When you hear "Medicaid income requirements," it's easy to think there's a single magic number you need to be under. But the truth is, there isn't one. It’s not that simple.

Figuring out if you qualify is less about a national rule and more about your specific situation—where you live, how many people are in your family, and which group you fall into (like a pregnant woman, a child, or an adult without disabilities).

Decoding Medicaid Income Eligibility

Trying to understand Medicaid's financial rules can feel like solving a puzzle where the pieces keep changing depending on which state you're in. At its core, it’s a straightforward comparison: how does your income stack up against the limit your state has set?

These limits aren’t pulled out of thin air. They’re tied to the Federal Poverty Level (FPL), which is the government's baseline for what it means to live in poverty in the U.S. Each state then uses a percentage of that FPL to set its own income cutoffs.

Think of it this way:

- Your State Calls the Shots: A single person in Texas might have a very different income limit than a single person in California. One state might say you qualify with a $20,000 annual income, while another might have a much lower threshold.

- Household Size Is a Big Deal: The more people in your household, the higher the income limit. A family of four has more room to breathe financially than a single individual, and the rules reflect that.

- Who You Are Matters: The income limit for a pregnant woman is often significantly higher than for a childless adult. Different groups have different needs and, therefore, different rules.

Why Your State's Choices Are Everything

One of the biggest game-changers is whether your state decided to expand Medicaid under the Affordable Care Act (ACA). This is huge.

In states that expanded Medicaid, most adults with incomes up to 138% of the FPL can get coverage. This opened the door for millions of people. But in states that didn't expand, the rules are often much, much stricter, especially for adults who don't have dependent kids. We're talking about a difference of thousands of dollars in annual income just by crossing a state line.

The most important thing to remember is this: where you live and who’s in your family are just as critical as your paycheck when it comes to qualifying for Medicaid.

To help you keep track of these moving parts, here’s a quick summary of the core ideas.

Key Medicaid Income Concepts at a Glance

This table breaks down the core concepts for a quick reference, helping you grasp the essentials immediately.

| Concept | What It Means for You |

|---|---|

| Federal Poverty Level (FPL) | This is the national baseline. Your state uses a percentage of this number (like 138%) to set its income limit. |

| Modified Adjusted Gross Income (MAGI) | This is the specific income figure Medicaid uses. It’s not just your salary; it’s a specific calculation based on your tax return. |

| Household Size | The more people who depend on your income, the higher your income limit will be. |

| Eligibility Group | Different rules apply if you're a child, parent, pregnant woman, or a non-disabled adult. |

| State Expansion | Whether your state expanded Medicaid under the ACA is the biggest factor determining income limits for adults. |

These concepts all work together to determine your eligibility.

Ultimately, these income rules exist to make sure that people who need help the most can get it. Medicaid is a lifeline for so many, covering everything from doctor visits to long-term support. Understanding how your income fits into the picture becomes even more crucial when you consider the actual cost of home care services and realize how essential this support can be.

What Are MAGI and the Federal Poverty Level?

To get a real handle on Medicaid income rules, you need to know two key terms that are the foundation of every eligibility decision: the Federal Poverty Level (FPL) and Modified Adjusted Gross Income (MAGI).

They might sound like complicated government jargon, but they’re actually just the tools states use to figure out who qualifies. Think of them this way: one is the measuring stick, and the other is the method for measuring.

The Federal Poverty Level as a National Benchmark

The Federal Poverty Level (FPL) is the official measuring stick. Every year, the Department of Health and Human Services releases these numbers to create a standard income line for what’s considered poverty in the U.S.

It’s not just one number—it changes based on how many people are in your household. A single person has one FPL, while a family of four has a much higher one. It’s a baseline for fairness.

States don't just use the raw FPL number, though. Instead, they use a percentage of it. You’ll see Medicaid income limits written as things like 138% of the FPL or 210% of the FPL. This lets states set their own rules while still using a consistent national standard.

For example, the ACA’s Medicaid expansion set a new income limit for adults in many states at 138% of the FPL. That percentage translates into a clear dollar amount that gets updated annually, creating a straightforward cutoff for millions of people.

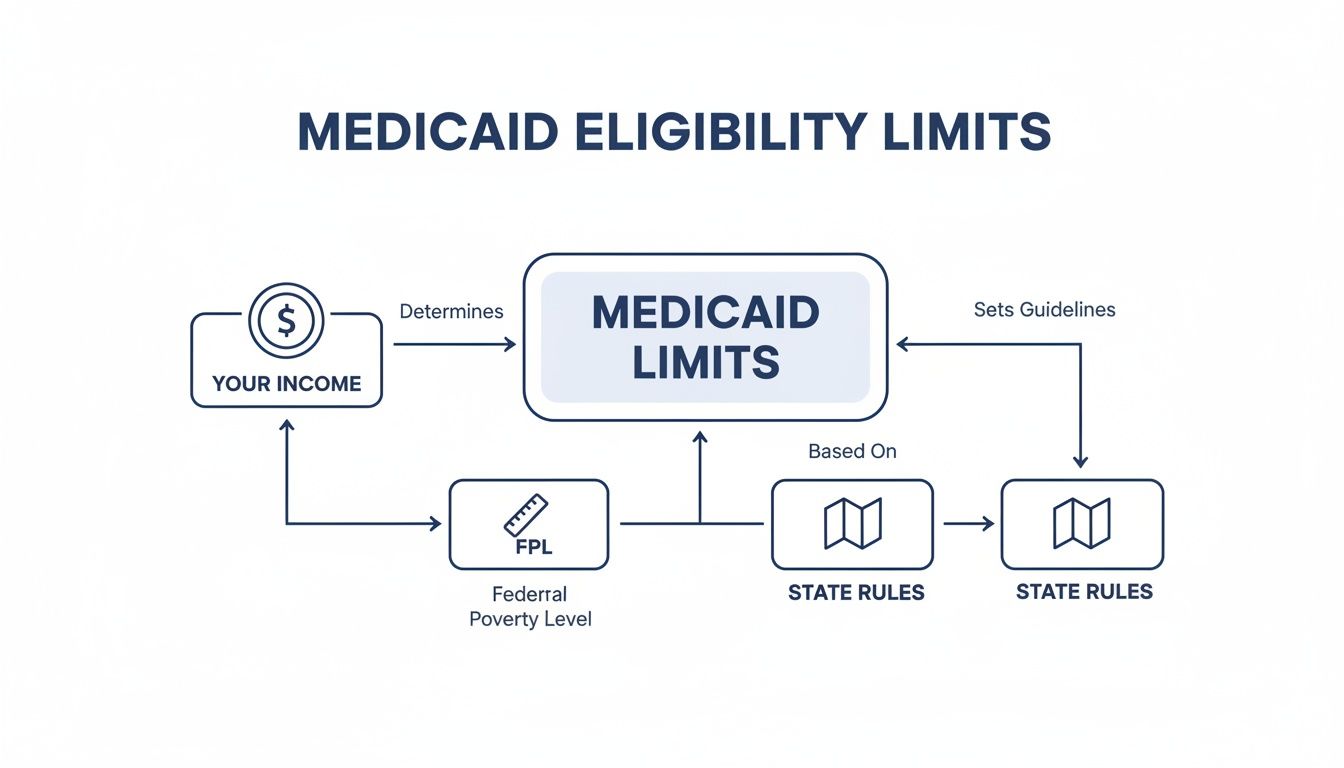

This flowchart shows how your income, the FPL, and your state’s rules all work together.

As you can see, your income is measured against the FPL benchmark, but your state gets the final say on the exact limit.

Understanding Modified Adjusted Gross Income

So if the FPL is the measuring stick, then Modified Adjusted Gross Income (MAGI) is how they decide what to measure.

MAGI isn’t just your paycheck. It’s a specific formula based on the numbers you report on your federal tax return.

For most people, MAGI is almost the same as their Adjusted Gross Income (AGI) from their tax forms. It starts with your AGI and then adds back a few specific things, like untaxed foreign income or tax-exempt interest. Getting lost in the financial terms is easy, but our health insurance glossary can help clear things up.

Key Takeaway: MAGI is a standardized way to count income. The whole point is to create a single, fair system for both Medicaid and other health insurance programs, making sure everyone is measured the same way.

So, what does this actually mean for you? It means Medicaid looks at certain types of income but completely ignores others.

-

Countable Income (Included in MAGI):

- Wages, salaries, tips

- Net income from freelance or self-employment work

- Unemployment benefits

- Most Social Security benefits (retirement, disability)

- Pension and retirement account withdrawals

-

Non-Countable Income (Excluded from MAGI):

- Child support you receive

- Supplemental Security Income (SSI)

- Veterans’ disability benefits

- Workers’ compensation

- Scholarships or grants used for tuition

This is a huge deal. If a source of money is excluded from MAGI, it won't be held against you when you apply for Medicaid. For many families, that can make all the difference. Once you understand both the FPL and how your MAGI is calculated, you'll be able to get a much better idea of where you stand before you even start the application.

How Your State Sets Medicaid Income Rules

Where you live is the single most important factor in figuring out if your income qualifies for Medicaid. While the federal government sets the basic foundation, each state gets to build its own system on top of it. That choice has created two completely different realities for people trying to get coverage across the US.

The biggest dividing line? Whether your state adopted Medicaid expansion under the Affordable Care Act (ACA). This one decision drastically changes who can qualify, especially for adults who don't have dependent children.

The Impact of Medicaid Expansion States

In states that expanded Medicaid, the door to health coverage swung wide open. The goal was to simplify the rules and create one clear income limit for most adults.

These states typically offer Medicaid to adults under 65 who have a household income up to 138% of the Federal Poverty Level (FPL). This created a lifeline for millions of low-income workers, gig economy freelancers, and people between jobs who never would have qualified before.

For instance, a single person in an expansion state could qualify with an income of roughly $20,782 a year (based on 2024 FPL numbers). It’s a total game-changer if you don't get insurance through a job.

Navigating Stricter Non-Expansion State Rules

Life is much different in the states that did not expand Medicaid. The rules are far more restrictive, and the income limits can be shockingly low. Eligibility is often reserved for very specific groups of people.

In these states, the income limit for an adult with no dependent children can be almost nothing—sometimes even 0% of the FPL. This means that unless you fall into a specific category—like being pregnant, caring for a young child, having a disability, or being elderly—you probably can't get Medicaid, no matter how little you earn.

This creates a painful situation known as the “coverage gap.”

The coverage gap traps people who make too much to qualify for their state’s strict, old-school Medicaid rules but not enough to get financial help (subsidies) to buy a plan on the Health Insurance Marketplace. They are left with literally no affordable options.

If you find yourself in this gap, it’s frustrating, but don't give up. You may need to explore other avenues for coverage. Our guide on where to find cheap health insurance can walk you through other possibilities that might be available.

A Tale of Two States

To really see how much your address matters, let's put these two scenarios side-by-side. The table below shows just how different the outcome can be for a single, non-disabled adult depending on their state's decision.

Expansion vs. Non-Expansion State Eligibility Example

| Scenario | Expansion State (Income Limit ~138% FPL) | Non-Expansion State (Typical Limit for Childless Adult) |

|---|---|---|

| Annual Income Limit | Roughly $20,782 | Often $0 (No eligibility pathway exists) |

| Eligibility Outcome | An individual earning $18,000 a year would likely qualify. | An individual earning $10,000 a year would likely be denied. |

| Key Difference | Coverage is available based on income alone. | Coverage is tied to being in a specific category (e.g., pregnant, disabled). |

This stark contrast isn't just theoretical; it has a massive, real-world impact on millions of people. It’s why knowing your state’s rules is the absolute first step.

National data shows that roughly 69.8 million people were enrolled in Medicaid, with another 7.25 million in the Children's Health Insurance Program (CHIP). These numbers aren't just statistics—they represent millions of lives directly affected by these state-by-state decisions.

Calculating Your Income for Medicaid

Alright, you've got the basics down—MAGI and FPL aren't just confusing acronyms anymore. But now comes the real work: turning your unique financial life into the numbers Medicaid needs to see. This part can feel a little intimidating, especially if your money doesn't come from a simple, steady paycheck.

For freelancers, early retirees, and families juggling multiple jobs, this is the most important part of the entire application. Getting it right can be the difference between a sigh of relief and a frustrating denial.

Calculating Income When You're Self-Employed

If you’re a 1099 contractor, freelancer, or run your own small business, Medicaid doesn’t look at your gross revenue—that big number you see before any expenses. Instead, they care about your net income, which is your profit after you subtract your legitimate business costs. This is a huge distinction.

Think of it this way: your gross income is the whole pizza, but Medicaid is only interested in the slices you actually get to keep after paying for all the ingredients.

To figure out your net income, you'll start with what you earned and then subtract all your allowable business expenses. These are the same kinds of deductions you’d claim on your tax return.

Common Business Deductions:

- Office Supplies: Think paper, ink, and other materials that keep your work flowing.

- Software and Subscriptions: Monthly fees for tools like Adobe or project management software count.

- Mileage: If you use your personal car for business, you can deduct the standard mileage rate.

- Home Office Deduction: A portion of your rent or mortgage if you have a dedicated workspace at home.

- Business Insurance: Any premiums for liability or professional insurance policies.

Deducting these expenses lowers your countable MAGI, which can make a real difference in whether you meet the income requirements for medicaid.

Navigating Income for Retirees and Families

Retirement funds and fluctuating family paychecks have their own set of rules. It’s not just about what you’re earning right now, but about how different kinds of money are counted by Medicaid.

Important Note: For most people under 65, the process is MAGI-based. But for applicants who are aged, blind, or disabled, different rules often apply, and your assets might be considered, too.

Let’s break down how to handle these situations.

Early Retirees and Pre-Medicare Adults

Retired before 65? Your income might be coming from a few different places. Here’s how Medicaid generally sees them:

- 401(k) or IRA Withdrawals: The amount you actually withdraw is counted as income.

- Pension Payments: Regular payments from a pension plan are definitely included in your MAGI.

- Social Security Retirement Benefits: Yep, most of these benefits are considered countable income.

But here’s the good news: the money just sitting in your retirement accounts? As long as it stays there, it’s not counted as income for MAGI-based Medicaid. Only the funds you actually take out and use are part of the calculation.

Families with Fluctuating Paychecks

When you have variable hours, seasonal jobs, or several income sources, figuring out a single monthly income number feels like a guessing game. Your goal is to give the most accurate snapshot of your current financial reality.

A simple way to do this is to average your income over the last few months—three is a good place to start. If your pay has changed dramatically just recently, use your latest pay stubs to project your monthly earnings. The key is to be realistic and base it on your recent history.

No matter your situation, keeping clear records is your best friend. Before you even start the application, it’s a great idea to gather your paperwork. Our guide on what documents you need to get insurance has a handy checklist that can make this whole process feel much less overwhelming. When you calculate your income correctly from the start, you can submit your application with confidence and avoid any unnecessary setbacks.

When Your Assets and Medical Bills Come into Play

For most people, getting Medicaid is all about one thing: income. This is the world of MAGI Medicaid, where what you own—like your savings account or your car—doesn’t even enter the conversation. But the rulebook flips completely for certain folks.

If you’re applying for Medicaid because you’re 65 or older, blind, or have a disability, you'll likely step into what’s called the “non-MAGI” world. Here, it’s not just about what you earn. It’s also about what you own.

Understanding Medicaid Asset Limits

Think of an asset limit as a second financial test you have to pass, right after the income one. It’s a hard cap on the total value of your resources. If your countable assets are over that line, you won’t be eligible, even if your income is well below the limit.

The good news? They don’t count everything you own against you. Medicaid knows you need to keep your home and other essentials to live.

What’s usually NOT counted?

- Your primary home: The house you live in is almost always protected.

- One vehicle: Your main set of wheels is exempt.

- Your personal stuff: Furniture, clothes, and appliances don't count.

- Pre-paid funeral plans: Money set aside in an irrevocable burial trust is often excluded.

What IS usually counted?

- Cash and bank accounts: Checking, savings, and any other liquid funds.

- Investments: Stocks, bonds, and mutual funds are all on the table.

- Extra property: A vacation home or a second car will count toward your limit.

The exact limit changes by state, but it’s often a very strict threshold—around $2,000 for an individual and $3,000 for a couple. It’s not a lot of wiggle room, which makes planning ahead critical.

How a Medicaid Spend-Down Can Be a Lifesaver

So what happens if your income is just a little too high to qualify under the non-MAGI rules? You might feel like you’re stuck in a tough spot, but many states offer a path forward called a Medicaid spend-down.

Imagine the income limit is a finish line you have to get under. A spend-down lets you subtract your medical bills from your income to "spend your way down" to that line.

A spend-down basically works like a deductible. You pay for your medical care out-of-pocket up to a certain amount. Once you hit that number, Medicaid steps in to cover the rest of your bills for that time period.

Let's walk through a quick example to see how it works.

A Simple Spend-Down Scenario:

- State's Monthly Income Limit: $1,200

- Your Monthly Income: $1,500

- Your "Excess Income": $300 ($1,500 – $1,200)

In this case, your spend-down amount is $300. To get Medicaid coverage for the month, you need to prove you’ve already paid for $300 in medical services. This could be anything from doctor’s visit co-pays and prescription costs to payments on old hospital bills.

Once you show you've met your spend-down, you’re eligible for Medicaid for the rest of that month. For people with high medical needs whose income is just over the line, this program is an absolute lifeline to the care they depend on.

Your Step-by-Step Medicaid Application Guide

Okay, so you've figured out the income rules. That’s a huge first step. But knowing the requirements is one thing; actually getting through the application is another.

Let's turn that knowledge into action. This guide will give you a clear, simple roadmap to follow, breaking down what can feel like a confusing process into manageable steps.

There are two main doors you can walk through to apply for Medicaid, and the right one for you usually depends on your state.

- The Health Insurance Marketplace: You can start at HealthCare.gov. The beauty of this is that a single application checks your eligibility for everything—Medicaid, CHIP, or a subsidized Marketplace plan. It’s a one-stop shop.

- Your State Medicaid Agency: You can also go straight to the source and apply directly with your state's agency. This is often the best route if you're applying based on age, blindness, or disability (the non-MAGI route).

Assembling Your Application Toolkit

Think of this like gathering your ingredients before you start cooking. Having everything ready ahead of time makes the whole process smoother and keeps you from scrambling later.

Before you sit down to apply, pull these documents together:

- Proof of Identity and Citizenship: Your birth certificate or a U.S. passport is perfect.

- Proof of Residency: A recent utility bill, your lease agreement, or even a driver's license will do the trick.

- Income Documentation: This is the big one. Grab your recent pay stubs, W-2 forms, or your latest tax return. If you're a freelancer, a simple profit and loss statement is what they'll want to see.

- Social Security Numbers: You'll need the number for every person in your household who is applying.

Having these items on hand means you can fill out the application accurately and hopefully avoid those follow-up letters asking for more information. For a deeper dive, our guide on how to qualify for Medicaid has even more details.

Pro Tips for a Smooth Application

Getting this done is about more than just filling in blanks on a form. A few insider tips can help you sidestep common headaches and get your application reviewed without delays.

The single biggest reason for application delays? Incomplete or wrong information. Seriously, double-check every single entry before you hit submit, especially your income numbers and how many people are in your household. A small typo can cause a major holdup.

Also, life happens. If you get a new job, someone moves in or out, or you move to a new address, report it right away. Most states require you to let them know about these changes within 10 to 30 days.

It also helps to understand the bigger picture of healthcare costs. For instance, you might want to learn more about the costs of ADHD testing and insurance coverage to see how specific medical needs and insurance plans interact.

And if your application is denied? Don't panic. You absolutely have the right to appeal the decision. The denial letter will explain exactly what steps you need to take next.

Got Questions About Medicaid Income Limits? We’ve Got Answers.

Even when you think you have a handle on the rules, real life has a way of throwing curveballs. When it comes to the income requirements for Medicaid, the devil is always in the details of your specific situation.

Let’s walk through some of the most common questions we hear from families, freelancers, and folks with fluctuating paychecks.

Does My Spouse's Income Count Toward My Medicaid Application?

Yes, in most situations, it absolutely does. Medicaid looks at your total household income, which is almost always based on how you file your taxes.

If you’re married and living together, your spouse's income gets included in the final calculation—even if they have their own insurance and aren't applying for coverage themselves. There are some niche exceptions, especially for non-MAGI Medicaid for long-term care, but for most people, the answer is yes.

What Happens if My Income Changes During the Year?

This is a big one. You are required to report any significant changes in your income to your state Medicaid agency, and you need to do it quickly—usually within 10 to 30 days.

If your income goes up, you might no longer be eligible for Medicaid. But don't panic! This change would likely trigger a Special Enrollment Period, allowing you to get a subsidized plan on the Health Insurance Marketplace.

On the flip side, a drop in income could mean you’re newly eligible for Medicaid. It's so important to keep your information current. It ensures you have the right coverage and keeps you from running into headaches later.

Staying on top of this is key. A quick update can save you a world of trouble.

Can I Have a Savings Account and Still Qualify for Medicaid?

It completely depends on which path you take to qualify for Medicaid.

- For most people under 65 (MAGI Medicaid): Good news—your savings are safe. There are no asset limits for this type of Medicaid. Your savings account, your car, and the value of your home don't count against you. It's all about your income.

- For those who are aged, blind, or disabled (non-MAGI Medicaid): This is where it gets tricky. Yes, there are very strict asset limits. An individual can typically only have $2,000 in countable assets. Your primary home and one car are usually exempt, but savings will definitely be counted.

I'm a Contractor. How Do I Report Income That's Always Changing?

When your income is up one month and down the next, the key is to give your best, honest estimate of your current monthly earnings. The state knows self-employment income isn't perfectly steady.

You can figure this out by averaging your income over the last few months. Another common way is to use your most recent tax return to project your annual income, then just divide that number by 12.

Just remember to always report your net income (what’s left after you subtract your business expenses), not your gross pay. It’s a good idea to have documents like invoices, bank statements, or a simple profit and loss statement ready in case they ask for proof.

Figuring out health insurance can feel like a maze, but you don't have to navigate it alone. The friendly experts at My Policy Quote are here to help you find coverage that actually fits your life and your budget. See what your options are today at https://mypolicyquote.com.