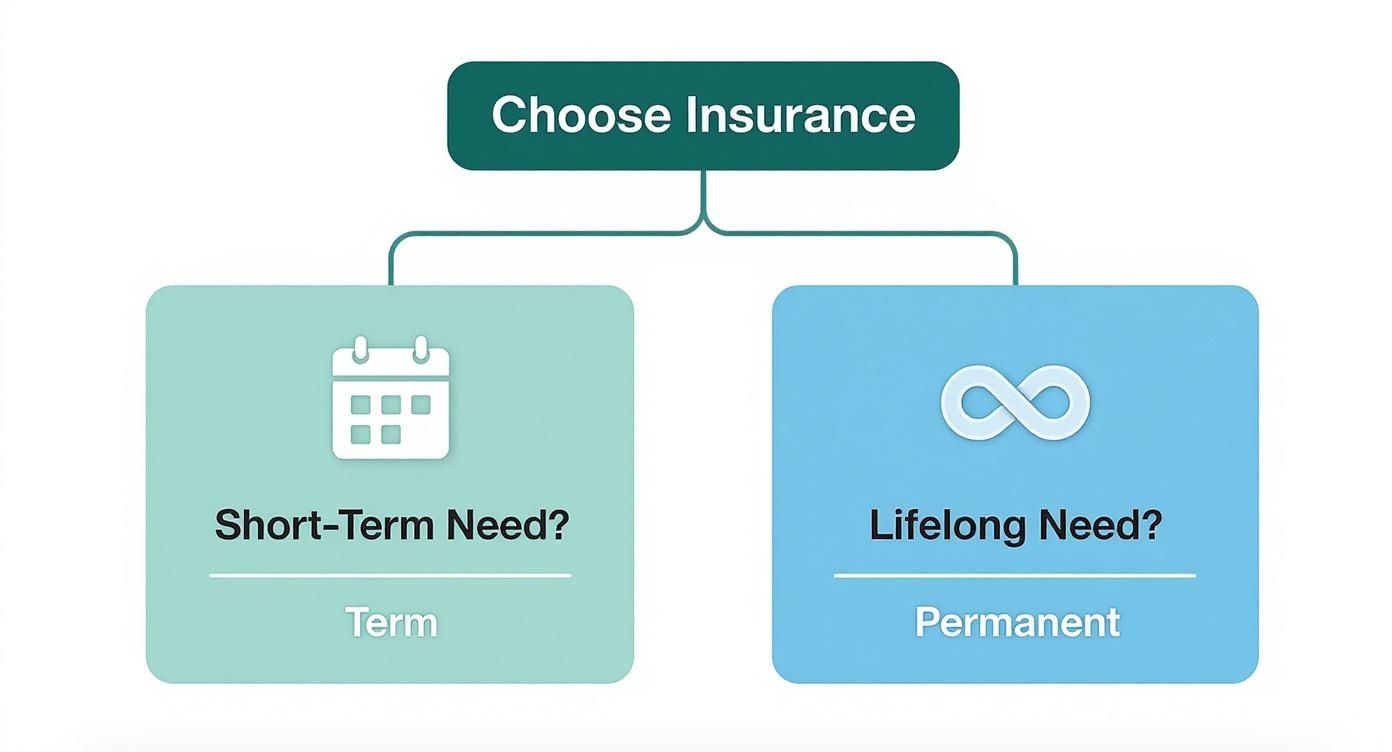

Diving into the world of life insurance can feel like learning a new language, but it really boils down to one simple question. Do you need protection for a specific time, or for your entire life?

That’s it. Every policy out there falls into one of two buckets: Term Life (temporary coverage) or Permanent Life (lifelong coverage). The easiest way to think about it is like renting versus buying a home for your family's financial security.

Your Foundational Guide to Life Insurance Choices

Choosing life insurance is a big decision, but it doesn’t have to be a confusing one. At its heart, the goal is straightforward: to create a financial safety net for the people you love if you’re no longer around to provide for them. While every policy shares that purpose, they get there in different ways.

Let’s go back to our home analogy.

Term life insurance is like renting an apartment. You get protection for a fixed period—maybe 10, 20, or 30 years—at a very affordable price. It’s perfect for covering big, temporary responsibilities, like a mortgage or the years you're raising your kids. But once the term is up, the coverage ends, just like a lease.

Permanent life insurance, on the other hand, is like buying a home. It's a lifelong commitment that does more than just provide a death benefit. It also builds equity over time through a feature called "cash value." It costs more, but you get lasting security and an asset that grows with you.

Life Insurance At a Glance Renting vs Owning Protection

To make it even clearer, here’s a quick breakdown of how these two approaches stack up. This table will help you see the core differences side-by-side.

| Feature | Term Life (Like Renting) | Permanent Life (Like Owning) |

|---|---|---|

| Coverage Duration | For a specific period (e.g., 20 years) | Your entire lifetime |

| Cost | Lower monthly premiums | Higher monthly premiums |

| Main Purpose | Covers temporary needs like a mortgage or raising kids | Provides lifelong protection and builds wealth |

| Cash Value | No | Yes, builds a tax-deferred savings component |

| Flexibility | Simple and straightforward | More complex, with investment options |

Seeing it laid out like this really simplifies things. You're either choosing temporary, affordable protection or you're investing in a permanent asset that lasts a lifetime.

Think of it this way: the "renting vs. owning" idea is your compass for navigating life insurance. It cuts through the jargon and helps you focus on what truly matters for your family—affordable protection for now, or permanent security for the future.

This guide will walk you through both paths, breaking down the pros and cons of each policy type. With this foundation, you’ll be ready to confidently compare your options and make the right choice.

Understanding Term Life Insurance: The Temporary Shield

If life insurance were a car, term life would be the lease. It’s a clean, simple, and incredibly affordable way to get protection for a specific window of time. You pay for what you need, for as long as you need it, without the heavier financial commitment of “owning” a policy for life.

Term life insurance is designed to provide a financial safety net for a set period—usually 10, 20, or 30 years. If you pass away during that term, your family receives a tax-free payout. If you outlive it, the policy simply ends. No payout, no strings attached. You can walk away, renew your coverage, or even convert it to a permanent policy.

Its main job is to shield your family’s finances during your peak earning years. Think of it as a financial bodyguard while you’re paying down a mortgage, raising kids, and building a retirement nest egg.

The Different Kinds of Term Policies

Not all term policies are built the same. They come in a few different flavors, each designed to tackle a different kind of financial goal. Getting to know the differences is the key to finding the right fit.

Here are the most common types of term life insurance you’ll run into:

- Level Term: This is the one most people choose, and for good reason. Both your monthly payment (the premium) and the death benefit stay the same for the entire term. That predictability makes it perfect for replacing your income or covering big, long-term debts like a 30-year mortgage.

- Decreasing Term: With this policy, the death benefit shrinks over time, typically year by year, while the premium stays put. It’s often lined up with a specific debt that’s also getting smaller, like a mortgage or a business loan. As you pay down the debt, your need for coverage drops with it.

- Annual Renewable Term (ART): This is short-term coverage, literally one year at a time. You have the option to renew it each year without needing a new medical exam. The catch? While it’s super cheap at first, the premium goes up every time you renew. ART is best for temporary situations, like bridging a coverage gap between jobs.

For many people, especially young families, term life insurance is the perfect starting point. It offers the biggest bang for your buck—the highest amount of coverage for the lowest initial cost.

Pros and Cons of Term Life Insurance

So, is term life the right move for you? To figure that out, you have to look at both sides of the coin. This balanced view will help you see if this "renting" approach to protection lines up with your life right now.

Advantages of Term Life:

- Affordability: It’s way less expensive than permanent life insurance. This means you can afford a much larger death benefit for a fraction of the cost.

- Simplicity: These policies are refreshingly straightforward. You pick a term, choose a coverage amount, pay your premiums, and you’re done. Your family is protected.

- Flexibility: You can match the policy’s term length to your biggest financial responsibilities. Need coverage until the mortgage is paid off or the kids are out of college? A 20- or 30-year term has you covered.

Disadvantages of Term Life:

- No Cash Value: This is a big one. Unlike permanent policies, term life has no savings or investment component. It’s pure protection, which means you can’t build equity or borrow against it.

- Coverage Expires: If you outlive your policy, the coverage just stops. You don’t get any of your premiums back. And if you want to get a new policy when you're older, it will be significantly more expensive.

- Temporary Solution: It’s designed to solve a temporary problem. If you need coverage that will last your entire life—for things like estate planning or leaving an inheritance—term life might not be enough on its own.

Ultimately, term life insurance is a powerful and budget-friendly tool for protecting what matters most during your most critical financial years. To see how different policies stack up, a detailed term life insurance comparison can give you a clearer picture of costs and features from top providers.

Exploring Whole Life Insurance: Lifelong Security and Growth

If term life insurance is like renting protection, then whole life is like buying a home for your family's financial future. It’s the original, classic form of permanent coverage, built to last your entire life while building real, tangible value along the way.

Think of it like a fixed-rate mortgage. You lock in a predictable premium that will never, ever go up—no matter how old you get or if your health changes. A piece of that payment guarantees the death benefit, while another piece builds "equity" in your policy. We call this the cash value.

This two-in-one structure delivers a powerful combination of lifelong security and steady, tax-deferred growth, making it a true cornerstone for long-term financial planning.

The Three Guarantees of Whole Life

What really sets whole life apart is its foundation of guarantees. This predictability brings incredible peace of mind because you know exactly what to expect from your policy from the day you sign up. These core promises take all the guesswork out of the equation.

- A Guaranteed Death Benefit: As long as you pay your premiums, the payout your loved ones receive is locked in. It will never decrease.

- Guaranteed Fixed Premiums: Your payment is set in stone when you buy the policy and stays the same for life. A 35-year-old will pay the exact same premium at age 75.

- A Guaranteed Rate of Return: The cash value is guaranteed to grow at a minimum fixed interest rate set by the insurer, ensuring slow but incredibly steady accumulation.

This triple-guarantee structure makes whole life one of the most stable and reliable financial tools you can find for legacy planning and wealth transfer.

The real appeal of whole life insurance is its unwavering predictability. In a world full of financial ups and downs, it offers a guaranteed outcome for your loved ones and a secure way to build a financial asset over your lifetime.

Understanding Dividends: The Non-Guaranteed Bonus

On top of all its guarantees, many whole life policies from mutual insurance companies offer the potential to earn dividends. Now, these aren't like stock dividends. Instead, think of them as a refund or a return of a portion of the company's profits back to you, the policyholder.

While dividends aren't guaranteed, many well-established insurers have a track record of paying them out consistently for decades, sometimes even over a century. When you receive a dividend, you've got options:

- Take it in Cash: Get a check mailed directly to you.

- Reduce Your Premiums: Use the dividend to lower what you pay out-of-pocket.

- Earn Interest: Let it sit with the insurer to collect interest in a separate account.

- Buy Paid-Up Additions: This is the big one. You can use the dividend to purchase small, fully paid-up blocks of additional permanent life insurance. This move increases both your death benefit and your future cash value growth.

Choosing to buy paid-up additions is often the most powerful way to supercharge your policy, as it compounds its value over time. When you start exploring the best whole life insurance policies, a company's dividend-paying history is definitely something you'll want to look at.

Weighing the Pros and Cons

Whole life is a powerful tool, but its higher cost means it isn't the right fit for absolutely everyone. The U.S. life insurance market saw slow premium growth for years, but the pandemic sparked a huge surge in demand. In 2021, sales hit highs we hadn't seen in over 40 years. Looking ahead, LIMRA projects premium income will reach $15.9 billion in the coming year, driven by both term and whole life products. You can read more about these life insurance market trends on LIMRA.com.

Advantages of Whole Life:

- Lifelong Coverage: The policy never expires as long as you pay your premiums. Peace of mind for life.

- Predictable Costs: Fixed premiums make budgeting simple and straightforward for decades to come.

- Guaranteed Cash Value Growth: It provides a safe, conservative, tax-deferred way to build savings you can access later in life.

Disadvantages of Whole Life:

- Higher Premiums: It is significantly more expensive than term life for the same amount of death benefit.

- Lower Initial Returns: The cash value grows very slowly, especially in the first several years of the policy.

- Less Flexibility: Unlike other types of permanent insurance, you can’t typically adjust your premiums or death benefit.

Universal Life Insurance: Flexible Protection for a Changing Life

If whole life insurance feels like a predictable, fixed-rate mortgage, think of Universal Life (UL) insurance as a financial toolkit. It's permanent coverage built for one main purpose: flexibility. This makes it an incredibly powerful option for anyone whose financial journey has more twists and turns than a straight road.

At its core, a UL policy separates the three main components of life insurance—the death benefit, the savings (cash value), and the costs. This design gives you the freedom to adjust your premium payments and even your death benefit as your life evolves.

Imagine you're a small business owner who just had a fantastic year. With a UL policy, you could pay more into it, beefing up your cash value. If next year is a bit leaner, you could potentially lower your payments—or even skip one—by letting the cash value you’ve built up cover the policy’s costs.

How Does Universal Life Actually Work?

It’s simpler than it sounds. Every premium you pay goes into your policy’s cash value account. Then, each month, the insurance company simply deducts the cost of insurance and any administrative fees.

Whatever’s left over earns interest, allowing your cash value to grow. That flexibility is the biggest draw, but it also means you have to stay on top of it. If the cash value gets too low to cover the monthly costs, your policy could be in danger of lapsing.

Universal life insurance is built for people who want permanent coverage but know life isn't always predictable. It’s for those who are comfortable taking a more hands-on role in managing their policy.

The Different Flavors of Universal Life

The name "Universal Life" is actually an umbrella for a few different types of policies. Each one handles cash value growth a little differently, and understanding the nuances is key when you're trying to figure out the different types of life insurance explained by people who know.

Here are the main ones you'll run into:

- Guaranteed Universal Life (GUL): This is the most straightforward version. GUL is all about giving you a guaranteed death benefit that lasts your entire life, plain and simple. It doesn’t focus on cash value growth, making it feel more like a "term-for-life" policy with costs that are locked in.

- Indexed Universal Life (IUL): A very popular option. An IUL policy links your cash value growth to a stock market index, like the S&P 500. Your gains are usually capped, but the real benefit is the built-in protection: you have a "floor" (often 0%) that prevents you from losing money in a down market.

- Variable Universal Life (VUL): This is the most hands-on type. VUL lets you invest your cash value directly into sub-accounts that work like mutual funds. It offers the highest potential for growth, but it also comes with real risk—you could lose money if your investments don't perform well.

Is Universal Life the Right Choice for You?

UL's adaptability makes it a great tool, but it's definitely not a one-size-fits-all solution. The life insurance sector is massive, with global premium income hitting around EUR 2,902 billion, making it the largest segment of the insurance market. The market saw a recent growth spurt of 10.4%, with North America jumping 14.4%, thanks in large part to demand for flexible products. This trend, highlighted in a global insurance market analysis from Allianz.com, shows just how much people need options that fit their unique lives.

Universal Life might be a great fit if:

- Your income isn't always the same. If you're a freelancer, a salesperson on commission, or a business owner, the ability to adjust your premiums is a game-changer.

- You want more growth potential. IUL and VUL policies give you a shot at much higher returns on your cash value than the slow-and-steady rate you get with whole life.

- You know your coverage needs will change. Once the kids are grown or the mortgage is paid off, you might want to lower your death benefit to reduce your costs. UL lets you do that.

The biggest thing to remember, though, is the risk. Because the premiums are flexible and the returns aren't always guaranteed, you have to actively monitor your policy. If you don't manage it properly, a UL policy can fall short of its promise.

Comparing the Major Life Insurance Types

Knowing the individual types of life insurance is a great start. But the real "aha!" moment comes when you put them side-by-side. Seeing them compared directly helps you grasp the trade-offs and turn abstract concepts into a practical decision-making tool.

Remember, there's no single "best" policy for everyone. It’s all about finding the best fit for your life, right now. Your age, your financial goals, and who you’re protecting will all point you toward the right choice.

Term vs Whole vs Universal A Detailed Feature Comparison

So, how do the big three really stack up? Let's break down their core features—how long they last, what they cost, whether they build value, and how much control you have over them. This at-a-glance comparison makes the differences crystal clear.

| Feature | Term Life | Whole Life | Universal Life |

|---|---|---|---|

| Coverage Duration | Temporary (e.g., 10, 20, 30 years) | Lifelong, as long as premiums are paid | Lifelong, as long as premiums are paid |

| Typical Cost | Lowest premiums | Highest, but fixed and predictable | Varies; often less than whole life |

| Cash Value | No | Yes, with a guaranteed growth rate | Yes, with variable interest rates |

| Flexibility | Very little; set and forget | Low; premiums and benefits are fixed | High; can adjust premiums & death benefit |

As you can see, there’s a fundamental trade-off. Term life offers maximum protection for the lowest cost, but it’s temporary and doesn't build any savings. On the other hand, permanent policies like Whole and Universal Life give you lifelong coverage and grow cash value, but you'll pay a significantly higher price for those benefits.

Want to dive deeper into this key distinction? You can learn more about the difference between term and permanent life insurance in our detailed guide.

Putting It into Practice Real World Scenarios

Let's see how these policies play out in the real world. The right choice often clicks into place when you connect a policy’s features to an actual financial need.

-

The New Homeowner: A couple, both 30 years old, just bought their first house with a 30-year mortgage. Their number one worry? Making sure their partner could pay off the house if one of them were to pass away unexpectedly. For them, Term life insurance is the perfect fit. A 30-year term policy gives them a large, affordable death benefit that perfectly matches the timeline of their biggest debt.

-

The Established Professional: A 50-year-old business owner wants to leave a tax-free inheritance for her kids and cover potential estate taxes. She values predictability and guarantees above all else. Whole life insurance is a strong contender. Its fixed premiums, guaranteed death benefit, and steady cash value growth deliver the stability she needs for her long-term estate plan.

-

The Freelancer with a Fluctuating Income: A 40-year-old graphic designer has an income that varies from month to month. He needs lifelong coverage but wants the ability to pay more in good years and scale back in leaner ones. Universal life insurance offers the ideal solution. Its premium flexibility allows him to adjust payments to match his cash flow without risking his coverage.

This simple decision tree can help you see the choice more clearly.

Ultimately, the core question is this: does your financial need have an expiration date? If the answer is yes, term life is often the simplest and most affordable answer. If it's a lifelong need, a permanent policy is likely the better tool for the job.

How to Choose the Right Life Insurance Policy for You

Okay, you’ve learned about the different kinds of life insurance out there. That's the first step. Now, let’s get personal.

Choosing a policy isn't about picking the "best" one on the market. It’s about finding the right fit for your life, your budget, and your family. It’s a decision that should feel right.

The whole process starts with a bit of self-reflection. By answering a few simple questions, you can create a clear roadmap that points you straight to the coverage you actually need. No complicated formulas, just an honest look at your world.

Define Your Financial Responsibilities

First things first: what (and who) are you trying to protect? Think of life insurance as a financial stand-in for you when you're gone. The policy needs to be big enough to cover the promises you've made.

Start by listing your financial responsibilities:

- Income Replacement: How many years of your salary would your family need to live comfortably and maintain their lifestyle?

- Mortgage or Rent: Do you want to make sure the house is paid off or that rent is covered for a long time?

- Other Debts: Don't forget about car loans, student loans, or credit card balances that would otherwise fall on your loved ones.

- Future Education: Are you planning to help with college tuition for your kids or grandkids?

The goal here is to create a financial safety net that is custom-fit to your family's needs. It's about ensuring that your financial goals for them can still be achieved, even in your absence.

Match the Policy to Your Timeline

Next, ask yourself this critical question: how long will these financial responsibilities last? Your answer is the key to deciding between a temporary plan (Term) and a lifelong one (Permanent).

If your main goal is to protect your family until the kids are grown and the mortgage is paid off, a 20- or 30-year term policy is usually the most affordable and sensible option. It’s designed for that specific chapter of life.

But if you have bigger, lifelong goals—like funding care for a special-needs child or leaving a guaranteed inheritance—a permanent policy like whole or universal life makes a lot more sense. Getting an accurate estimate is crucial, and using a detailed life insurance needs calculator can give you a solid starting point for how much coverage to get.

Assess Your Budget and Long-Term Goals

Of course, your budget plays a huge role. Term life insurance offers the biggest death benefit for the lowest premium, which makes it a great choice for almost anyone.

Permanent policies are a bigger financial commitment, but they come with a powerful bonus: they build cash value. This is a living benefit you can actually borrow from or use later in life.

If you have some room in your budget and like the idea of a policy that doubles as a financial asset, a permanent option could be a fantastic fit. And for those with more complex financial situations, understanding tools like a life insurance trust can be a game-changer for estate planning and protecting your legacy.

By carefully weighing your immediate needs against your long-term goals, you can confidently choose a policy that gives you true peace of mind.

Still Have Questions About Life Insurance? Let’s Clear Them Up

Even after walking through the different types of life insurance, you probably have a few more questions rattling around. That’s perfectly normal. This is a big decision, after all.

Let’s tackle some of the most common questions head-on to help you feel confident as you figure out your next steps.

How Much Life Insurance Coverage Do I Actually Need?

There’s no magic number here, but a good starting point is the 10 to 12 times rule. The idea is to have a policy that’s worth 10 to 12 times your current annual income. For many families, that provides a solid financial cushion to keep life moving forward without a primary earner.

If you want to get more specific, think like an accountant for a moment.

- First, add up all your big financial responsibilities. This means your mortgage, any car loans or credit card debt, and the estimated cost of your kids' college education.

- Next, subtract your existing assets. This includes savings, investments, and any other life insurance you already have.

That final number? It's a pretty solid estimate of the death benefit your family would truly need.

Can I Have More Than One Life Insurance Policy?

Yes, you absolutely can. It’s not only legal but also a pretty smart strategy that many people use. It’s often called “laddering,” and it involves stacking multiple policies to cover different needs at different times in your life, often saving you money in the process.

Here’s a real-world example: You might get a large 20-year term policy to cover the years when your mortgage is high and your kids are still at home. At the same time, you could have a smaller whole life policy that’s designed to stick around forever, just to make sure final expenses are covered and you can leave a little something behind. It’s all about creating the right protection for each chapter of your life.

What Happens If I Outlive My Term Life Policy?

So, you’ve paid your premiums for 20 or 30 years, and the term is up. What now? If you’ve outlived your policy, the coverage simply ends. You stop paying, and the insurance company doesn’t pay out.

Think of it like car insurance. You paid for protection during those years, and thankfully, you never had to use it. That’s a good thing!

But you’re not left without options. Most policies will let you convert your term plan into a permanent one without a new medical exam. You can also renew your term, but be prepared for a much higher price tag since you’re older now. It's always a great idea to look at these options a year or two before your policy is set to expire. And when you’re thinking about what a policy covers, don’t forget the details—for example, it's wise to understand whether life insurance covers natural organic reduction so you can plan for every possibility.

Navigating these choices is so much easier when you have an expert in your corner. At My Policy Quote, we’re here to help you find the perfect policy that fits your family, your life, and your budget.

Explore your personalized life insurance options with us today!