every single option from multiple insurance carriers.

He finds three plans that catch his eye:

- Plan A: A basic, high-deductible plan for $450/month. This would cover his premium and leave him with $50 extra.

- Plan B: A balanced plan with better copays for $520/month. He’d use his full allowance and pay the remaining $20 himself.

- Plan C: A premium plan with a huge network for $600/month, meaning he’d need to contribute an extra $100.

After thinking about his needs, Tom picks Plan B. It’s the perfect middle ground for him—a decision he made for himself, not one that was made for the entire company.

Stage 4: The Reimbursement Is Processed

The final piece of the puzzle is getting reimbursed. Each month, Tom pays his $520 premium directly to his insurance company.

Then, he submits proof of payment—like a receipt or bank statement—to Sarah's ICHRA administrator. Once the expense is verified, Tom gets his $500 reimbursement, completely tax-free. It might show up in his paycheck or as a separate direct deposit.

This simple cycle repeats every month. Sarah enjoys predictable costs, and Tom has a health plan he personally chose, paid for with tax-free dollars from his job. That’s the power of an ICHRA.

ICHRA vs. Traditional Group Plans: What's the Real Difference?

Choosing between an Individual Coverage HRA (ICHRA) and a traditional group health plan feels like picking between two totally different worlds for employee benefits. They both get you to the same destination—health coverage—but the journey, flexibility, and who’s in the driver’s seat are worlds apart.

At its heart, the debate comes down to one simple idea: control.

Traditional group plans put the employer and the insurance company in charge. They pick a few plans, and everyone has to fit into one of those boxes. An ICHRA flips that script completely. It hands the control back to the employee, turning a rigid, one-size-fits-all benefit into a flexible health allowance.

This single change has a massive impact on everything from your budget to how happy your team is with their coverage. Let's break down how these two models really stack up.

Cost Control and Predictability

For any business owner, the biggest headache with old-school group plans is the wild unpredictability of costs. Premiums can jump by double digits every single year, turning your budget into a guessing game. One year you’re hit with a 15% rate hike, and you’re stuck—either you eat the cost, reduce benefits, or ask your employees to pay more.

An ICHRA gets rid of that nightmare. You decide on a fixed monthly allowance for your team, and that’s it. Your costs become 100% predictable for the entire year. No more shocking renewal letters, just stable, manageable finances.

Employee Choice and Flexibility

This is where the difference becomes personal for your employees. With a group plan, they might get two or three options, and chances are, none of them are a perfect fit. Maybe their trusted family doctor isn't in the network, or the deductible is way too high for their budget. They're forced to compromise.

An ICHRA opens up the entire individual insurance marketplace. It’s like giving your employees a catalog of hundreds of plans to choose from. They can finally pick a plan from any insurance carrier that truly works for them.

- Their Doctor, Their Network: They can choose a plan that includes the doctors and hospitals they already know and trust.

- Their Budget, Their Rules: They can pick a high-deductible plan to keep premiums low or a plan with lower out-of-pocket costs for more peace of mind.

- The Coverage They Actually Need: They can find a plan with great prescription drug benefits or one that focuses on mental health services.

It shifts the conversation from, "Which of these few options is the least bad for me?" to "Which of these hundreds of options is the absolute best for my family?" That level of personalization is something a traditional group plan can never offer.

To give you a clearer picture, here’s a simple side-by-side look at how these two approaches compare on the features that matter most to both employers and their teams.

ICHRA vs. Traditional Group Health Plans

| Feature | ICHRA (Individual Coverage HRA) | Traditional Group Plan |

|---|---|---|

| Budget Control | 100% predictable. Employer sets a fixed allowance. | Volatile. Subject to annual rate hikes and market changes. |

| Plan Choice | Unlimited. Employees choose any plan on the individual market. | Limited. Employer offers a few pre-selected plan options. |

| Flexibility | High. Works for remote, part-time, and distributed teams easily. | Low. Tied to a single carrier; difficult for multi-state teams. |

| Admin Workload | Minimal. Managed through software; no plan selection or renewals. | High. Requires annual renewals, plan negotiations, and complex compliance. |

| Personalization | Tailored. Each employee gets a plan that fits their unique health needs. | One-size-fits-all. A single plan design must cover everyone. |

Ultimately, the table shows a fundamental divide: ICHRAs are built for flexibility and predictable costs, while traditional plans are built around a more rigid, top-down structure.

Administration and Geographic Freedom

Managing a traditional group plan is notoriously complicated, especially if you have a remote or distributed team. Trying to find a single plan that works across different states is a logistical nightmare—and often impossible. If you want to dive deeper into those complexities, you can explore our guide on group health insurance.

An ICHRA makes this so much simpler. Because employees buy plans on their local individual market, your company can have staff in 50 different states, all covered under one simple ICHRA. You just provide the allowance, and each employee finds a plan that works right where they live.

The eye-watering costs of traditional plans are pushing more businesses to make the switch. Employer-sponsored family coverage can easily cost $27,000 a year. And on top of that, these plans often come with sky-high deductibles—averaging $1,886—with 72% of workers facing out-of-pocket maximums over $3,000. An ICHRA paired with an individual plan offers a much clearer, more honest alternative. You can see the numbers for yourself and learn more about these health insurance cost trends.

Who Should Consider an ICHRA

The Individual Coverage Health Reimbursement Arrangement (ICHRA) isn't some niche product for a specific type of company. It’s a flexible, powerful tool for a whole range of businesses—especially those who feel trapped by the limits of traditional health insurance.

An ICHRA solves real problems, from small businesses tired of unpredictable costs to employees who just want more say in their coverage. It’s built for anyone who thinks health benefits should be adaptable, predictable, and put people back in the driver’s seat.

Small Businesses and Non-Profits

For any small or medium-sized business, the annual group health insurance renewal feels like a financial rollercoaster. Premiums spike without warning, forcing you to make tough choices between your budget and your team's benefits. An ICHRA is your off-ramp from that chaotic cycle.

By setting a fixed monthly contribution, business owners get 100% predictable health benefit costs. That kind of financial stability is a game-changer. It lets you offer competitive benefits without putting your bottom line at risk. This is especially huge for non-profits, where every single dollar has to count toward the mission.

An ICHRA allows an organization to stop guessing what its healthcare costs will be and start dictating them. It transforms the benefits budget from a volatile liability into a fixed, manageable expense.

This model also makes administration worlds simpler. Instead of battling insurance carriers and managing complicated plans, your only job is to fund the employee allowances. Easy.

Companies with a Distributed Workforce

Is your team spread out across different cities or states? Then you already know the nightmare of finding a single group plan that actually works for everyone. A plan with a great network in one state could be practically useless for an employee just a few hundred miles away.

An ICHRA completely sidesteps this problem. Because it’s geographically neutral, it's a perfect fit for:

- Fully Remote Companies: Offer a consistent, valuable benefit to everyone, no matter where they call home.

- Businesses with Multiple Locations: Stop juggling different regional health plans and bring everything under one simple ICHRA.

- Organizations with Hybrid Teams: Give your in-office and remote staff the exact same great benefit.

Since every employee shops for a plan on their local market, they’re guaranteed to find coverage with doctors and hospitals in their area. This makes the benefit equally valuable to every single person on your team.

Employees Seeking Flexibility and Choice

The real magic of an ICHRA is how much it empowers employees. So many people, especially those in working-class families or with unique health needs, find traditional plans too rigid. A one-size-fits-all plan rarely fits anyone perfectly.

For them, an ICHRA is liberating. It lets them use their employer's tax-free money to buy a plan that actually fits their family. Maybe that means choosing a plan with a lower deductible, one that covers a specific pediatric specialist, or one with better mental health coverage.

This empowerment is a lifeline for working-class families and anyone with unstable job-based health options. An ICHRA lets employers of all sizes fund employee-purchased individual insurance tax-free, avoiding the mess of group plans where family premiums recently hit an eye-watering $26,993. It's a huge relief for the 29% of workers stuck with high-deductible plans or the 34% of people facing deductibles over $2,000. By pairing an ICHRA with an individual plan, employees get both choice and protection with out-of-pocket maximums capped at $9,200 for individuals and $18,400 for families. You can learn more about how an ICHRA offers a smarter path forward for many families on ehealthinsurance.com.

Industries with Varied Employee Needs

Some industries are practically tailor-made for the ICHRA model because their workforces are so diverse. In these sectors, a single group plan is almost guaranteed to be a bad fit for a huge chunk of the team.

Think about businesses like these:

- Restaurants and Hospitality: These places often have a mix of full-time salaried managers, full-time hourly staff, and part-timers. An ICHRA lets the employer create different allowance classes for each group, making the benefits both fair and affordable.

- Construction and Trades: With crews moving between job sites and work fluctuating with the seasons, a portable health benefit is a massive advantage. An ICHRA lets workers keep their chosen health plan, even if their job status changes.

- Startups and Tech Companies: Fast-growing startups need to attract top talent with great benefits but can't afford the administrative headache of a complex group plan. An ICHRA is a lean, scalable solution that gives employees the premium benefits they’re looking for.

In every one of these cases, the ICHRA offers a personalized approach that a rigid group plan just can’t touch. It meets people where they are, giving them a benefit that works for their life and their job. If any of this sounds familiar, an ICHRA is definitely worth a closer look.

Navigating the Rules of an ICHRA

While an Individual Coverage HRA (ICHRA) gives you incredible freedom, it’s not a free-for-all. Think of the rules not as red tape, but as the guardrails that keep this flexible benefit model fair, compliant, and working for everyone.

Getting a handle on these rules is key. For employers, it means offering the benefit correctly. For employees, it means making the smartest choice for their health coverage. Let’s break down the big ideas into simple, clear pieces.

Customizing Allowances with Employee Classes

One of the most powerful features of an ICHRA is the ability to offer different allowance amounts to different groups of employees. You do this by organizing your team into employee classes.

This isn’t about picking favorites. It’s a structured, legitimate way to tailor benefits based on real job-based differences. You can't just create a class for one person, but you can segment your team using established categories like:

- Full-time vs. Part-time Employees: It makes sense to offer a larger allowance to full-time staff.

- Salaried vs. Hourly Employees: These are distinct compensation structures, and their benefits can be, too.

- Geographic Location: If you have teams in New York City and rural Idaho, you can adjust allowances to match local insurance costs.

- Seasonal or Temporary Employees: This lets you provide benefits that fit the nature of non-permanent work.

This system gives you pinpoint control over your budget while still distributing benefits fairly. It's a huge reason why the ICHRA is so adaptable to nearly any business.

The golden rule is fairness. As long as the allowance is the same for everyone within a class, you have the flexibility to design a benefits strategy that fits your company perfectly.

Understanding the Affordability Rules

For larger businesses—specifically those with 50 or more full-time equivalent employees—there’s an important concept called affordability. This regulation ensures the ICHRA you offer is a meaningful benefit, not just a token gesture.

Basically, the health plan an employee can buy with their allowance has to be considered "affordable" by government standards. The official calculation is a bit complicated, but it boils down to this: an employee's out-of-pocket cost for the cheapest silver plan in their area can't be more than a set percentage of their household income.

Thankfully, you don't need a math degree to figure this out. Most companies handle the complexities by outsourcing employee benefits administration to experts with software that does the calculations for you. And if you’re a small business? This rule doesn't even apply, giving you even more wiggle room.

ICHRA and Government Subsidies

This is a huge one for employees to get right. An ICHRA offer can directly impact your eligibility for Premium Tax Credits (PTCs)—the government subsidies that make marketplace plans more affordable.

Here’s the breakdown:

- If the ICHRA offer is affordable: The employee is not eligible for government subsidies, even if they turn down the ICHRA. They have to use the company’s money.

- If the ICHRA offer is unaffordable: The employee gets a choice. They can either take the company's ICHRA money or they can reject it and claim their PTCs on the marketplace instead.

This is why employees must look closely at their ICHRA offer. A financial advisor can help run the numbers to see which path saves them the most money. If you want to dive deeper into how different health accounts work together, our article on the differences between an HSA and an HRA is a great place to start.

Let's Answer Your Top ICHRA Questions

As more people discover the Individual Coverage HRA (ICHRA), it’s only natural to have a few questions. How does it really work day-to-day? Let's clear up some of the most common ones so you can feel confident about what an ICHRA means for you.

One of the biggest questions we hear is about what happens when you leave your job. Can you take the ICHRA money with you? The short answer is no—the allowance is tied to your employer. But here's the game-changer: the health insurance plan you bought with it is 100% yours. You can keep that plan without any interruption, which is a massive upgrade from losing your group coverage every time you switch jobs.

Can an ICHRA Cover More Than Just Premiums?

This is a great question, and the answer really shows off the ICHRA's flexibility. While its main job is to reimburse you for your health insurance premiums, employers can design a much more generous benefit if they want to.

An employer can set up their ICHRA to also reimburse other qualified medical expenses. Think about things like:

- Deductibles

- Copayments and coinsurance

- Dental and vision care

- Prescription drugs

This turns the ICHRA from a simple premium-reimbursement tool into a more powerful and complete health benefit. It's totally up to the employer to decide how much value they want to provide.

Is an ICHRA a Stable, Long-Term Benefit?

Some people worry that ICHRAs are just a passing trend. But since they first rolled out in 2020, they have proven to be a durable and incredibly popular alternative to old-school group plans. Their staying power is so clear that Congress has already made multiple proposals to write the ICHRA permanently into federal law.

While recent legislative efforts to expand the ICHRA didn't pass in full, the consistent bipartisan interest sends a strong signal. Lawmakers on both sides see its value, which means ICHRAs are not a temporary fix but a permanent part of the benefits landscape.

This long-term stability should give everyone peace of mind. Choosing an ICHRA is a strategic move toward a modern, employee-first benefits model that’s built to last. It’s a reliable way to offer great health coverage for years to come, adapting to what people actually need without the volatility of traditional insurance.

Ready to explore a smarter way to manage health benefits? The experts at My Policy Quote can help you find the perfect individual plan to pair with an ICHRA, ensuring you get the most out of your coverage. https://mypolicyquote.com