Choosing the best life insurance for families is one of the most significant financial decisions you'll make, establishing a vital safety net for your loved ones. This isn't just about a policy document; it's a foundational promise to protect their future, ensuring financial stability should the unexpected happen. The right coverage can secure their ability to maintain their quality of life, from keeping the family home and covering daily expenses to funding a child's college education. It transforms potential financial hardship into security during an already challenging time.

The market is filled with diverse options, ranging from straightforward term policies designed for temporary needs to permanent plans that build cash value over time. Understanding the core differences is essential to making an informed choice that aligns with your specific circumstances. For instance, a young family with a mortgage might prioritize a large, affordable term policy, while others may seek the lifelong coverage and investment potential of a whole or universal life plan. For couples seeking to combine coverage, exploring dedicated married life insurance options can help secure both partners' futures.

This guide is designed to eliminate the confusion. We will break down the 8 best life insurance options for families, providing a clear and comprehensive roundup. You'll learn about each type's distinct features, pros, cons, and estimated costs, empowering you to compare them effectively. Our goal is to equip you with the knowledge to select the financial shield that offers true peace of mind and safeguards your family’s tomorrow.

1. Term Life Insurance: Maximum Protection for Key Years

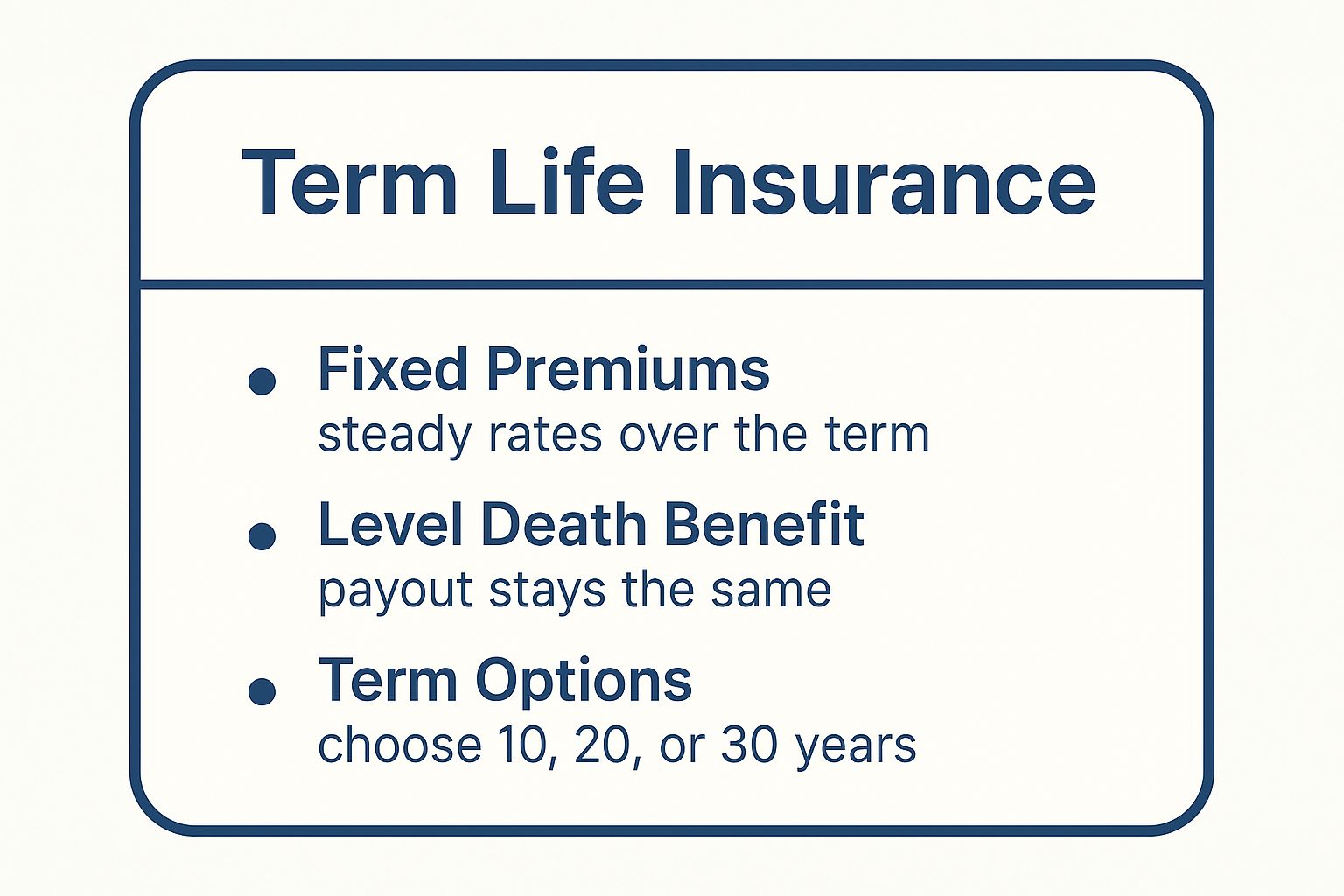

Term life insurance is the most straightforward and affordable type of life insurance, making it a foundational choice for most families. It provides a death benefit to your beneficiaries if you pass away during a specific, pre-determined period, or "term." These terms typically last 10, 20, or 30 years, designed to align with major financial responsibilities.

The primary purpose of term life insurance is to provide a financial safety net during your family's most vulnerable years. Think of it as pure protection. If you have a 30-year mortgage or young children who will depend on your income for the next two decades, a term policy ensures those obligations are covered. For many, this makes it the best life insurance for families looking for maximum coverage at the lowest possible cost.

How Term Life Insurance Works for Families

The concept is simple: you pay a fixed premium each month or year for the duration of the term. If you die within that term, your beneficiaries receive the full, tax-free death benefit. If you outlive the term, the policy expires, and no benefit is paid.

- Example Scenario 1: A 35-year-old parent with two young children and a mortgage purchases a $750,000, 20-year term policy. This coverage is designed to replace their income and cover college costs until the children are adults. Their premium could be as low as $40 per month.

- Example Scenario 2: A two-income household buys separate 30-year term policies on both spouses. This ensures that if either partner passes away, the surviving spouse can manage the mortgage, daily expenses, and future goals without financial strain.

Key Features and Strategic Tips

When considering term life insurance, its core features are designed for stability and predictability. This quick reference box summarizes the key structural elements of a typical term policy.

These features ensure that your family’s financial protection remains consistent and your budget stays predictable for the entire policy duration. To make the most of your policy, consider these actionable tips:

- Calculate Coverage Wisely: A common rule of thumb is to secure coverage equal to 10-12 times your annual income.

- Choose Level Premiums: Opt for a "level term" policy where your premium is locked in, rather than an "annually renewable" policy where costs increase each year.

- Look for Convertibility: A convertible term policy allows you to convert some or all of your coverage to a permanent policy later on without a new medical exam, offering crucial future flexibility.

2. Whole Life Insurance: Lifelong Protection and Guaranteed Growth

Whole life insurance offers a permanent solution that combines a guaranteed death benefit with a cash value savings component. Unlike term insurance, it is designed to last your entire life, providing certainty that your beneficiaries will receive a payout. The policy also builds cash value at a fixed, predictable rate, making it a conservative long-term financial planning tool for families.

This type of policy is often considered one of the best life insurance for families seeking stability, wealth transfer capabilities, and a financial asset that grows over time. It serves as both protection and a disciplined savings vehicle, ensuring your family has a permanent safety net that will never expire as long as premiums are paid.

How Whole Life Insurance Works for Families

With whole life, you pay a consistent premium for the life of the policy. A portion of that premium pays for the insurance, and the rest contributes to a cash value account that grows tax-deferred. You can borrow against this cash value or surrender the policy for the cash, though doing so may impact the death benefit.

- Example Scenario 1: A high-net-worth family uses a whole life policy to create a tax-free inheritance for their children and to cover potential estate taxes, ensuring their assets are passed on efficiently.

- Example Scenario 2: Parents purchase a small whole life policy for their young child. This locks in a low premium rate for life and guarantees their future insurability, regardless of any health issues they may develop later.

- Example Scenario 3: Two business partners fund a buy-sell agreement with separate whole life policies. If one partner dies, the death benefit provides the surviving partner with the capital needed to buy out the deceased partner's share of the business from their heirs.

Key Features and Strategic Tips

Whole life insurance is defined by its guarantees and permanence. These features provide a bedrock of financial security that can be relied upon for decades, making it a powerful tool for life insurance for parents who want to leave a lasting legacy.

To maximize the benefits of a whole life policy, it's crucial to approach it with a long-term strategy. Consider these actionable tips:

- Focus on Mutual Insurers: Choose a policy from a mutual insurance company (like Northwestern Mutual or MassMutual) with a strong history of paying dividends, which can significantly enhance your policy's cash value and death benefit.

- Utilize Paid-Up Additions (PUAs): Use dividends or extra payments to purchase "paid-up additions." These are small, fully paid-up blocks of insurance that increase both your death benefit and your cash value, accelerating policy growth.

- Plan for the Long Haul: Whole life is a long-term commitment. To see substantial cash value growth, plan to hold the policy for at least 15-20 years.

- Compare Illustrations Carefully: When comparing policies, look closely at the assumptions used in the illustrations, especially the guaranteed values versus the non-guaranteed dividend projections.

3. Universal Life Insurance: Flexible Permanent Protection

Universal life (UL) insurance is a type of permanent life insurance that offers lifelong coverage combined with unparalleled flexibility. It allows families to adjust their premium payments and death benefit as their financial needs evolve, making it an excellent choice for those with fluctuating incomes or changing long-term goals.

The core advantage of universal life insurance is its adaptability. Unlike term or whole life policies with rigid structures, a UL policy can be modified to fit your circumstances. This makes it a strong candidate for the best life insurance for families who need permanent coverage but anticipate changes in their financial journey, such as career growth, business ownership, or eventual retirement.

How Universal Life Insurance Works for Families

A UL policy has two main components: a death benefit and a cash value account. A portion of your premium payment goes toward the cost of insurance, while the remainder is deposited into the cash value account, which earns interest. The policy’s flexibility allows you to use this cash value to pay premiums or adjust your coverage.

- Example Scenario 1: A self-employed professional with a variable income purchases a UL policy. During a high-earning year, they overfund the policy to build cash value. In a leaner year, they can use that accumulated cash value to cover the premiums, ensuring their family’s protection never lapses.

- Example Scenario 2: A family reduces their death benefit once their mortgage is paid off and their children are financially independent. This lowers the cost of insurance, allowing more of their premium to build cash value for supplemental retirement income or estate planning.

Key Features and Strategic Tips

Universal life insurance is defined by its adjustable nature, offering a dynamic way to manage long-term financial security. Understanding its mechanics is crucial to maximizing its value.

These features provide a powerful tool for long-term planning, but they require active management to perform optimally. To leverage your policy effectively, consider these actionable strategies:

- Fund Above the Minimum: Consistently paying only the minimum premium may cause the policy to lapse later in life as insurance costs rise. Funding above the minimum builds a cash value cushion.

- Monitor Policy Performance: Request an in-force illustration from your insurer annually. This statement shows how your policy is performing and projects its future sustainability based on current interest rates and charges.

- Understand Fees and Charges: Be aware of all potential costs, including administrative fees, cost of insurance charges, and surrender charges. Knowing these helps you manage the policy effectively. To understand how these factors evolve, it's wise to learn more about what type of life insurance is best in your 30s, 40s, and 50s.

4. Variable Life Insurance: Growth Potential for Savvy Investors

Variable life insurance is a type of permanent policy that combines a death benefit with a cash value component that can be invested in a variety of separate accounts, similar to mutual funds. This option is geared toward families with a higher risk tolerance who want the potential for greater cash value growth tied to market performance.

The primary purpose of variable life insurance is to offer both protection and a tax-advantaged investment vehicle. The policyholder directs how the cash value is invested, choosing from a portfolio of stock, bond, and money market funds. This control makes it a potentially powerful tool for supplementing retirement savings or building wealth, though it comes with investment risk. For financially savvy individuals, this can be the best life insurance for families looking to integrate their protection and investment strategies.

How Variable Life Insurance Works for Families

With variable life insurance, a portion of your premium pays for the cost of insurance, while the rest is invested in the sub-accounts you select. The cash value and, in some cases, the death benefit can fluctuate daily based on the performance of these investments.

- Example Scenario 1: A high-income professional, having already maxed out their 401(k) and IRA contributions, uses a variable life policy as an additional tax-deferred investment vehicle. They allocate their cash value to a diversified mix of equity and bond funds, aiming for long-term growth to supplement their retirement income.

- Example Scenario 2: A business owner funds a variable life policy as part of an executive compensation plan. The policy's potential for high returns makes it an attractive benefit, and the death benefit provides a key-person protection component for the business.

Key Features and Strategic Tips

When considering variable life insurance, understanding its dual nature as both an insurance and investment product is critical. Its features are designed for those comfortable with active management and market volatility.

This policy type requires active monitoring and a clear understanding of market dynamics. To leverage a variable life policy effectively, consider these actionable tips:

- Maintain Diversified Investments: Avoid concentrating your cash value in a single fund. Spread investments across different asset classes to mitigate risk.

- Review Performance Regularly: Treat it like any other investment. Review your sub-account performance quarterly and rebalance your portfolio as needed to stay aligned with your financial goals.

- Ensure Adequate Funding: Your policy's performance can impact its costs. Ensure you are funding it sufficiently to cover the mortality and expense charges, especially during market downturns, to prevent the policy from lapsing.

- Understand All Fees: Variable policies come with investment management fees, administrative charges, and surrender charges. Be sure you fully understand the fee structure before purchasing.

5. Indexed Universal Life (IUL): Growth Potential with a Safety Net

Indexed Universal Life (IUL) insurance is a sophisticated form of permanent life insurance that offers a unique hybrid approach to cash value growth. It provides a death benefit alongside a savings component that is linked to the performance of a stock market index, like the S&P 500, without directly investing in the market. This structure gives families the opportunity for higher returns while protecting the cash value from market losses.

IUL policies are designed for families seeking more than just a death benefit; they want a flexible financial tool that can supplement retirement income, fund education, or build tax-advantaged wealth. By offering a guaranteed minimum interest rate (often 0%), your cash value is protected during market downturns. This combination of growth potential and downside protection makes it a compelling option for those looking for the best life insurance for families with long-term financial goals.

How IUL Works for Families

With an IUL, a portion of your premium pays for the cost of insurance and fees, while the rest goes into a cash value account. This account earns interest based on the upward movement of a selected stock index. The insurance company sets a "cap rate," which is the maximum interest you can earn, and a "floor rate," which is the minimum (typically 0%), ensuring your principal is safe.

- Example Scenario 1: A middle-class family wants to build a tax-free supplemental retirement fund. They purchase an IUL, and over 25 years, the cash value grows based on positive S&P 500 performance. In retirement, they can take tax-free loans against the cash value to boost their income.

- Example Scenario 2: A business owner uses an IUL for estate planning. The policy's death benefit will provide liquidity to their heirs to pay estate taxes, and the cash value grows without market risk, ensuring the funds will be available when needed.

Key Features and Strategic Tips

IUL policies are defined by their unique crediting methods and flexibility. Understanding these structural elements is crucial for maximizing the policy's value for your family.

- Understand Key Terms: Before buying, learn about cap rates (the maximum return), participation rates (the percentage of index growth credited to you), and spreads (a percentage deducted from the index's return).

- Fund It Properly: To maximize growth potential and ensure the policy remains in force, consider funding the policy above the minimum premium illustrated by the agent.

- Review Index Options: Most IULs offer multiple index choices. Diversify your allocations or choose the one that best aligns with your risk tolerance and growth expectations.

- Monitor Annually: An IUL is not a "set it and forget it" product. Review your annual statements with an experienced IUL specialist to ensure it is performing as expected and meeting your long-term goals.

6. Group Life Insurance Through Employers: A Convenient Starting Point

Group life insurance offered by an employer is often a family's first introduction to life insurance coverage. This benefit typically provides a death benefit equal to one or two times your annual salary, often at no cost or a very low group rate. It's an incredibly convenient and accessible form of protection that requires minimal effort to enroll.

The primary purpose of group life insurance is to provide a foundational layer of financial security. While it is rarely enough to cover a family's long-term needs, it serves as an excellent, low-cost starting point. Because enrollment is guaranteed for a base amount, it’s often the best life insurance for families who need immediate, basic coverage without a medical exam, especially if a household member has pre-existing health conditions that might make individual policies expensive.

How Group Life Insurance Works for Families

The mechanism is simple: your employer sponsors a master policy, and you enroll as a member of the group, usually during your initial hiring or annual open enrollment. The premium, if any, is typically deducted directly from your paycheck.

- Example Scenario 1: A new employee at a large corporation is automatically enrolled in a company-paid group policy worth $50,000. They also have the option to buy supplemental coverage up to three times their salary at a low group rate, which they add to bolster their protection.

- Example Scenario 2: A government worker receives a generous group policy equal to two times their annual salary. They recognize this isn't enough to cover their mortgage and children's education, so they purchase an individual 20-year term policy to fill the gap.

Key Features and Strategic Tips

Group life insurance is defined by its convenience and accessibility, but it comes with limitations you must understand. The core features are designed for ease of administration for the employer, not comprehensive protection for the employee.

These features make group coverage a great perk, but not a complete strategy. To maximize this benefit and ensure your family is truly protected, follow these actionable tips:

- Maximize the Freebie: Always sign up for the employer-paid portion of the coverage. It’s a free financial safety net.

- Supplement, Don't Rely: Use group insurance as a base and buy a separate individual policy that you own and control. This ensures you have coverage even if you change jobs.

- Understand Portability Rules: Find out if you can convert your group policy to an individual policy (portability) if you leave your job. Be aware that the premiums for a converted policy are often significantly higher.

- Review During Open Enrollment: Re-evaluate your needs and coverage options annually. A promotion or new child may warrant purchasing additional supplemental coverage if available.

7. Child Life Insurance: Securing Their Future Insurability

Child life insurance is a unique financial tool designed to provide a small death benefit for a minor child, but its primary value lies in guaranteeing their future insurability. These policies, often purchased as whole life insurance, lock in a child's ability to get coverage as an adult, regardless of any health issues that may arise later in life.

The main purpose of a child policy is not to replace income but to serve as a long-term strategic gift. It ensures that a childhood illness or a genetic condition discovered later on won't prevent them from qualifying for their own affordable life insurance when they have a family and mortgage. This makes it a potential option as one of the best life insurance for families who are focused on generational financial planning.

How Child Life Insurance Works for Families

A parent, grandparent, or legal guardian purchases a small whole life policy (typically $10,000 to $50,000) on a child. You pay a low, fixed premium, and the policy builds a modest cash value over time. The key feature is the "guaranteed purchase option" or "guaranteed insurability rider," which allows the child to buy additional coverage at specific milestones as an adult without a medical exam.

- Example Scenario 1: Grandparents purchase a $25,000 whole life policy for their newborn grandchild as a gift. The premium is minimal, and when the child turns 25, they can purchase a much larger policy to protect their own family, even if they've since developed a chronic health condition.

- Example Scenario 2: A couple with a family history of diabetes buys a policy for their young child. This acts as a safeguard, ensuring their child can secure affordable coverage as an adult, which might otherwise be difficult or expensive to obtain.

Key Features and Strategic Tips

While the death benefit is a component, the long-term benefits are the real focus. The best use of these policies is strategic, not just for immediate coverage. As you explore why life insurance matters when you have kids, understanding these features is crucial. Learn more about protecting your children's future.

To make the most of a child life insurance policy, keep these tips in mind:

- Prioritize the Guaranteed Insurability Rider: This is the most valuable feature. Ensure the policy includes a rider that allows the child to purchase significant additional coverage in the future.

- Consider a Child Rider First: Before buying a standalone policy, check if you can add a "child term rider" to your own term life insurance policy. This is often a more cost-effective way to get a death benefit for all your children under one provision.

- Compare with Education Savings Plans: If your primary goal is saving for college, compare the cash value growth of a child policy to a dedicated 529 plan, which offers tax advantages specifically for education.

- Understand the Long-Term Purpose: A child policy is a long-game tool. When the child becomes an adult, transfer ownership and educate them on how to use its benefits to build their own financial foundation.

8. Return of Premium Term Life Insurance: Protection with a Payback

Return of Premium (ROP) term life insurance offers a unique twist on traditional term coverage, appealing to families who want protection but dislike the idea of paying for a benefit they may never use. This policy provides a death benefit if you pass away during the term, but if you outlive it, the insurance company refunds all the premiums you paid.

The core purpose of ROP is to eliminate the "use it or lose it" aspect of standard term life insurance. It functions as a forced savings mechanism combined with pure protection, ensuring you either leave behind a death benefit or get your money back. For families seeking a no-loss proposition, this hybrid approach makes it one of the best life insurance for families who value guaranteed financial outcomes.

How ROP Term Life Insurance Works for Families

The mechanics are similar to a standard term policy: you select a coverage amount and a term length (typically 20 or 30 years) and pay fixed premiums. The key difference is the premium cost, which is significantly higher than a traditional term policy. In exchange for this higher cost, you are guaranteed to receive a full, tax-free refund of all premiums paid if you are still alive when the policy expires.

- Example Scenario 1: A 40-year-old professional buys a $500,000, 20-year ROP policy. The premium might be $150 per month, compared to $45 for a standard term policy. If they pass away during the 20 years, their family receives $500,000. If they outlive the term, they receive a check for $36,000 ($150 x 12 months x 20 years).

- Example Scenario 2: A conservative couple, hesitant to "waste" money on insurance, opts for ROP policies. They view the extra premium cost as a disciplined way to save for a future goal, like a down payment on a vacation home, knowing their protection is in place.

Key Features and Strategic Tips

ROP policies are structured to provide both a safety net and a financial return, but it's crucial to understand the trade-offs. The higher cost is the most significant factor to weigh against the guaranteed payback.

When evaluating if ROP is the right fit, consider these strategic points to maximize its value for your family:

- Compare the Opportunity Cost: Before committing, calculate what you could earn by buying a cheaper, standard term policy and investing the premium difference. An ROP policy often yields a very low, or even zero, rate of return compared to investing.

- Assess Premium Affordability: ROP premiums are substantially higher. Ensure you can comfortably afford the payments for the entire term, as lapsing the policy means you forfeit both the coverage and the premium refund.

- Account for Inflation: The lump sum you receive back in 20 or 30 years will have less purchasing power due to inflation. Factor this into your decision-making process.

- Understand Policy Riders: Some ROP policies allow for additional benefits, and it's important to know how they affect your premium return. You can learn more about adding a spouse term rider and other options to customize your coverage.

Top 8 Family Life Insurance Comparison

| Insurance Type | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Term Life Insurance | Low – straightforward policy | Low – affordable premiums | Temporary coverage, no cash value | Young families needing max coverage on a budget | Lowest premiums, simple, max coverage for term |

| Whole Life Insurance | High – complex structure | High – higher premiums | Permanent coverage with guaranteed cash value | Affluent families seeking permanent coverage & wealth transfer | Guaranteed cash value, fixed premiums, dividends |

| Universal Life Insurance | Medium – flexible and adjustable | Medium – flexible premium payments | Permanent coverage with variable cash value | Families wanting premium flexibility and adjustable coverage | Flexible premiums, adjustable death benefits |

| Variable Life Insurance | High – requires investment knowledge | High – active management and fees | Potential for high cash value growth with investment risk | Investment-savvy families seeking growth potential | Investment control, tax-deferred growth |

| Indexed Universal Life (IUL) | Medium-High – hybrid complexity | Medium – moderate premiums, linked to index | Market-linked growth with downside protection | Families wanting market upside with safety nets | Market upside potential, downside protection |

| Group Life Insurance Through Employers | Low – automatic enrollment | Low – employer-paid or low-cost | Basic life coverage, often insufficient alone | Employed individuals needing foundational coverage | No medical exams, convenient, often free |

| Child Life Insurance | Low – simple policies | Low – low premiums | Permanent coverage with cash value for children | Families prioritizing child’s future insurability & savings | Locks insurability, low cost, cash value growth |

| Return of Premium Term Life Insurance | Medium – term plus refund feature | High – premium 2-4x regular term cost | Term coverage with premium refund if alive | Conservative families wanting term coverage plus premium return | Premium refund, forced savings, peace of mind |

Making Your Final Decision: Next Steps to Secure Your Family's Future

Choosing the right life insurance is one of the most significant financial decisions you will make for your family. It's a foundational act of love, providing a safety net that protects your loved ones from financial hardship when they are at their most vulnerable. Throughout this guide, we've navigated the landscape of family life insurance, from the straightforward protection of Term Life to the complex, growth-oriented features of Variable and Indexed Universal Life policies.

The central truth is that there is no universal "best" policy. The best life insurance for families is the one that aligns perfectly with your unique circumstances. Your decision hinges on a careful evaluation of your family's needs, your long-term financial goals, and your current budget. The ideal policy for a young family of four seeking affordable income replacement will look very different from the one chosen by a high-net-worth individual focused on wealth transfer and estate planning.

Key Takeaways to Guide Your Choice

As you move from learning to deciding, keep these core principles at the forefront of your mind:

- Clarity of Purpose: Define exactly what you want the insurance to accomplish. Is its primary job to pay off the mortgage and cover college tuition if you pass away unexpectedly? Or are you looking for a financial tool that also builds cash value and can supplement your retirement income? Answering this question will immediately narrow down your options.

- Term vs. Permanent: This is the most fundamental choice. Term life is simple, affordable, and covers you for a specific period, making it ideal for covering finite needs like a mortgage or raising children. Permanent life insurance (Whole, Universal, etc.) is a lifelong financial asset with a savings component, suited for goals like estate planning or leaving an inheritance.

- Cost is Not the Only Factor: While affordability is crucial, the cheapest policy isn't always the best. Consider the insurer's financial strength rating (e.g., from A.M. Best), customer service reputation, and the specific riders or features included that might add significant value for your family, such as an accelerated death benefit rider.

Your Actionable Next Steps

Information is only powerful when acted upon. Here is a clear, step-by-step path to take you from consideration to a confident decision:

- Calculate Your Coverage Needs: Don't guess. Use a comprehensive needs calculator or the DIME method (Debts, Income, Mortgage, Education) to arrive at a realistic coverage amount. Factor in final expenses, outstanding loans, and the annual income your family would need to maintain their standard of living for a set number of years.

- Evaluate Your Budget: Determine a realistic monthly or annual premium you can comfortably afford. This will help you balance the desired coverage amount and policy type with your current financial obligations.

- Explore Advanced Strategies: For those with more complex financial situations, life insurance can play a sophisticated role in wealth management. Once you understand the various types of life insurance, you can explore strategies for leveraging life insurance for your estate plan to help minimize taxes and ensure a smooth transfer of assets to your heirs.

- Compare Multiple Quotes: This step is non-negotiable. Premiums for the exact same coverage can vary dramatically between insurers based on their underwriting criteria. Obtaining quotes from at least three to five different top-rated companies is essential to ensure you are getting the most competitive rate.

Securing your family's financial future is a profound promise. It’s an investment that delivers immeasurable peace of mind today, knowing that no matter what happens, the people you care about most will be protected. Don't let indecision lead to inaction. The best time to get life insurance is always now, while you are younger and healthier. Take these final steps and turn your intention into a lasting legacy of security.

Ready to find the perfect policy without the hassle? At My Policy Quote, we do the heavy lifting for you by comparing rates from top-rated insurance carriers, ensuring you find the best coverage at the most competitive price. Get your free, personalized quotes in minutes and take the first step toward securing your family’s future today at My Policy Quote.