When you're your own boss, the single best thing you can do for your future is to open a tax-advantaged retirement account—like a SEP IRA or Solo 401(k)—and put your contributions on autopilot. It’s a simple strategy that ensures you're consistently saving for tomorrow, no matter how much your income swings this month, all while letting your money grow with some serious tax perks.

The Reality of Retiring as Your Own Boss

The freedom of self-employment is incredible, but it comes with a catch: you are 100% in charge of your financial future. There’s no HR department to hand you a 401(k) packet. No company match to give your savings a boost. You’re the one who has to build your retirement plan from the ground up, from picking the account to making sure it gets funded.

Honestly, that can feel like a lot. You’re already busy running your business, chasing invoices, and keeping clients happy. To make it all work, you need more than just your core skills; you need a solid business mindset, which includes mastering project management for freelancers to build the kind of stable income that makes saving possible in the first place.

Understanding the Savings Gap

For entrepreneurs, the stakes are just higher. A 2025 Transamerica Institute survey found that self-employed folks believe they need a median of $700,000 to retire comfortably—way more than their traditionally employed peers.

Even so, a staggering 13% of self-employed people have zero retirement savings. That’s nearly double the rate for regular employees. You can dig into more of the numbers in this comprehensive retirement outlook survey.

This gap really gets to the heart of the challenge: how do you turn the hustle of today into real financial security for tomorrow? The good news? There are powerful tools designed specifically to help you do just that.

The single most important move you can make is to treat your retirement savings like a non-negotiable business expense. Pay yourself first, just as you would any other critical vendor.

Your First Actionable Steps

Getting started is less complicated than it seems. It really just comes down to a few key decisions that put you back in the driver's seat. This guide is here to cut through the noise and give you a clear, simple path to follow.

This table breaks down the immediate, high-impact moves you can make to get started.

| Immediate Actions for Self-Employed Retirement Savings |

| :— | :— | :— |

| Action Item | Why It Matters | Your First Step |

| Acknowledge Your Role | This mindset shift is everything. You're the CEO and the benefits manager. | Say it out loud: "I am responsible for my retirement." Then, block off one hour in your calendar this week to plan. |

| Choose Your Account | The right account maximizes tax benefits and aligns with your income. | Learn the basics of the SEP IRA and Solo 401(k). A quick search will give you the pros and cons of each. |

| Automate Everything | Consistency beats intensity. Automation ensures you save even when you're too busy to think about it. | Set up a recurring transfer from your business checking to your new retirement account. Start small if you have to. |

These steps lay the foundation, turning a vague goal into a concrete plan.

Thinking about the long-term also means planning for things like healthcare, which can become a major expense later in life. As you build your retirement fund, it’s a smart move to also learn about your options for retirement health insurance so you can make sure all your bases are truly covered.

Choosing the Right Retirement Account for You

Trying to figure out retirement accounts can feel like learning a new language. You hear acronyms like SEP, SIMPLE, and Solo 401(k) thrown around, and it's easy to feel lost. But let’s cut through the noise. The goal is simple: find the account that fits your business and helps you build wealth the best way possible.

Think of it like picking the right tool for a job. The best plan for a freelance designer with unpredictable income is going to be different from what a high-earning consultant needs. We'll break down the main options with real-world examples so you can see exactly which tool is right for you.

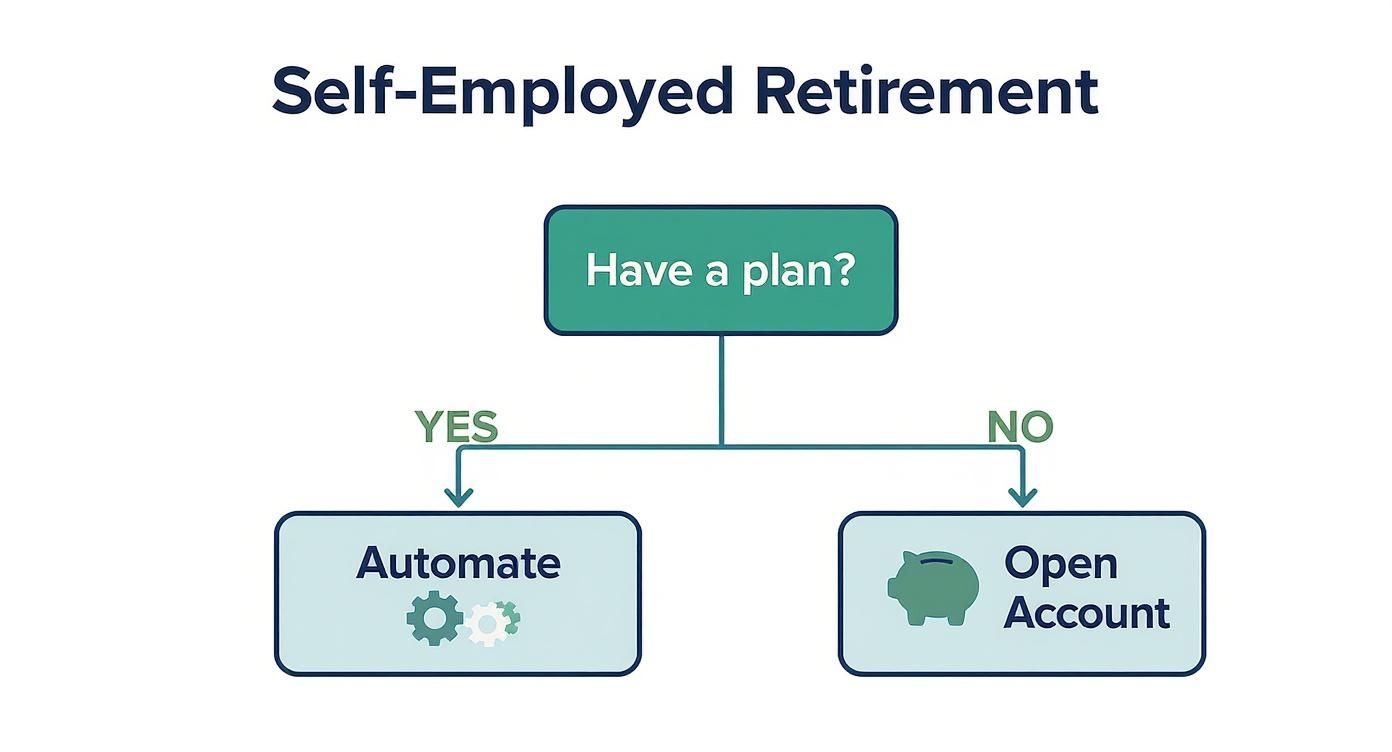

This decision tree gives you a quick visual of where to start, depending on whether you already have a plan.

The first step is a simple choice—either open a new account or kick the one you have into high gear by automating your contributions.

The SEP IRA For Maximum Flexibility

The Simplified Employee Pension (SEP) IRA is a huge favorite among freelancers and sole proprietors, and for one big reason: flexibility. There are no mandatory yearly contributions. Have a fantastic year? You can put away a serious chunk of cash. Hit a slow patch? You can contribute less—or nothing at all—without a penalty.

This is perfect for anyone whose income swings wildly. Imagine you’re a wedding photographer who earns 60% of your income between May and October. A SEP IRA lets you make a huge contribution after your busy season wraps up, instead of forcing you to save a fixed amount during the leaner winter months.

It also comes with high contribution limits. A SEP IRA lets you contribute up to 25% of your net earnings, with a maximum of $69,000 for the 2024 tax year. They are also super easy to open and can be set up as late as your tax filing deadline. You can find more details about top retirement options on myccmi.com.

Who is the SEP IRA for?

The freelance writer, graphic designer, or consultant with variable income who wants a simple, low-admin account with high contribution potential and the freedom to adjust contributions year by year.

The Solo 401(k) For Power Savers

The Solo 401(k) is the power move for high-earning self-employed people with no employees (besides a spouse). Its brilliant structure lets you contribute as both the "employee" and the "employer," which means you can save more, much faster.

Here’s how it works:

- As the "employee," you can put in up to $23,000 in 2024 ($30,500 if you're 50 or older).

- As the "employer," you can add another 25% of your compensation.

The combined total can’t go over $69,000 for 2024, but that dual-contribution structure is a real game-changer. A consultant making $150,000 could max out their employee contribution and then pile a big employer contribution on top, supercharging their savings.

Another massive perk is the option for a Roth component. This lets you make after-tax contributions that grow and can be withdrawn completely tax-free in retirement. That's a huge win if you think you'll be in a higher tax bracket down the road.

The SIMPLE IRA For Small Teams

What happens when your one-person show grows into a small team? The SEP IRA and Solo 401(k) are off the table. That’s where the Savings Incentive Match Plan for Employees (SIMPLE) IRA steps in. It’s designed for small businesses with up to 100 employees.

A SIMPLE IRA works a lot like a traditional 401(k). Your employees can choose to contribute, and you, as the employer, are required to chip in, too.

You have two options for the employer match:

- Dollar-for-dollar match: Match employee contributions up to 3% of their pay.

- Non-elective contribution: Contribute a flat 2% for each eligible employee, even if they don’t contribute themselves.

The limits are lower than other plans, but it's a fantastic, straightforward way to offer a retirement benefit that helps you attract and keep good people as you grow.

Don't Forget the IRA Basics

No matter which business plan you pick, you can almost always contribute to a Traditional or Roth IRA, too. These have lower limits—$7,000 in 2024, or $8,000 if you're 50 or over—but they’re an easy and accessible place to start.

A Roth IRA is especially powerful. You contribute with after-tax money, so your qualified withdrawals in retirement are 100% tax-free. For a young entrepreneur whose income is still low, funding a Roth can be an incredibly smart long-term play.

Comparing Self-Employed Retirement Plans

Choosing how to save for retirement when you're self-employed really boils down to your personal situation. This table breaks down the options side-by-side to make it a little clearer.

| Account Type | Annual Contribution Limit | Best For | Key Feature |

|---|---|---|---|

| SEP IRA | Up to 25% of net earnings, max $69,000 (2024) | Freelancers & sole proprietors with fluctuating income. | Flexible, contribution amounts can vary each year. |

| Solo 401(k) | Up to $69,000 (2024) through employee/employer contributions. | High-earning sole proprietors with no employees. | Highest potential savings and option for a Roth component. |

| SIMPLE IRA | $16,000 (2024) for employees, plus employer match. | Small businesses with up to 100 employees. | Easy way to offer a retirement benefit to a team. |

| Traditional/Roth IRA | $7,000 (2024) | Everyone, especially those just starting out. | Accessible and offers tax-free growth (Roth). |

At the end of the day, the best plan is the one you actually open and start funding. Take a hard look at your income, your business structure, and your goals for the future. Making an informed choice now will put you on the path to a secure and comfortable retirement.

Creating a Savings Plan for Fluctuating Income

The feast-or-famine cycle is one of the biggest headaches of self-employment. One month, you’re flush with cash from a huge project; the next, you’re chasing down invoices and watching your bank balance shrink. That kind of unpredictability can make consistent retirement saving feel like a pipe dream.

The numbers back this up. A 2025 survey showed that only 21% of self-employed Americans contribute regularly to retirement. Most others save when they can, if at all, because a variable income makes it tough to commit to a fixed amount. You can dig into the full research on these retirement saving habits on pensionbee.com.

The key isn't more willpower; it's a better system. You need a savings plan that works with your income swings, not against them. This means ditching the old habit of saving whatever is "left over" and building a structure that automatically funnels money toward your future.

Embrace the Profit First Model for Retirement

One of the smartest moves you can make is to adapt the "Profit First" method for your retirement. The idea is simple but incredibly powerful: pay your future self first, every single time you get paid. Before that money even hits your personal account where it can get eaten up by bills, a piece of it goes straight to your retirement fund.

This approach completely flips the traditional savings script. Instead of saving what’s left after spending, you spend what’s left after saving.

Here’s how to put it into action:

- Pick a Percentage: Decide on a slice of every payment to save for retirement. Start with something you know you can handle, like 5% or 10%. You can always bump it up later.

- Build a System: Set up an automatic transfer. The moment a client payment lands in your business account, your chosen percentage gets whisked away to your SEP IRA or Solo 401(k).

- Treat It Like a Tax: Think of this as a non-negotiable "future you" tax. It’s just another cost of doing business, like your software or internet bill.

By automating everything, you take emotion and decision-making out of the picture. The savings just happen, making sure you’re always making progress, whether it’s from a $5,000 project fee or a $500 retainer.

Implement a Variable Contribution Strategy

While the Profit First model creates a steady baseline, a variable contribution strategy lets you take full advantage of your high-income months. This system prepares you for the lean times by letting you save more aggressively when business is good. The goal is simple: over-save during the peaks to build a buffer.

This two-pronged approach—a baseline percentage on every payment plus aggressive saving in good times—is how you build a bulletproof retirement plan on a fluctuating income.

Think of it like a squirrel stuffing its cheeks with acorns before winter hits. When you have a month where your income is 50% higher than average, that’s your cue to contribute more. You can structure this in a few ways.

Setting Your Contribution Tiers

Create a simple tier system based on your monthly revenue. This takes the guesswork out and gives you a clear plan.

| Monthly Revenue | Retirement Contribution | Action to Take |

|---|---|---|

| Below $4,000 | 5% of gross income | Maintain baseline savings. |

| $4,000 – $8,000 | 10% of gross income | Stick to your standard contribution rate. |

| Above $8,000 | 15% of gross income + 25% of everything over $8k | Accelerate savings during a high-earning month. |

This tiered model gives you a framework that adapts your savings to your real-time financial situation.

Of course, it's also critical to protect the source of that income in the first place. An unexpected illness or injury can derail even the best plans. It’s wise to explore your options for disability insurance for self employed professionals to make sure your ability to earn—and save—is secure. By combining a proactive savings system with a solid safety net, you create a truly resilient financial plan.

Using Tax Deductions To Boost Your Savings

Your retirement account is more than just a savings vehicle; it's one of the most powerful tax-slashing tools you have as a self-employed professional.

When you learn how to use it right, you can save a ton on your tax bill today and free up more cash to invest for tomorrow. This isn't just a smart move—it’s a core strategy for anyone serious about building wealth on their own terms.

The real magic happens when you understand the difference between contributing pre-tax versus post-tax dollars. When you put money into a traditional SEP IRA or Solo 401(k), you’re using pre-tax funds. This means every dollar you contribute lowers your taxable income for the year, giving you an immediate tax break.

On the flip side, Roth contributions—available in a Solo 401(k) or a separate Roth IRA—are made with post-tax money. You don’t get a deduction now, but your qualified withdrawals in retirement are 100% tax-free.

A Real-World Tax Savings Example

Let's make this real. Imagine you're a freelance photographer with a net business income of $80,000 for the year. Business is good, but you can already feel that tax bill looming.

So, you decide to contribute $15,000 to your SEP IRA before the tax deadline. That contribution comes right off the top of your income.

- Income Before Contribution: $80,000

- Retirement Contribution: -$15,000

- Adjusted Gross Income (AGI): $65,000

With that one move, you just dropped your taxable income by $15,000. If you're in the 22% federal tax bracket, that could translate to $3,300 in direct tax savings. That’s cash that stays in your pocket instead of going to the IRS.

This isn't just a saving; it's a strategic investment. The tax savings you realize today can be reinvested back into your business or used to make an even larger contribution for the following year, creating a powerful savings cycle.

The Ripple Effect Of Lowering Your AGI

The benefits don't stop there. Lowering your Adjusted Gross Income (AGI) creates a positive domino effect across your entire financial life.

A lower AGI might suddenly make you eligible for other valuable tax credits and deductions you would have otherwise missed. A perfect example is the Saver's Credit, which is designed to help low-to-moderate-income taxpayers save for retirement. Your contribution could drop your income into the right range to claim it.

Plus, a lower AGI can impact other areas of your finances, like student loan payment calculations or eligibility for certain subsidies. Managing your AGI is a key financial lever, and your retirement contributions are the best way to pull it. For a wider view, exploring essential small business tax tips can give you even more ideas.

And don't forget, other deductions work alongside your retirement savings. Understanding the self-employed health insurance deduction, for instance, is another fantastic way to reduce your taxable income. Stacking these strategies ensures you're building wealth efficiently from every angle.

Advanced Strategies to Accelerate Your Retirement

Once you've got your core retirement plan set up and the contributions are automated, it's time to start thinking bigger. For the ambitious business owner, simply meeting the basics isn't enough. The real magic happens when you move beyond them to truly supercharge your journey to financial freedom.

These strategies are all about optimizing every tool you have to build wealth faster and smarter. It's not just about saving more; it's about making your savings work harder by using accounts and rules that many people completely overlook.

By layering these tactics onto your SEP IRA or Solo 401(k), you can build a financial engine that's far more powerful.

Unleash the Power of a Health Savings Account

One of the most underrated retirement tools isn't even a retirement account—it's a Health Savings Account (HSA). If you have a high-deductible health plan, an HSA offers a rare triple tax advantage that no other account can match. Seriously.

Here’s why it’s so powerful:

- Tax-deductible contributions: The money you put in lowers your taxable income for the year, just like a traditional IRA.

- Tax-free growth: You can invest your HSA funds, and any growth is completely tax-free.

- Tax-free withdrawals: As long as you use the money for qualified medical expenses, it comes out 100% tax-free, now and in retirement.

And here’s the kicker: after you turn 65, an HSA basically acts like a traditional IRA. You can pull money out for any reason, and you'll just pay regular income tax on it. But if you use it for medical costs, it stays totally tax-free.

Combine Pre-Tax and Post-Tax with a Roth Solo 401(k)

For high-earning entrepreneurs, the Solo 401(k) has a killer feature: the ability to add a Roth component. This gives you the best of both worlds in a single, streamlined plan.

You can make traditional, pre-tax "employer" contributions to get a tax deduction today, while also making post-tax Roth "employee" contributions for a tax-free future.

This strategy gives you incredible tax diversification when you finally retire. You'll have a pool of tax-free money (your Roth funds) ready to go, giving you the flexibility to manage your taxable income and keep your tax bill low in your later years.

This dual approach is perfect for the business owner who wants an immediate tax break but also wants to lock in tax-free growth, hedging against the possibility of higher tax rates down the road.

Executing the Backdoor Roth IRA

What happens when your income gets too high to contribute to a Roth IRA directly? Don't worry, there's a well-known workaround: the Backdoor Roth IRA. This simple move allows high-income earners to sidestep the usual income limits.

The process is surprisingly straightforward:

- First, you contribute to a non-deductible Traditional IRA.

- Then, shortly after, you convert those funds into a Roth IRA.

- You'll owe income tax on any earnings that pop up between the contribution and the conversion, but if you do it quickly, that amount is usually tiny.

This maneuver gets your money into a Roth account where it can grow and eventually be withdrawn tax-free in retirement, no matter how much you earn. It’s a key strategy for self-employed pros whose success might otherwise lock them out of this incredibly valuable account.

As you plan for an independent future, it’s also important to consider how all your assets fit together. Learning about different types of insurance for early retirement can help you build a complete financial safety net.

Got Questions About Freelance Retirement? We've Got Answers.

Jumping into retirement savings is a massive win. But once you start, a whole new set of questions usually pops up. Your business isn't static, and neither is your financial life. Let's tackle some of the most common hurdles freelancers face head-on.

It's completely normal to feel a bit lost in the details. The trick is to find clear answers so you can keep building your future with confidence.

"My Business Isn't Profitable Yet. Can I Still Contribute?"

This is probably the number one question for new entrepreneurs, and it’s a great one. The short answer is: it depends on the account.

For plans like a SEP IRA or a Solo 401(k), your contributions are tied directly to your net adjusted self-employment income. If your business ends the year with a net loss, you technically can't contribute to these specific plans for that year.

But don't panic—that doesn't mean you're out of the game. If you have other earned income (maybe from a part-time gig or a few side projects), you can absolutely still put money into a Traditional or Roth IRA. Every dollar counts, especially in those early building years.

"What If I Go Back to a 9-to-5 Job?"

Life happens. Maybe you'll take a W-2 job for a while. The great news is your self-employed retirement accounts are 100% yours. That money stays put and keeps growing for you.

You won't be able to contribute your W-2 salary to your Solo 401(k) or SEP IRA anymore, but you can easily move the funds.

- Solo 401(k): You can often roll this right into your new employer's 401(k) or into an IRA.

- SEP IRA: This can be seamlessly rolled over into a Traditional IRA.

Of course, you can also just leave the funds where they are. But consolidating everything into one or two accounts usually makes life a lot simpler.

No matter where your career takes you, the money you've saved is yours. A new job just changes how you'll save going forward, not what you've already built.

"How Do Catch-Up Contributions Work?"

Once you hit age 50, the IRS gives you a major perk: the ability to make "catch-up" contributions. It's an incredible tool for supercharging your savings as you get closer to retirement.

Here’s a quick breakdown of how it works for different accounts:

- Solo 401(k) & SIMPLE IRA: These plans allow for a specific, extra dollar amount you can contribute as an "employee."

- SEP IRA: There aren't separate catch-up rules here, mainly because the contribution limit is already a generous percentage of your income.

- Traditional or Roth IRA: You can add an extra $1,000 a year (as of 2024).

If you started saving a bit later in life or just want to give your nest egg a final push, these extra contributions are a game-changer. It's a key part of mastering how to save for retirement when you're self-employed and in the home stretch of your career.

Navigating insurance and retirement can be complex, but you don't have to do it alone. My Policy Quote is here to help you find the right coverage to protect your financial future. Explore your options today at mypolicyquote.com.