When you start looking into a term life insurance cost comparison, you might be pleasantly surprised. It's not uncommon for a healthy 30-year-old to find a $500,000 policy for as little as $25-$35 a month. But that's just a starting point—the actual price tag is shaped entirely by you: your age, your health, and the coverage you decide you need.

How Much Does Term Life Insurance Actually Cost

So many people put off buying life insurance because they assume it’s out of their budget. In reality, studies show that most people overestimate the true cost by three to six times. Term life insurance was designed from the ground up to be an affordable safety net for the years when your financial responsibilities are at their peak.

The premium you're offered isn't just a random number. It's the result of an insurance company carefully assessing risk. They look at a few key things to figure out your final rate:

- Your Age: It’s simple—the younger you are, the lower your rates will be.

- Your Health: A clean bill of health with no major or chronic conditions will always get you better pricing.

- Tobacco Use: This is a big one. Smokers can expect to pay a lot more than non-smokers.

- Policy Details: The length of the term (like 10, 20, or 30 years) and the total coverage amount are direct drivers of your monthly cost.

A Snapshot of Average Monthly Premiums

To give you a clearer idea, let's look at some real-world numbers. These estimates are a solid baseline for what you might pay, but remember, your quote will be unique to you.

The table below shows some sample monthly costs for a $500,000, 20-year term policy for a non-smoker in excellent health.

Sample Monthly Term Life Insurance Premiums at a Glance

| Age Group | Average Monthly Cost for Men | Average Monthly Cost for Women |

|---|---|---|

| 30 | $28 | $24 |

| 40 | $40 | $35 |

| 50 | $98 | $81 |

As you can see, locking in your rate while you’re young gives you a huge financial advantage over the life of the policy. The numbers don't lie, and they really show why doing a personalized term life insurance cost comparison is so critical.

Understanding Premium Structures

The cost of term life can vary quite a bit, but one thing is consistent: premiums almost always go up as you get older. Some policies, for example, use five-year age bands, which means your rate will tick up every five years as you move into a new age group.

It’s also important to remember that term policies don’t build cash value. This is what keeps them so simple and much more affordable than other types of life insurance. For a more detailed look at pricing, check out our guide on how much life insurance costs. This straightforward approach ensures you’re only paying for the death benefit protection your family truly needs, and nothing more.

Decoding the Factors That Drive Your Premium

Ever wonder how an insurance company comes up with your life insurance quote? It’s not just a random number. It’s the result of a careful risk assessment process called underwriting, where insurers look at your unique story to figure out how long you’re likely to live.

Knowing what they look for is a game-changer. It gives you real insight into your specific term life insurance cost comparison and puts you in the driver's seat to find the best possible rate.

Each piece of information, from your age to your job, helps the insurer build a picture. Once you understand how these pieces fit together, you can get a much better sense of what your final premium will be and even find ways to lower it.

Your Personal Demographics

At its core, underwriting starts with data. Insurers use massive actuarial tables to predict life expectancy, and two of the biggest factors are your age and gender.

-

Age: This is the big one. The younger you are when you lock in a policy, the lower your risk in the eyes of an insurer. That means lower premiums. Getting a policy in your 30s versus waiting until your 50s can literally save you thousands of dollars over the life of the term.

-

Gender: It's a simple statistical fact: women tend to live longer than men. Because of that, women usually pay less for life insurance than men of the same age and health.

These two factors set the baseline for your premium before anything else is even considered.

Your Health Profile and Classification

Right after demographics, your health takes center stage. Insurers will look at your medical records, prescription history, and often ask you to complete a simple medical exam. The goal is to place you into a specific health class.

This classification has a direct impact on what you'll pay:

- Preferred Plus/Super Preferred: Think of this as the A+ group. You’re in excellent health, have a clean family medical history, and are at an ideal weight. This gets you the absolute lowest premiums.

- Preferred: You're still in great shape but might have a minor, well-managed issue, like slightly high cholesterol controlled by medication. Your rates will still be very competitive.

- Standard Plus: This is for people in above-average health who might have a few more risk factors, like being a bit overweight or having a treated medical condition in their past.

- Standard: This is the category for an average person with average health. You might be managing a chronic condition well or be significantly overweight.

Where you land in these tiers is a huge part of any term life insurance cost comparison. Just moving from "Standard" to "Preferred" can lead to massive savings.

The High Cost of Tobacco Use

Nothing inflates a life insurance premium like using tobacco. Insurers see smoking as one of the biggest risks, period. Smokers can expect to pay anywhere from 200% to 400% more than a non-smoker for the exact same policy. The good news? If you quit, you can get your rate lowered after being tobacco-free for a year or two.

Lifestyle and Occupational Risks

Finally, insurers take a look at your life outside the doctor's office—what you do for work and for fun.

Most jobs won't change your rate at all. But if you have a high-risk profession like commercial fishing, logging, or piloting, it can lead to higher premiums. The same goes for hobbies considered dangerous, like scuba diving, rock climbing, or skydiving. You can learn more by exploring the different costs of term life insurance.

Even your driving record matters. A history of DUIs or reckless driving signals higher risk to an insurer. By looking at everything from your birthday to your weekend plans, the insurance company creates a complete profile to calculate a premium that’s fair for your specific situation.

Comparing Term Life Insurance Costs Side by Side

Theory is one thing, but seeing the raw numbers is what really clicks. A side-by-side look shows you just how much your age, the policy's term, and the coverage amount can swing your monthly premium. This is where a smart term life insurance cost comparison truly begins.

When you break it down like this, you move from abstract ideas to concrete dollars and cents. It allows you to line up your budget with your family's actual needs, making the whole process feel much more manageable. Let's get into the specifics.

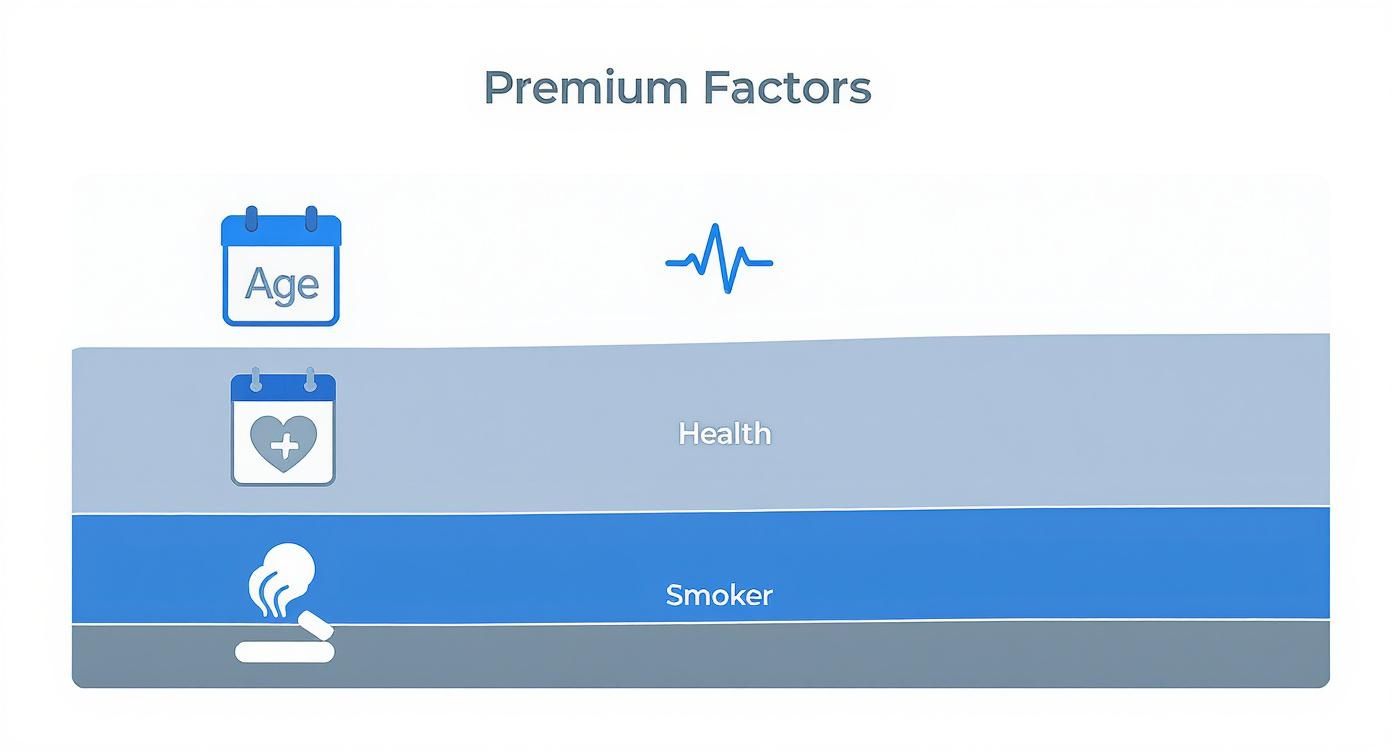

The infographic below really nails down the core factors that drive your premium. Age, health, and whether you smoke are the big three.

This visual just confirms it: while insurers look at a lot of things, these elements are the bedrock of how they calculate your risk—and your rate.

Premium Comparison by Age

Let’s be blunt: age is the single biggest factor in what you’ll pay. As you get older, the insurance company's risk goes up, and so do your premiums. Locking in a rate when you’re younger isn’t just a good idea; it’s a massive long-term savings strategy.

Just look at the difference in monthly premiums for a $500,000, 20-year term policy for a healthy non-smoker at various stages of life.

| Age | Estimated Monthly Premium for Men | Estimated Monthly Premium for Women |

|---|---|---|

| 30 | $28 | $24 |

| 40 | $40 | $35 |

| 50 | $98 | $81 |

See that? The premium for a 50-year-old is more than triple what a 30-year-old pays. That’s not a small jump. It’s a powerful reminder that the best time to get covered was yesterday—and the next best time is right now.

Premium Comparison by Term Length

How long you want the coverage also plays a huge role. A longer term means the insurance company is on the hook for a longer period, which naturally increases their risk. This is why a 30-year term will always cost more than a 10-year term, all else being equal.

Here’s a snapshot of how monthly premiums for a $500,000 policy for a healthy, 35-year-old non-smoker change based on the term.

| Term Length | Estimated Monthly Premium for Men | Estimated Monthly Premium for Women |

|---|---|---|

| 10 Years | $21 | $19 |

| 20 Years | $32 | $28 |

| 30 Years | $55 | $47 |

The jump from a 20-year to a 30-year term is pretty significant. The key is to match your term length to your biggest financial responsibility, like your mortgage or until the kids are on their own, without paying for more than you need.

Premium Comparison by Coverage Amount

And finally, the most straightforward factor: the size of the death benefit. More coverage costs more. Simple. The real art is finding that sweet spot where you have enough protection for your family without breaking your monthly budget.

This table shows the estimated monthly premiums for a healthy, 40-year-old non-smoker with a 20-year term at different coverage levels.

| Coverage Amount | Estimated Monthly Premium for Men | Estimated Monthly Premium for Women |

|---|---|---|

| $250,000 | $24 | $21 |

| $500,000 | $40 | $35 |

| $1,000,000 | $72 | $61 |

Notice that doubling the coverage from $500,000 to $1,000,000 doesn't actually double the cost. Insurers often give you a better rate per dollar on larger policies, which means that big-time peace of mind might be more affordable than you think.

Strategic Insight for Smart Shoppers

When you’re comparing policies, don't just chase the lowest number. Look at the value. Sometimes paying a few extra bucks a month for a much larger death benefit or a longer term gives your loved ones a disproportionately larger safety net.

The good news is that the insurance market is competitive, and that works in your favor. In 2025, term life policies made up about 19% of the U.S. life insurance market. While that's a small dip from past years, the explosion of online platforms has forced carriers to compete fiercely on price. It's never been easier to shop around.

For instance, a healthy 30-year-old guy might snag a $500,000 20-year policy for $15 to $25 a month, but someone just 20 years older could pay three or four times that. This just proves that taking the time to compare quotes is absolutely worth it. You can explore more about life insurance market trends at MoneyGeek.com.

By looking closely at these tables, you can start to build a policy that fits your life. The data makes it crystal clear: small tweaks to age, term, and coverage lead to big differences in cost. Use this knowledge to run a truly effective term life insurance cost comparison.

Real-World Scenarios and Cost Breakdowns

The data tables are a great starting point, but let’s be honest—numbers on a chart don't tell the whole story. To really get a feel for how a term life insurance cost comparison works, it helps to see how policies are built for real people with real lives.

When you connect coverage amounts and term lengths to actual life events, an abstract policy becomes a powerful financial safety net. Let’s walk through a few common scenarios to see what this looks like in practice.

Think of these profiles as a way to translate numbers on a page into a practical protection plan for your own family.

Persona 1: The New Parents

Meet Mark and Sarah. They're both 32 years old, healthy non-smokers, and just welcomed their first child. They have a $350,000 mortgage with 28 years left and want to make sure their new baby will be secure all the way through college.

Their goals are crystal clear:

- Wipe out the mortgage balance.

- Replace their incomes until their child is grown.

- Set aside a fund for future education costs.

A 30-year term makes perfect sense here. It covers them until the house is paid off and their child is well past their college years. A combined $1.5 million in coverage ($750,000 each) would comfortably handle their debts, replace their paychecks, and secure their child’s educational future.

Estimated Cost Breakdown:

- Mark (32-year-old male): A $750,000, 30-year term policy would run about $48 per month.

- Sarah (32-year-old female): The same $750,000, 30-year term policy would be around $41 per month.

For less than $90 a month, they can lock in total peace of mind for the next three decades.

Persona 2: The Recent Homebuyer

Now, let's look at Jessica, a 40-year-old single professional who just bought her first home. She’s in excellent health and a non-smoker. Her biggest worry is that her $400,000, 30-year mortgage could become a burden for her family if anything happened to her.

Because her primary goal is protecting her home, her insurance strategy can be laser-focused. A 30-year term policy aligns perfectly with her loan.

Situational Recommendation: A $500,000 policy is a smart move. It covers the entire mortgage and leaves an extra $100,000 to handle final expenses, property taxes, or other debts without forcing her family to sell the house under pressure.

Estimated Cost Breakdown:

- Jessica (40-year-old female): A $500,000, 30-year term policy would likely cost her around $54 per month.

That small monthly payment guarantees her biggest asset is protected. That’s what peace of mind is all about.

Persona 3: The Small Business Owner

Finally, meet David, a 45-year-old who co-owns a small marketing agency. He's in good health but has slightly elevated cholesterol, putting him in a "Standard Plus" health class. He also has a personally guaranteed Small Business Administration (SBA) loan for $250,000.

David’s needs are twofold: he needs to protect his family from his business debt and ensure his partner can keep the company running. His policy has to cover the loan and potentially fund their buy-sell agreement.

A 20-year term fits well with the business's growth plan and the loan’s timeline. To pin down the right coverage amount, it’s best to use a detailed life insurance needs calculator that can account for business-specific liabilities.

Estimated Cost Breakdown:

- David (45-year-old male, Standard Plus): A $500,000, 20-year term policy would cost approximately $65 per month.

This coverage ensures his personal assets are shielded from his business debts—a critical move for any entrepreneur. Each of these stories shows that the key isn't just buying insurance; it's about tailoring it to your specific financial timelines and responsibilities.

A Practical Guide to Comparing Quotes

Alright, you understand how premiums work, so now it’s time to find the best deal. Getting a great rate on term life insurance is about more than just luck—it’s about having a smart game plan.

Shopping for quotes isn't just about plugging your age into a website and picking the cheapest option. It’s about being prepared, knowing what you're looking for, and making sure every policy you look at is on a level playing field. Let's walk through it.

Step 1: Get Your Info Ready

Before you even think about filling out a form, take a few minutes to get organized. Insurers need a clear picture of who you are to give you an accurate starting quote. Having everything in one place makes the whole process faster and way less stressful.

Here’s a quick checklist of what you'll need:

- The Basics: Your full name, date of birth, and contact info.

- Your Health Story: Jot down any current or past health issues, medications you’re taking, and your doctor's name and address.

- Family Health History: You’ll likely be asked about the health of your immediate family (parents and siblings), especially regarding things like cancer, heart disease, or diabetes.

- Lifestyle Facts: Be ready to talk about your job, hobbies, driving record, and whether you use tobacco.

Honesty is everything here. If the insurance company finds out later that you weren't upfront, they could jack up your premium or even deny your coverage altogether.

Step 2: Compare Apples to Apples

This is the single most important rule. If you get a quote for a 20-year term from one company and a 30-year term from another, you’re not really comparing them. It’s like trying to decide between a sedan and a pickup truck based on price alone—they’re built for different things.

To get a true comparison, make sure these three things are identical for every quote you request:

- Term Length: Are you looking for 10, 20, or 30 years? Pick one and stick to it.

- Coverage Amount: Whether it’s $250,000, $500,000, or $1 million, use the same number everywhere.

- Policy Riders: If you want a specific add-on, like an accelerated death benefit, make sure it’s included in every quote.

Crucial Takeaway: A cheap quote means nothing if the policy details don't match up. An apples-to-apples comparison is the only way to find out which company truly offers the best value for the protection you need.

The global life insurance market is massive—we’re talking about a $3.1 trillion industry in 2024, and the U.S. makes up nearly 27% of that. That intense competition is exactly why you see such different prices from one insurer to the next for the very same person.

Step 3: Use the Right Tools and People

You’ve got two main ways to gather quotes: go directly to each insurance company one by one, or work with an independent agent or broker.

Online comparison tools are great for getting a quick, bird's-eye view of the market. In just a few minutes, you can see dozens of preliminary rates lined up side-by-side.

But don’t underestimate the value of a human expert. An independent agent lives and breathes this stuff. They know which carriers are more forgiving about certain health conditions or which ones have the smoothest application process. They can be a huge help, especially if your situation isn’t perfectly straightforward. For a deeper dive, check out our guide on comparing life insurance quotes.

By following these steps, you’re no longer just a shopper—you’re an informed buyer, ready to lock in the best policy at the best price.

Your Questions Answered: Getting Clear on Term Life Costs

As you get closer to a decision, a few last questions always pop up. It's completely normal. This is about making sure you feel 100% confident in the choice you're making for your family. Let's clear up some of the most common things people ask when they’re comparing term life policies.

My goal here is to give you simple, direct answers so you can finalize your plan and lock in the right protection.

How Can I Get My Premiums as Low as Possible?

Lowering your premium isn’t about some secret coupon code; it’s about showing the insurance company you’re a low-risk person to cover. The good news? You have a ton of control over the things that matter most. A few smart moves can save you a surprising amount of money over the years.

Here’s what really works:

- Dial in Your Health. Even small improvements can make a big difference. If you can get your cholesterol or blood pressure down, or even lose a few pounds, you could qualify for a better health class. That directly translates to lower rates.

- Quit Tobacco for Good. This is the single most powerful way to slash your costs. Once you've been tobacco-free for one to two years, you can ask for a new rate. It's not uncommon to see premiums drop by an incredible 200% to 400%.

- Pick the Right Term Length. Don’t pay for more than you need. The goal is to match your policy's term to your biggest financial responsibility, like your mortgage. If a 20-year term covers that, it will be significantly cheaper than a 30-year policy.

- Shop Around. Always. Never, ever take the first quote you get. The prices for the exact same coverage can be wildly different from one carrier to the next. Getting at least three to five quotes isn't just a good idea—it's essential.

A Pro Move: Laddering Your Policies

If you have different financial needs over time, you can "ladder" your policies. This just means buying a few smaller policies with different term lengths. For example, you could get a 30-year, $500,000 policy to cover the mortgage, plus a separate 20-year, $250,000 policy for college costs. As the smaller policies expire, your total coverage drops—and so do your costs.

How Much More Expensive Is Whole Life Compared to Term?

The price difference between term and whole life insurance is huge, and it all comes down to their purpose. They're built to do two completely different jobs, and their price tags reflect that.

Term life is pure, simple protection. You pay a premium for a specific number of years—the "term"—and if you pass away during that time, your family gets the payout. That’s it. There’s no cash value or investment component, which is exactly why it’s so affordable. For most families, it's the smartest, most cost-effective way to get a large amount of coverage.

Whole life, on the other hand, is built to last forever. A chunk of your (much higher) premium pays for the insurance, and another part goes into a cash value account that grows over time. Because it bundles a death benefit with a savings vehicle and never expires, it costs a lot more. A healthy 30-year-old might pay around $3,959 per year for a $500,000 whole life policy, while the same term policy could be just $187 per year.

Do I Really Need to Take a Medical Exam?

You can get term life insurance without a medical exam, but it’s usually not the cheapest option. These "no-exam" policies are all about speed and convenience—you can often get approved in minutes or days. But that convenience costs you.

When an insurer doesn't get to see your medical results, they're taking on more risk. They don't know what they don't know. To make up for it, they charge higher premiums and usually limit how much coverage you can buy, often capping it at $500,000 or less.

For most people who are in decent health, going through with a quick medical exam is the best financial move. It's simple: a paramedic comes to you, checks your height, weight, and blood pressure, and takes a small blood and urine sample. It gives the insurer a clear picture of your health, which allows them to give you their absolute best rates.

When Should I Buy Term Life Insurance?

The answer couldn't be simpler: right now. Or, more specifically, as soon as you have someone who depends on you financially.

As you saw in the comparison tables, your age is the biggest driver of your cost. A 30-year-old pays a fraction of what a 50-year-old pays for the exact same policy. Every single birthday you have, your potential rate goes up.

By locking in a policy when you're young and healthy, you secure a super-low premium that's fixed for the next two or three decades. It’s not just about protecting your loved ones; it’s about saving yourself a ton of money in the long run. The longer you put it off, the more you'll pay.

Ready to see how affordable your peace of mind can be? At My Policy Quote, we make the term life insurance cost comparison process simple and transparent. Get your free, personalized quote in minutes and find the perfect policy to protect your family's future. Visit us today at https://mypolicyquote.com.