When you’re an independent contractor, you’re the CEO, the creative director, and, most importantly, the entire safety department. Traditional jobs wrap you in a cocoon of employer-sponsored health plans and liability coverage. But when you strike out on your own, you’re the one who has to build the safety net.

This guide is your blueprint for doing just that.

Why Insurance for Independent Contractors Is Non-Negotiable

Going it alone without insurance for independent contractors is like walking a tightrope with no net below. The freedom is amazing, but one misstep could lead to a financial freefall. You don't have the standard protections of a W-2 employee, which leaves you, your business, and your personal assets completely exposed.

Every project, every client, and every single workday carries its own set of risks.

The stakes are much higher than most freelancers think. There's a reason the global liability insurance market is valued at around $290.5 billion in 2024. It’s not just a number; it’s a reflection of real-world risk.

Shockingly, studies show that anywhere from 36% to 53% of small businesses get hit with a lawsuit in any given year. Almost 90% will face legal action at some point. Those aren't just statistics; they're cautionary tales. You can learn more about these legal exposure risks and see the full report.

To truly understand the landscape, it helps to see the threats and solutions side-by-side.

Why Independent Contractors Need Insurance At a Glance

| Risk Type | Potential Consequence | Primary Insurance Solution |

|---|---|---|

| Client Lawsuit | A client claims your work caused them a financial loss, leading to a costly legal battle. | Professional Liability Insurance (Errors & Omissions) |

| On-Site Accident | Someone gets injured at your home office or a client's site, making you liable for their medical bills. | General Liability Insurance |

| Sudden Illness or Injury | An unexpected health issue leads to massive medical debt and an inability to work. | Health Insurance & Disability Insurance |

| Data Breach | Client data is stolen from your systems, resulting in legal action and reputational damage. | Cyber Liability Insurance |

| Property Damage | A fire or theft destroys your essential work equipment, halting your business operations. | Commercial Property Insurance |

This table lays it all out—for every potential disaster, there's a specific shield to protect you.

From Liability to Livelihood

Your insurance needs go way beyond just protecting your business from mistakes. While liability policies are the bedrock, a real safety net protects the most important asset of all: you.

This guide covers the whole spectrum, helping you shield both your professional reputation and your personal well-being.

We'll walk through how to:

- Protect Your Business: Keep your company safe from lawsuits, client disputes, and accidents with the right liability policies.

- Secure Your Income: Make sure your personal finances are rock-solid with health, disability, and life insurance.

- Manage Costs Effectively: Learn the ropes of finding affordable coverage that doesn't skimp on protection.

Stop thinking of insurance as just another bill. It’s one of the smartest investments you can make in your business. It buys you the peace of mind to focus on what you do best—delivering great work and growing your client base.

This guide will break it all down into simple, clear steps. You’ll learn how to figure out your specific risks, compare different policies, and build an insurance portfolio that’s right for you. By the end, you'll see insurance not as a confusing chore, but as your strongest ally for long-term success.

Protecting Your Business with Core Liability Policies

If your business is your castle, then liability insurance is the moat, the walls, and the watchtower keeping it safe. These policies are the absolute foundation of insurance for independent contractors. They’re designed to shield your finances from claims of damage, error, or simple bad luck.

Think of them as your first line of defense. Lawsuits can drain your savings and threaten the very business you’ve worked so hard to build.

Accidents happen. Mistakes are made. It's part of life. But when you’re flying solo as an independent contractor, the fallout from those incidents lands squarely on your shoulders. Liability insurance is what transfers that immense financial risk from you to an insurance company, giving you the freedom to do your best work without constant worry.

Let's break down the three core liability policies that every contractor needs to have on their radar.

General Liability: The Shield Against Physical Mishaps

This is your classic “slip-and-fall” coverage. General liability insurance protects you when your business operations cause bodily injury to someone or damage to their property. It’s all about tangible, real-world accidents.

Picture these all-too-common scenarios:

- A freelance photographer is on a shoot at a client’s home and accidentally knocks over an antique lamp, shattering it. General liability can cover the cost to replace it.

- A marketing consultant meets a potential client at a coffee shop. The client trips over the consultant’s laptop bag, falls, and breaks their wrist. This policy helps cover the medical bills that follow.

- A home organizer working in a client's kitchen inadvertently causes a small water leak that damages the hardwood floors. General liability is there to handle the repair costs.

Without this coverage, you’d be paying for those expenses out of your own pocket—and they can add up fast. It’s a must-have for anyone who interacts with clients or the public in a physical space, even if that space is just a client’s office.

Professional Liability: The Malpractice Insurance for Your Expertise

While general liability handles physical accidents, professional liability insurance steps in to cover financial damages caused by your professional services or advice. It’s often called Errors & Omissions (E&O) insurance, and it’s like malpractice insurance for a doctor, but built for consultants, designers, developers, and other experts.

This policy defends your most valuable asset: your professional reputation. It kicks in when a client claims you made a mistake, were negligent, or failed to deliver on a promise, costing them money.

Professional liability insurance is critical because it defends you against claims of what you did or what you failed to do with your expertise. It protects your advice, your code, your designs, and your strategic guidance.

For example, imagine a freelance web developer builds an e-commerce site for a retailer. A month after launch, a hidden coding error leads to a data breach, costing the client thousands in lost sales. The client could sue the developer for negligence. A professional liability policy would be there to cover the legal defense and any potential settlement.

Cyber Liability: Your Defense in the Digital Age

In a world where everything is connected, cyber liability insurance isn't just for big tech companies anymore. If you handle any sensitive client information—names, addresses, payment details, or proprietary data—you are a target. A stolen laptop, a clever phishing email, or a hacked cloud account can expose your clients' private information in an instant.

Cyber liability insurance helps you manage the chaos that follows a data breach. It can cover the staggering costs associated with:

- Notifying every client whose data was compromised.

- Providing credit monitoring services to protect victims.

- Hiring a PR firm to manage your damaged reputation.

- Paying for legal fees and regulatory fines that may come your way.

The financial and reputational fallout from even a small breach can be devastating for a solo practitioner. In fact, many clients now demand you have this coverage before they’ll even sign a contract. You can learn more about specific contractor insurance requirements in our complete guide.

Securing Your Income and Personal Well-Being

While liability policies shield your business from the outside world, what about the policies that protect you? As an independent contractor, there’s no HR department looking out for your benefits. You are the safety net.

Your health, your ability to earn an income, and your family's future all rest on your shoulders. Building a personal insurance plan isn't just a smart move; it's the foundation of a long-lasting freelance career. Without it, one bad fall or a sudden illness could wipe out everything you've worked so hard to build.

Navigating Health Insurance as a Contractor

When you step away from a traditional 9-to-5, group health insurance is usually the first benefit you lose. Suddenly, you're on your own, trying to make sense of a world of plans and premiums. It can feel like a lot, but it’s a non-negotiable step toward protecting yourself.

To get started, it helps to know the language:

- Deductible: The amount you have to pay out-of-pocket before your insurance kicks in. Think of it as your initial investment in your care for the year.

- Co-pay: A simple, fixed fee you pay for certain services, like a doctor’s visit, once you’ve met your deductible.

- Premium: Your monthly membership fee. You pay it to keep your plan active, whether you see a doctor or not.

The good news? You have plenty of options. You can find plans on the Health Insurance Marketplace, go directly to private insurers, or even join professional groups that offer coverage to members. If you need a hand cutting through the noise, you can get quality health insurance fast by talking to people who get what freelancers need.

Disability Insurance: Your Paycheck Protection

Let's be real. If you get sick or injured and can't work for a few months, what happens to your income? For most contractors, it just stops. Cold. That’s why disability insurance isn't a luxury—it's one of the most important tools you can have.

Think of disability insurance as paycheck protection. It’s not about covering a single hospital bill. It’s about replacing your income so you can still pay the mortgage, buy groceries, and keep the lights on while you get back on your feet.

Imagine a freelance graphic designer who spends her days creating amazing visuals. She develops severe carpal tunnel and her doctor says she can't use a mouse or stylus for six months. Without an income, her savings would drain, and debt would start piling up.

But she had a disability policy. It started paying her a monthly benefit equal to 60% of what she used to earn. That check became her lifeline. It allowed her to focus on healing, not on how she was going to survive financially. That's the real power of protecting your ability to earn.

Life Insurance: Protecting Your Loved Ones

If you have a family that depends on your income, life insurance is an absolute must. It’s the promise that if the worst happens to you, they won't be left with a legacy of bills and financial chaos. It’s about taking care of them, no matter what.

A life insurance policy gives your family a tax-free payment after you're gone. This money can help them:

- Replace the income you provided, for years to come.

- Pay off the mortgage and other debts.

- Fund a child's college education.

- Cover funeral costs and give them space to grieve without financial stress.

Knowing your family is protected provides a kind of peace that you can't put a price on. It turns all your hard work into something that not only supports them today but secures their tomorrow.

Figuring Out Your Insurance Costs (and How to Lower Them)

To get a handle on your insurance costs, you first have to understand where those numbers come from. Premiums aren't just pulled out of a hat; they’re a calculated reflection of your specific business risk. Think of it as a sliding scale—the more risk an insurer sees, the higher your premium will be.

An insurance company looks at a freelance graphic designer working from a home office very differently than a contractor overseeing a busy construction site. The designer’s biggest worry might be a data breach. The contractor, on the other hand, deals with the daily possibility of physical injury and property damage. That gap in risk is the single biggest driver behind your insurance price tag.

Market trends also play a huge part. For instance, even when some global insurance rates are dropping, other types can climb. We recently saw the cost of casualty insurance—which covers general liability—go up in the U.S. because of a spike in claims. So, while some coverage might get cheaper, the liability protection most contractors can't live without is always in flux.

What Goes Into Your Premium?

A handful of key factors come together to shape your final quote. Knowing what they are gives you the power to make smarter decisions and, hopefully, bring your costs down.

This table breaks down the main variables that insurers look at when they're calculating your premium.

| Cost Factor | Why It Matters | Example |

|---|---|---|

| Your Profession | High-risk work (like construction) naturally costs more to insure than low-risk work (like freelance writing). | A roofer will always pay more for liability insurance than a virtual assistant. |

| Coverage Limits | The more financial protection you want, the higher the premium. | A policy with a $2 million liability limit is going to cost more than one with a $500,000 limit. |

| Deductible Amount | This is what you agree to pay yourself before the insurance company steps in. | Choosing a $2,500 deductible instead of a $500 one will usually lower your monthly payment. |

| Claims History | A history of filing claims signals to insurers that you're a higher risk, which can lead to higher rates. | A business with two liability claims in three years will likely see a premium increase at renewal. |

| Business Location | Rates can change a lot based on state laws and the local risk of events like floods or wildfires. | A contractor in a hurricane-prone state will pay more for property insurance than one in a low-risk area. |

Understanding these moving parts is the first step. The next is taking action.

Smart Ways to Cut Your Insurance Costs

You can’t change the risks of your industry, but you have more control than you think. A few strategic moves can make your coverage much more affordable without leaving you exposed.

Here are some of the best ways to find some savings:

- Bundle Your Policies: Ask about a Business Owner's Policy (BOP). It combines general liability and commercial property insurance into a single package, often for a much lower price than buying them separately.

- Raise Your Deductible: If you have a solid emergency fund, think about increasing your deductible. When you agree to cover a larger portion of a claim yourself, insurers often reward you with a lower premium.

- Get Serious About Risk Management: The best way to keep costs low is to avoid claims in the first place. Use rock-solid client contracts, keep your workspace safe, and document everything to prevent mistakes.

Joining a professional association can be a total game-changer. These groups often negotiate group insurance rates for their members, giving you access to top-tier coverage at a fraction of the cost.

And don’t forget about your health coverage—it's another major expense. It pays to shop around and compare all your options so you're not spending more than you have to. We cover this in-depth in our guide to affordable health insurance options.

Your Step-By-Step Guide to Getting Covered

Trying to secure the right insurance can feel like you're staring at a thousand-piece puzzle. It’s overwhelming. But it doesn't have to be.

Let's break it down into a few simple, clear actions. Think of this as your roadmap to building a real safety net for your business—one that protects your hard work and gives you total peace of mind.

Start by Assessing Your Professional Risks

Before you can even think about shopping for a policy, you have to know what you’re protecting yourself from. This is the most important step. A freelance writer's biggest threat isn't the same as an IT consultant's or a construction contractor's.

So, take a moment to be brutally honest about your daily operations.

Ask yourself these questions:

- Do I meet clients in person? If the answer is yes, you're one slip-and-fall away from a lawsuit. That points directly to General Liability insurance.

- Could my advice or work cost a client money? If a mistake on your end could hurt their bottom line, you absolutely need Professional Liability (E&O) insurance.

- Do I handle sensitive client data? We’re talking names, emails, payment info—anything. If you store it, Cyber Liability is non-negotiable.

- What happens if I get sick or hurt and can't work? If an injury would immediately shut off your income, Disability Insurance is your lifeline.

This quick self-audit acts as your compass. It stops you from overpaying for coverage you don’t need and, more importantly, from leaving yourself exposed to the very things that could sink your business.

Gather Your Essential Documents

Okay, you know what you need. Now it’s time to get your paperwork in order. Insurers need some basic info to give you an accurate quote, and having it ready makes the whole process faster and smoother.

You’ll generally need to have these on hand:

- Your business name and address

- Your business license or registration number

- A simple, clear description of what you do

- Your estimated annual revenue or recent income statements

This information gives providers a snapshot of your business—its size, its nature, and its risks—so they can build a policy that actually fits.

Compare Providers and Get Quotes

Now for the fun part: shopping around. The good news is that the insurance market has finally caught up with the freelance economy, so you have more choices than ever.

The global insurance industry pulled in a staggering EUR 7.0 trillion in premium income in 2024. A huge chunk of that—the property and casualty insurance that contractors rely on—grew by 7.7%. This isn't just a random number; it shows a massive shift as more professionals recognize their risks. North America is leading the charge, making up over half of the world's premiums. You can discover more insights about this growing market on Allianz.com.

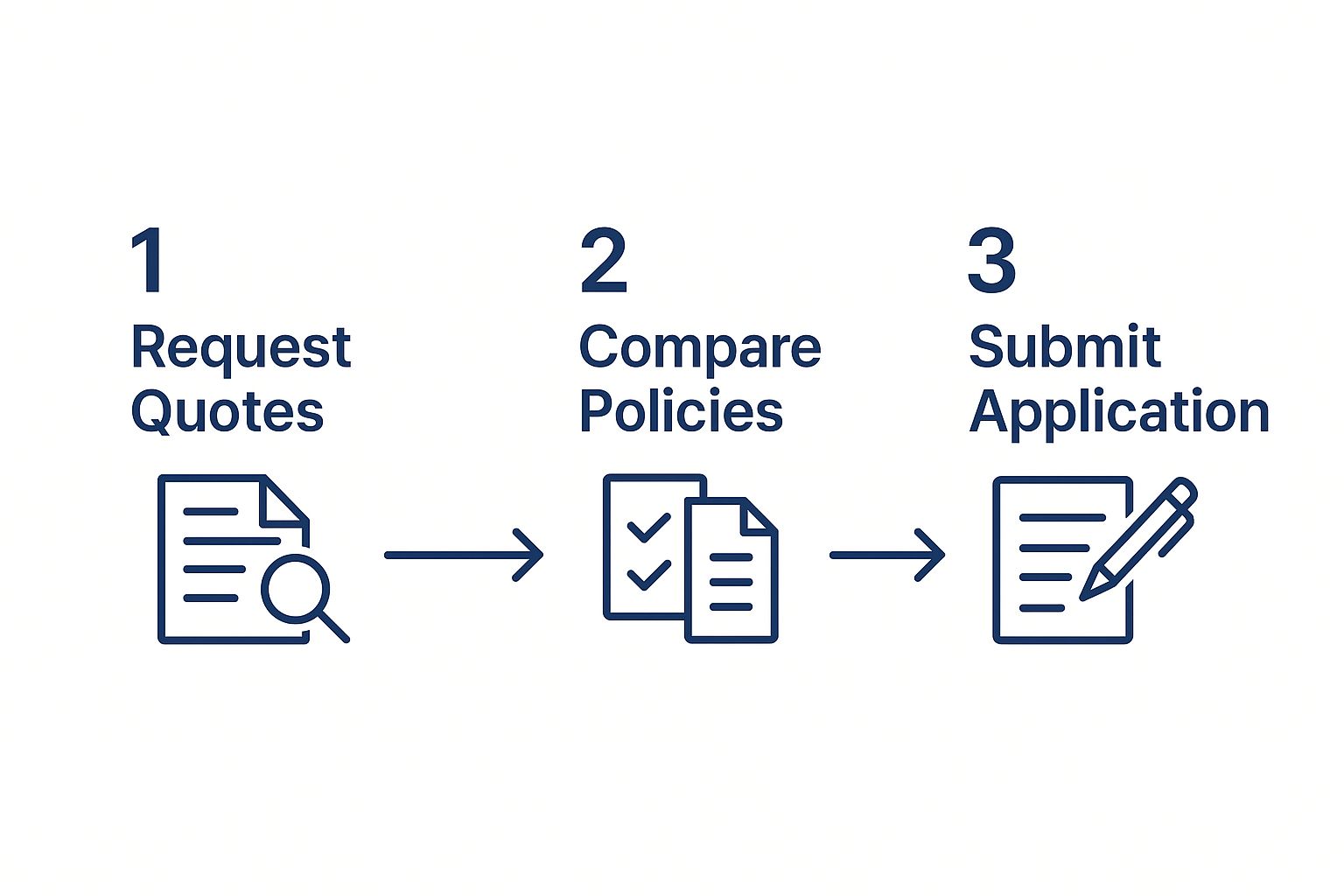

This process isn't complicated. It's just three simple phases: requesting quotes, comparing what you get, and submitting your application.

Breaking it down like this keeps you in control and prevents that feeling of being overwhelmed.

You’ve got a few solid options for finding the right fit:

- Independent Insurance Agents: These are the pros who work with tons of different carriers. They do the legwork to find the best policy for your specific situation.

- Online Marketplaces: These digital platforms are built for speed. You can get and compare multiple quotes from different companies in a matter of minutes.

- Direct Insurers: You can always go straight to the source and get a quote directly from an insurance company’s website.

A word of warning: don't just chase the lowest price. Look closely at the coverage limits, the deductibles, and—most importantly—what the policy excludes. A cheap plan that doesn’t cover your biggest risk isn't a bargain; it's a liability.

By following this simple, structured approach—assess, gather, and compare—you turn a daunting task into a series of empowering steps. This is how you land the right insurance for independent contractors and get the confidence to go all-in on growing your business.

Common Insurance Mistakes to Avoid

Getting your insurance policies in place is a massive win for your business. But the work doesn't stop there. Even the most careful contractors can fall into common traps that leave them surprisingly vulnerable.

Let’s walk through the missteps we see all the time, so you can build a safety net that actually works when you need it most.

Relying on Personal Policies

This is, without a doubt, the biggest and most dangerous mistake an independent contractor can make. It’s the assumption that your personal car or home insurance has your back for business activities. It doesn’t.

Almost every personal policy contains a business exclusion clause. This is non-negotiable fine print that says if you’re using your car for work or a client gets hurt in your home office, the insurer won’t pay. They will deny the claim, and you’ll be on the hook for every single penny.

Think of it this way: using a personal policy for your business is like bringing a garden hose to a five-alarm fire. It's just not the right tool, and the results can be catastrophic.

The fix is surprisingly simple:

- Your Vehicle: If you drive for anything beyond your daily commute—like visiting clients or making deliveries—you need a commercial auto policy. It’s built for business use.

- Your Home Office: To cover a client slipping on your steps or damage to their property, you need general liability insurance or a business owner’s policy (BOP).

A single uncovered claim can wipe out years of hard work. Believing a personal policy will cover a professional mistake is a gamble you just can't afford to take.

Underestimating Your Liability Needs

Another easy mistake is picking the lowest coverage amount just to get a cheaper premium. A $100,000 liability policy might sound like a huge number, but in the face of a serious lawsuit, it can disappear in a flash.

When that happens, you’re personally responsible for covering the rest.

Before you choose a limit, think about the absolute worst-case scenario in your line of work. What could one major mistake cost your biggest client? It's always, always better to be a little over-insured than to be even a dollar underinsured when a disaster hits.

Ignoring Policy Exclusions

Every single insurance policy has a section that clearly states what it will not cover. Ignoring these exclusions is like walking into a minefield blindfolded.

For example, a general liability policy is great for slip-and-fall accidents, but it won’t cover you if a client sues for professional negligence. That’s a completely different risk that requires a completely different policy (professional liability).

Take a few minutes to read the fine print. Better yet, ask your insurance agent to walk you through it line by line. You need to know exactly does your insurance really protect you from your specific risks. Once you understand what’s left out, you can find the right policies to fill those gaps and create truly comprehensive protection.

Contractor Insurance: Your Questions, Answered

Once you’ve got the basics down, the real-world questions start popping up. Let's tackle some of the most common ones we hear from freelancers and independent contractors just like you.

"I Work From Home. Do I Really Need Insurance?"

Yes, you absolutely do. Working remotely doesn’t mean you’re working without risk. The couch is a lot comfier than a courtroom.

Even if you never meet a client in person, your digital work—the code you write, the advice you give, the designs you create—carries professional liability. Professional Liability (E&O) insurance is non-negotiable for remote workers. It’s what protects you if a client claims your work caused them a financial loss due to an error or oversight.

And if you’re handling any client data, Cyber Liability insurance is just as critical. A data breach can happen from anywhere, and your standard homeowner's policy won't touch a business-related lawsuit.

"My Client Asked for a COI. What Is That?"

A Certificate of Insurance (COI) is just a one-page document that proves you have active business insurance. It’s a simple summary showing your policy types, coverage limits, and effective dates.

Clients ask for a COI to protect themselves. Plain and simple. By confirming you're insured, they know that if something goes wrong on a project you caused, you have the financial backing to handle it. It's a standard business practice and a sign that you’re a pro who takes your work seriously. Your insurer can usually send one over in just a few minutes.

Think of a COI as your business's insurance ID card. It’s the fastest way to show a client you’re prepared, protected, and ready to get to work. That simple piece of paper can be the difference between landing a small gig and a major contract.

"Can I Write Off My Insurance Premiums on My Taxes?"

In most cases, yes! This is one of the best perks of being your own boss. Insurance premiums are typically considered a necessary cost of doing business, which means you can deduct them to lower your taxable income.

The policies that are usually deductible include:

- General Liability Insurance

- Professional Liability (E&O) Insurance

- Cyber Liability Insurance

- Commercial Auto Insurance

Even better, premiums for self-employed health insurance can often be deducted, too. Tax laws can get tricky, though, so it's always a smart move to chat with a tax professional. They'll make sure you're getting every deduction you deserve.

At My Policy Quote, we cut through the confusion to find the right insurance for independent pros like you. Let us help you build the safety net your business deserves, so you can get back to doing what you love. Get your free, no-obligation quote today. https://mypolicyquote.com