A waiver of premium rider is a powerful add-on for your life insurance policy. Think of it as a financial safety net—it steps in to pay your premiums if you become totally disabled and can’t work.

Essentially, it’s insurance for your insurance. It ensures your life insurance coverage stays active right when you and your family need it most, even if your income suddenly stops. This small feature can prevent a policy from lapsing during a major life crisis.

What Is a Waiver of Premium Rider

Imagine you’ve secured a life insurance policy to protect your family's future. Now, picture suffering a serious illness or injury that leaves you unable to work for months, or even years. How would you keep paying those premiums?

This is the exact problem a waiver of premium rider solves. For a small extra cost, you can add this provision to your policy. If a total disability strikes, the insurance company takes over and covers your premium payments for you.

This rider isn't a separate policy; it’s an enhancement that makes your existing life insurance more resilient. For a deeper dive into how add-ons work, you can explore our guide on what is a rider on life insurance. The goal here is simple: to keep your valuable coverage in force when you’re most vulnerable and least able to afford it.

The Core Function of the Rider

The main job of the waiver of premium rider is straightforward but crucial: it keeps your policy from lapsing. Without it, a long-term disability could force you to choose between paying for insurance and covering basic living costs—an impossible decision.

This rider takes that dilemma off the table. The trigger for this protection is the policy's specific definition of "total disability." Understanding what qualifies for disability benefits is key to seeing how and when the rider kicks in.

Typically, there's a waiting period, often around six months, after the disability begins. Once you’ve met that requirement, the insurance company starts waiving the premiums, making sure your policy remains active without causing you any financial strain.

Waiver of Premium Rider at a Glance

To make it even clearer, let's break down the essential pieces of a waiver of premium rider. While the fine print can vary between insurers, these are the core features you'll almost always find.

This table gives you a quick snapshot of what to expect.

| Feature | Description |

|---|---|

| Purpose | To pay life insurance premiums if the policyholder becomes totally disabled. |

| Eligibility | Usually requires the policyholder to be under a certain age (e.g., 60 or 65) when the disability starts. |

| Waiting Period | A mandatory "elimination period" (typically 6 months) must pass before benefits begin. |

| Definition of Disability | The policy will spell out what "total disability" means—either being unable to do your own job or any job. |

| Benefit Duration | Premiums are generally waived for as long as the disability lasts, often up to a specific age like 65. |

This structure is designed to provide a robust financial backstop for genuine, long-term disabilities, giving you and your loved ones true peace of mind.

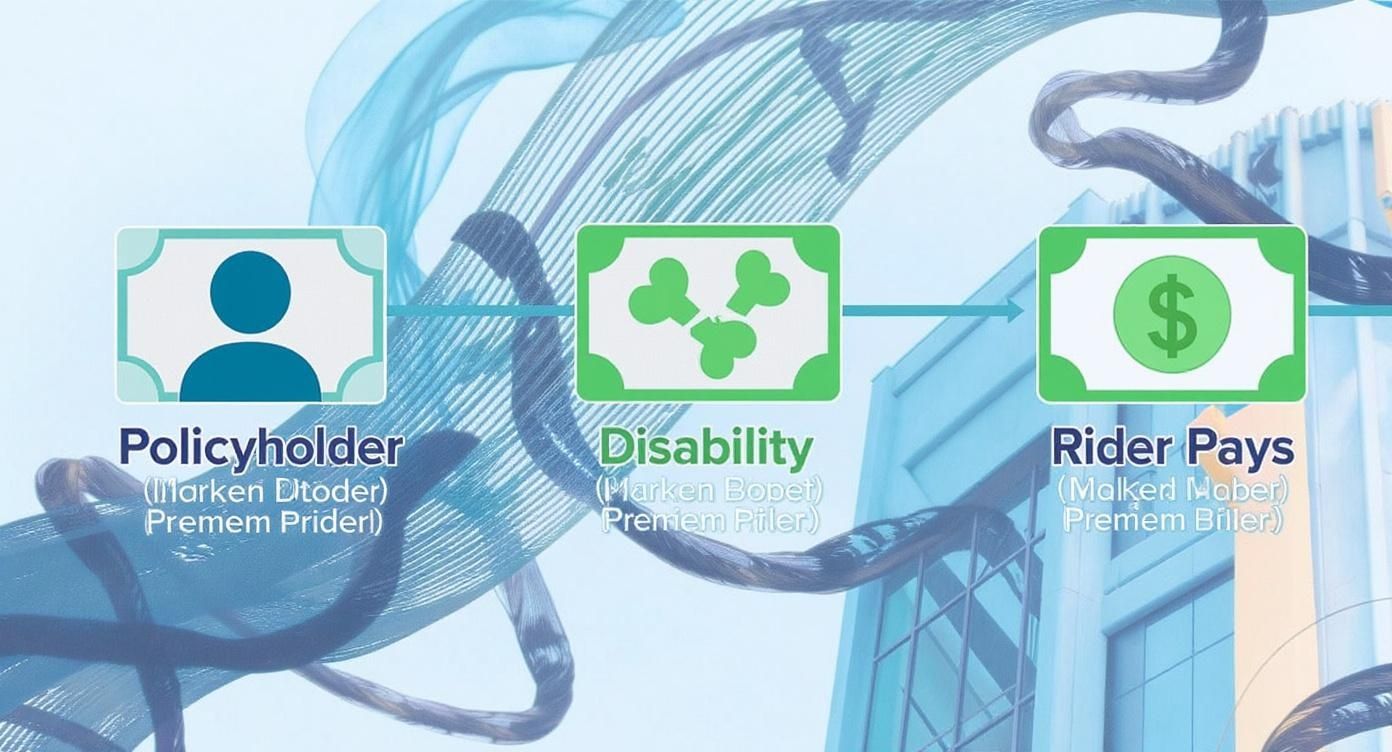

How a Waiver of Premium Rider Actually Works

It’s one thing to know what a waiver of premium rider is, but understanding how it kicks in when you actually need it is what really matters. Think of it like a safety net with a specific set of triggers. One event has to happen before the next, starting with a disability and ending with your policy premiums being paid for you.

Let’s walk through the real-world process, step-by-step, so you know exactly what to expect.

This simple flow shows the journey from being a healthy policyholder to a protected one.

As you can see, a qualifying disability is the key that unlocks the rider, letting it do its job and cover your payments.

Step 1: Navigating the Waiting Period

The very first hurdle after you become disabled is what’s called the elimination period, or waiting period. This is a set amount of time—most commonly six months—that you must wait before the rider’s benefits can start.

You have to be continuously disabled for that entire time. Crucially, you are still responsible for paying your life insurance premiums during this period. If you stop paying, your policy could lapse right before the protection you need kicks in.

Key Takeaway: The waiting period is like a deductible, but measured in time instead of money. It's there to make sure the rider covers serious, long-term disabilities, not temporary illnesses or injuries.

Step 2: Proving Total Disability

While you’re in that waiting period, it's time to start the claims process. You’ll need to officially notify your insurance company and provide solid proof of your disability. The most important detail here is how your policy defines "total disability."

There are two main definitions you'll encounter:

- Own-Occupation: This is usually the better one for you. You’re considered disabled if you can’t perform the main duties of your specific job.

- Any-Occupation: This definition is much stricter. It means you’re only considered disabled if you can’t do any job you’re reasonably suited for based on your education, training, or experience.

To get your claim approved, you'll need to submit thorough medical records. This typically includes statements from your doctor, test results, and any other documentation that proves your condition and how it prevents you from working. This review is a core part of the insurance approval process, and you can learn more by reading about what is underwriting in insurance.

Step 3: Activation and Ongoing Management

Once the waiting period is over and the insurance company approves your claim, they will start waiving your premiums. From that moment on, you can stop making payments, but your life insurance coverage stays active and in full force.

This isn't always a "set it and forget it" situation, though. The insurer will likely ask for proof that you're still disabled from time to time, often once a year. This might just be an updated form from your doctor. Insurers are also finding better ways to manage these claims, with new technologies transforming insurance claims with Agentic AI to make the process smoother.

The premium waivers will eventually stop under a few specific conditions:

- Recovery: If you get better and can go back to work, the waiver ends, and you’ll start paying your premiums again.

- Age Limit: Most riders have an age limit, usually 65. Once you hit that age, the benefit stops, even if you’re still disabled.

- Policy Expiration: If you have a term life policy, the rider naturally ends when your policy's term is over.

Real-World Scenarios and Cost Analysis

Theory is one thing, but seeing how a waiver of premium rider actually works is where its value really clicks. Let's move past the insurance-speak and look at a couple of real-life situations where this rider becomes a financial lifesaver. After that, we’ll get into exactly what it costs.

These stories show how a small addition to your policy can create powerful stability when life throws its biggest challenges your way, protecting your family’s future when you physically can't.

Example 1: The Self-Employed Contractor

Meet David. He’s a 42-year-old self-employed electrician and the sole provider for his family. If he can’t work, the income stops. He has a $750,000 term life policy, which costs him $65 a month. Knowing his job is physically risky, he added a waiver of premium rider for an extra $10 per month.

One afternoon, a fall on a job site leads to a severe back injury. He needs surgery and faces a long, painful recovery. His doctor is clear: he won't be able to work for at least a year. Just like that, his income is gone, and the family starts burning through their savings.

This is where his rider kicks in:

- The Waiting Period: For the first six months, David still has to pay the $75 monthly premium from his savings. This is the standard elimination period.

- Claim Approval: He sends his doctor's reports and medical records to the insurance company, and his claim gets approved.

- Premiums Waived: After those six months, the insurance company starts covering his $75 premium. For the next ten months of his recovery, he pays absolutely nothing, saving his family $750.

But the real win? His $750,000 life insurance policy stays active. That $120 he spent on the rider that year suddenly became the best investment he ever made. It kept his family’s safety net intact and gave them priceless peace of mind.

Example 2: The Young Parent with a Critical Illness

Now, let’s look at Sarah, a 35-year-old marketing manager with two young kids. She has a $500,000 whole life policy to make sure her children will always be provided for. Her premium is $180 per month, plus another $15 for the waiver of premium rider.

At 38, she gets a devastating diagnosis: a serious autoimmune disease that makes it impossible for her to keep working. Once the initial shock wears off, she remembers the rider and files a claim.

The rider activates after her six-month waiting period, and the insurer starts waiving her $195 monthly premium. Over the next five years of her disability, this saves her family a staggering $11,700 in payments. All the while, her policy's cash value keeps growing. This took a massive financial weight off her shoulders, letting her focus on her health and her family.

Analyzing the Cost of a Waiver of Premium Rider

So, how much does this kind of protection actually set you back? It's almost always a very affordable add-on. The cost is all about the insurance company's risk of you becoming disabled.

Here are the main things that influence the price:

- Your Age: The younger you are when you get the policy, the cheaper the rider will be.

- Your Health: If you have pre-existing conditions, the cost will likely be higher. In some cases, the rider might not be offered.

- Your Occupation: A construction worker will pay more for this rider than an accountant. It’s all about the on-the-job risk.

- The Policy's Death Benefit: A bigger policy means a bigger premium to waive, so the rider will naturally cost a bit more.

Let’s put some numbers to it. A healthy, non-smoking 40-year-old with a low-risk office job might have a $500,000, 20-year term policy for about $40 a month. Adding a waiver of premium rider could be as little as $5 to $10 extra per month.

If you want to dive deeper into how base policy premiums are set, our guide on the costs of term life insurance is a great resource.

When it comes down to it, you’re paying a small amount—often just a few dollars a month—to protect your entire life insurance investment. Compare that tiny cost to the massive relief of having your premiums covered during a disability, and it's easy to see why it's worth it.

Weighing the Pros and Cons of This Rider

Adding any rider to your life insurance policy is a decision that deserves some real thought. The waiver of premium rider offers a powerful safety net, but it’s not for everyone. To make the right call, you need to look at both sides of the coin—the massive benefits it provides versus its potential drawbacks and costs.

This balanced view will help you figure out if this extra layer of protection truly aligns with your financial strategy and personal needs. Let's break down the good and the bad so you can weigh them for yourself.

The Advantages of Adding This Rider

The biggest benefit here is the profound peace of mind it brings. Just knowing your life insurance is secure, even if you lose your ability to earn an income, removes a huge source of stress during an already difficult time.

This rider is a direct shield for your long-term financial plan. A serious disability can derail savings goals, retirement plans, and family budgets in an instant. By making sure your life insurance doesn't lapse, you keep the cornerstone of your family's financial security right where it needs to be.

It also takes an impossible choice off the table. Imagine facing mounting medical bills and a total loss of income, then having to decide between paying your life insurance or covering groceries. It’s a dreadful scenario. This rider makes sure you never have to face it.

The Ultimate Safety Net: Think of the waiver of premium rider as insurance for your insurance. For a relatively small cost, it protects a much larger asset—your death benefit—ensuring your family's future stays secure no matter what happens to your health.

The Disadvantages and Limitations to Consider

Of course, this kind of protection isn't free. The most obvious drawback is the additional cost. While it's usually modest, the rider adds to your premium every single month or year, and it’s a cost for a benefit you hope you never have to use.

Another major hurdle can be the strict definition of "total disability." Insurance companies don't take this term lightly. Qualifying often requires stacks of medical proof showing you meet the very specific criteria in your policy. This can be a challenging and long process, especially for certain conditions.

The waiting period is another big one. You typically have to stay disabled for six months before the waiver even kicks in, and you’re on the hook for paying premiums that whole time. This delay means it offers no immediate financial relief and won’t help with short-term disabilities at all.

Finally, you need to be aware of the fine print:

- Age Restrictions: Most riders have an age cap. They often stop working once you hit 65, even if your disability continues.

- Exclusions: Some policies won't cover disabilities that stem from pre-existing conditions or are the result of high-risk hobbies.

A Side-by-Side Comparison

To make things simpler, here’s a straightforward table comparing the key arguments for and against adding a waiver of premium rider.

| Pros (Advantages) | Cons (Disadvantages) |

|---|---|

| Protects Your Policy: Prevents your life insurance from lapsing when you can't pay. | Adds to Your Premium: An ongoing cost for a benefit you might never use. |

| Offers Peace of Mind: Reduces financial stress during a major health crisis. | Strict Disability Definitions: Qualifying for the benefit can be difficult and requires proof. |

| Secures Your Family's Future: Ensures your beneficiaries receive the intended death benefit. | Has a Waiting Period: Benefits don't begin immediately; you must wait (often 6 months). |

| Highly Affordable: The cost is usually a small fraction of the overall premium. | Includes Age and Other Limits: The rider typically expires at a certain age, like 65. |

In the end, the decision comes down to your personal risk tolerance and financial situation. For many people, the small added cost is a worthwhile price for the robust protection and security it guarantees.

Who Should Seriously Consider This Rider

A waiver of premium rider can be a game-changer, but let's be honest—it's not for everyone. For some people, though, it’s less of a "nice-to-have" and more of an essential piece of their financial armor. Figuring out if you're in one of those groups is the first step to building a plan that won't fall apart when life gets tough.

This protection is most critical for anyone whose income is directly tied to their ability to get up and go to work. If a disability would slam the brakes on your earnings and throw your family’s stability into chaos, you need to pay close attention.

Let’s break down who stands to gain the most from this powerful safety net.

Sole Breadwinners and Parents of Young Children

When you’re the primary or only income earner, the entire financial weight of the family rests on your shoulders. A long-term disability isn't just about you—it directly impacts your spouse, your kids, and everyone who depends on you. The loss of your income could make it impossible to cover the basics, let alone a life insurance premium.

This becomes even more urgent for parents with little ones. Your life insurance policy is there to protect their future, covering everything from groceries and braces to a college education. A waiver of premium rider acts as a guardian for that promise. It makes sure that even if you can't work, their future stays secure.

Key Insight: For the family's main provider, this rider isn't just about an insurance policy. It's about preserving a legacy and making sure a personal health crisis doesn’t become a financial crisis for the people you love most.

Self-Employed Professionals and Small Business Owners

When you work for yourself, you are the safety net. There's no employer-sponsored disability plan or paid sick leave to catch you. A serious illness or injury means your income can dry up overnight, leaving you to pull from savings to cover both business and personal bills.

A waiver of premium rider fills a huge gap here. It ensures one of your most important assets—your life insurance—stays safe without adding another expense to your plate. By covering the premium, it frees up cash that can go toward medical bills or just keeping your business afloat while you recover. You can get a better feel for your overall coverage needs by learning how to calculate your life insurance need, which is a must-do for any entrepreneur.

Individuals in High-Risk or Physically Demanding Jobs

Your job plays a massive role in your risk of becoming disabled. If you're in a physically demanding field, the odds of suffering an injury that keeps you from working are just plain higher.

Think about these professions:

- Construction Workers and Tradespeople: Electricians, plumbers, and roofers whose entire livelihood depends on their physical health.

- Healthcare Professionals: Surgeons, nurses, and EMTs who face incredible physical and mental strain daily.

- First Responders: Police officers and firefighters who walk into dangerous situations as part of their job description.

For people in these roles, a waiver of premium rider is simply a smart, logical move. It acknowledges the risks you take every day and adds an affordable layer of protection against a career-ending injury.

Anyone with Significant Long-Term Debts

Finally, if you're carrying major long-term debt, you should give this rider a close look. The most obvious example is a mortgage. A big reason you have life insurance is probably to make sure your family can stay in their home if you're gone.

But what if a disability strikes? The mortgage payments don't stop. A waiver of premium rider guarantees that the life insurance policy designed to pay off that debt stays active. It prevents your loved ones from facing the double crisis of your disability and the risk of losing their home. This logic applies to other big debts, too, like student loans or business loans.

Your Top Questions About Premium Waivers, Answered

Even after getting the basics down, it’s completely normal to have a few more questions about how a waiver of premium rider actually works when you need it most. This section is designed to clear up that lingering confusion.

Think of it as our final huddle. We’re here to give you straightforward answers so you can decide with confidence if this rider is a smart move for your financial game plan.

Is This Rider the Same as Disability Insurance?

This is probably the most common—and most important—question people ask. The short answer is no. A waiver of premium rider and a disability insurance policy are two different tools that do two very different jobs.

- Waiver of Premium Rider: Think of this as policy protection. Its one and only job is to pay your life insurance premiums if you become totally disabled. It doesn't send you a check for anything else.

- Disability Insurance: This is income protection. It's designed to replace a chunk of your monthly paycheck if you get sick or hurt and can’t work.

They actually work together perfectly. While your disability insurance is busy helping you pay the mortgage and buy groceries, the waiver of premium rider makes sure your life insurance—the long-term safety net for your family—doesn't disappear. That’s why so many advisors recommend having both.

What Kind of Medical Proof Do Insurers Require?

Kicking this rider into gear isn’t automatic. You have to provide clear, convincing medical evidence that you meet your policy's specific definition of "totally disabled."

Insurers are going to want a complete file to back up your claim. This usually includes:

- Attending Physician's Statement (APS): A detailed report from your doctor that spells out your diagnosis, limitations, and recovery outlook.

- Medical Records: This is the nitty-gritty stuff—lab results, MRI scans, notes from specialists, and anything else that documents your condition.

- Proof of Inability to Work: The paperwork has to connect the dots between your medical condition and why you can no longer do your job.

Don't be surprised if the insurance company asks you to see one of their doctors for an Independent Medical Examination (IME). They do this to get a second opinion. The bottom line is that the burden of proof is on you, so keeping organized records from day one will make the process much smoother.

Heads Up: That definition of "total disability" in your contract is everything. Whether it’s an "own-occupation" or "any-occupation" definition will make or break your claim.

Can I Add This Rider to an Existing Policy?

This is a great question, but the answer is usually no. Most of the time, you have to add a waiver of premium rider when you first buy your life insurance policy. It's built into the initial underwriting.

A few insurers might let you add it later, but it’s not as simple as filling out a form. You’ll almost certainly have to go through medical underwriting all over again. Your current age and any health issues you’ve developed since you first got the policy could make the rider way more expensive—or you might just get denied.

For that reason, the best and cheapest time to add a waiver of premium rider is right at the start, when you first apply for life insurance.

What Happens if I Recover from My Disability?

This benefit is only meant to last as long as your total disability does. If your health improves and you're able to go back to work, the premium waivers will stop.

You're required by your contract to let the insurance company know you've recovered. Once you do, you’ll be responsible for picking up the premium payments again to keep your policy going.

And they don't just take your word for it. Insurers will typically ask for periodic updates to confirm you're still disabled. This could be a yearly form for your doctor to sign or a request for recent medical records. It’s their way of making sure the benefit is only helping those who truly need it.

At My Policy Quote, our mission is to make insurance simple and clear. If you're ready to look at life insurance options that include a waiver of premium rider, our team is here to help you build the right protection for your family. Find your personalized quote today at My Policy Quote.