Shopping for life insurance isn't just about ticking a box; it's a serious financial decision. The goal is to find the best possible value to protect your family's future, and that rarely means taking the first offer you see. The quotes you get for the exact same coverage can be wildly different from one insurer to the next, all because of their internal underwriting rules and how they view risk. Getting a handle on this is the first step toward making a choice you can feel good about.

Why Comparing Life Insurance Quotes Is A Must-Do

Not comparing quotes is like buying the first house you tour. You'd never do that, right? You could be leaving a ton of money on the table. Every single life insurance company has its own unique way of assessing risk, and that directly translates into the premium they charge you. One insurer might see a specific health issue as a major red flag, while another considers it a minor blip.

These differences are anything but trivial. Let’s say you’re looking for a $500,000 term policy. Company A might quote you $40 a month, but Company B comes back with $70. Over a 30-year term, you’d end up paying over $10,800 more with Company B. That's a huge difference. By comparing quotes, you find the insurer whose risk model actually benefits you, making sure you don't overpay for the protection your family needs.

Understanding The Price Gaps

The life insurance market is enormous and incredibly competitive. In fact, it's the largest slice of the global insurance industry, with premium income projected to hit roughly EUR 2,902 billion in 2024. That figure makes up more than 40% of all global insurance premiums. In a market this massive, accepting the first offer is a rookie mistake. You have to compare several quotes to lock in the best coverage for your money.

So, why do the prices vary so much? It boils down to a few key things:

- Underwriting Guidelines: Think of this as each company's internal rulebook. They use it to evaluate your age, health, lifestyle, and family history. A smoker, for instance, might get a much better deal from an insurer with a more relaxed view on tobacco use.

- Risk Appetite: Some companies are just more comfortable with certain risks. An insurer that specializes in high-risk cases might offer surprisingly competitive rates to someone with a pre-existing medical condition that other companies would penalize heavily.

- Business Focus: Sometimes, an insurer will price certain products—like a 20-year term policy—really aggressively simply because they want to grab a bigger piece of that specific market.

The real point of comparing life insurance quotes isn't just to snag the lowest premium. It's about finding the sweet spot where you get solid coverage from a stable company at a price that actually fits your budget. That's true value.

A Smarter Way to Think About Financial Security

Try to see this process as a strategic financial move, not just another tedious task. When you gather multiple quotes, you’re collecting data points that give you leverage and a much clearer picture of the market. This groundwork is absolutely vital for making a smart, well-rounded decision. If you're new to all this, our guide to affordable life insurance is a great place to get your bearings.

Ultimately, comparing quotes ensures your final decision is based on a full view of your options, not just a single, potentially overpriced offer. The table below shows just how much your personal details can change the numbers, proving that a one-size-fits-all approach just doesn't work here.

| Factor | Insurer A Quote (Monthly) | Insurer B Quote (Monthly) | Key Takeaway |

|---|---|---|---|

| Healthy 40-Year-Old | $35 | $42 | Even in perfect health, different risk models lead to price variations. |

| 40-Year-Old with High BP | $85 | $65 | Insurer B is clearly more lenient toward this specific health issue. |

| Smoker, Age 40 | $120 | $155 | Insurer A offers a significantly more competitive rate for tobacco users. |

How to Decode Your Life Insurance Quote

When you get a life insurance quote, it's natural for your eyes to dart straight to two numbers: the monthly premium and the death benefit. But stopping there is a bit like judging a car solely by its paint job—it tells you nothing about what’s under the hood. A real comparison means digging into the details that define a policy's true value and flexibility over the long haul.

You might be looking at two quotes with the exact same monthly cost, but they could offer wildly different levels of protection. The trick is knowing what to look for beyond the price tag. Making a genuine apples-to-apples comparison is all about understanding these crucial details.

Beyond the Premium and Death Benefit

Sure, the premium is what you pay and the death benefit is what your family gets, but the policy's structure is what makes it work for you when life happens. A good quote breakdown includes several key elements that need your full attention. These are the things that reveal a policy's rules, its limitations, and its hidden value.

For example, optional add-ons, known in the industry as riders, can completely change how a policy functions. They let you customize your coverage to fit your specific situation, often for just a few extra dollars a month.

- Accelerated Death Benefit Rider: This is a common one. It allows you to access a chunk of your death benefit while you're still alive if you're diagnosed with a terminal illness. Those funds can be a lifesaver for medical bills or end-of-life care.

- Waiver of Premium Rider: If you become totally disabled and can't work, this rider steps in and pays your premiums for you. It ensures your policy doesn't disappear right when you need it most.

- Child Term Rider: This lets you add a small amount of term life insurance for your kids under your own policy, usually for a very low cost.

When you're comparing quotes, look closely at which riders are included versus which ones are available for an extra cost. A policy that costs a little more but includes a waiver of premium rider could provide far more security than a bare-bones alternative.

Assessing the Insurer's Financial Strength

A life insurance policy is a promise—a long-term commitment from an insurance company to your family. That promise is only as strong as the company's ability to pay claims, potentially decades from now. This is where financial strength ratings become an absolute must-check.

Independent rating agencies like A.M. Best, Moody's, and Standard & Poor's do the heavy lifting for you by evaluating an insurer’s financial health. They assign simple letter grades (like A++, A+, or A) that act as a scorecard for the company's stability. You should always aim for insurers with top-tier ratings of 'A' or better.

Here’s a snapshot of what you might see when looking up a company's rating on the A.M. Best website.

This screenshot shows the key financial ratings for an insurance company, which are crucial indicators of its stability and reliability for policyholders.

A little bit of research here goes a long way in giving you peace of mind.

To give you a clearer picture, let's break down the most important parts of any quote. These are the components you need to line up side-by-side to get a true sense of what you're actually buying.

Key Elements to Analyze in Every Life Insurance Quote

| Component | What to Look For | Why It Matters for Comparison |

|---|---|---|

| Policy Type & Term | Is it Term, Whole, or Universal? How long does the coverage last (e.g., 20-year term)? | You must compare identical policy types and term lengths. A 20-year term quote isn't comparable to a 30-year one. |

| Premium Cost | The fixed monthly or annual payment. Note if it's guaranteed to stay level for the entire term. | While important, the premium is just one piece of the value puzzle. The lowest price isn't always the best deal. |

| Death Benefit | The total payout amount. Is it a level amount or does it change over time? | This is the core of the policy. Ensure the amount aligns with your family's financial needs. |

| Included Riders | Look for built-in benefits like an Accelerated Death Benefit or conversion options. | "Free" riders add significant value and can be a major tie-breaker between two otherwise similar quotes. |

| Optional Riders | What add-ons are available (e.g., Waiver of Premium, Child Rider) and what do they cost? | This shows the policy's flexibility. A quote might be cheaper upfront but lack the custom options you need. |

| Insurer's Rating | Check the A.M. Best, Moody's, or S&P rating. Aim for 'A' grade or higher. | This is your indicator of the company's long-term financial stability and its ability to pay a claim decades from now. |

| Conversion Options | Does the term policy allow you to convert it to a permanent policy without a new medical exam? | A good conversion privilege provides crucial flexibility if your health changes or your needs evolve. |

This table isn't just a checklist; it's a framework for thinking. By systematically looking at each of these components, you move beyond price and start evaluating a policy's real, practical value for your family's future.

Putting It All Together: A Quote Comparison Scenario

Let's walk through a real-world example. Imagine you're a young parent and you get two quotes for a $500,000, 20-year term policy. Both come in at $35 per month. They look identical on the surface, but digging in reveals a clear winner.

| Component | Quote A (Insurer Alpha) | Quote B (Insurer Beta) | Analysis for a Young Family |

|---|---|---|---|

| Monthly Premium | $35 | $35 | The cost is identical, forcing us to look deeper at the features. |

| A.M. Best Rating | A++ (Superior) | A- (Excellent) | Both are solid, but Insurer Alpha has a slight edge in financial stability. |

| Included Riders | Accelerated Death Benefit | None Included | Insurer Alpha offers a critical living benefit at no extra cost. |

| Optional Riders | Waiver of Premium ($5/mo) | Waiver of Premium ($8/mo) | Insurer Alpha provides more affordable disability protection if you choose to add it. |

In this head-to-head, Quote A from Insurer Alpha is the hands-down winner. For the exact same price, you get a policy from a more financially sound company and it includes a valuable living benefit. Even if you add the disability waiver, it's still the more affordable option. This is the kind of detailed comparison that ensures you’re not just buying a policy, but securing the best possible protection for your family.

Comparing Term vs. Whole Life Insurance Quotes

When you start looking at life insurance quotes, the first big fork in the road is almost always term versus whole life. This isn't just a minor detail; it’s a fundamental choice that shapes everything from your monthly payment to the policy's long-term purpose. Let's move past the generic pro-con lists and look at this through the practical lens of your personal financial strategy.

The right answer boils down to your goals. Are you trying to secure affordable protection while your kids are growing up and you're paying off a mortgage? Or are you looking for a permanent financial tool for something like estate planning? Nailing down that "why" is the first real step.

Matching the Policy to Your Financial Picture

It helps to think of these policies as two completely different tools designed for different jobs. Term life is like renting protection—it's highly affordable and covers you for a specific, defined period. Whole life, on the other hand, is more like owning a financial asset; it costs more upfront but is built to last a lifetime and accumulate value.

For the vast majority of families, especially those with young kids and a mortgage, term life is the workhorse. Its sole job is income replacement. If something happened to you, the policy provides a large, tax-free payout that can keep the household running, pay off the house, and make sure future goals like college are still on the table.

Whole life insurance plays a different game entirely. It's often a key piece in more complex financial puzzles, like for high-net-worth individuals planning their estates, business owners setting up buy-sell agreements, or anyone wanting to leave behind a guaranteed inheritance.

A Tale of Two Scenarios

Let’s put this into practice with a couple of real-world examples.

Scenario 1: The Young Family

Picture the Jacksons, a couple in their early 30s with two small children and a new 30-year mortgage. Their number one concern is making sure the family would be okay financially if one of them were no longer around.

- Their Goal: Get the most coverage possible for the lowest cost, specifically during their kids' dependent years.

- The Right Tool: A 30-year term life policy.

- Why It Clicks: They can lock in a $1,000,000 death benefit for a surprisingly low monthly premium. The 30-year term is a perfect match for the timeline until their house is paid off and their kids are on their own.

For the Jacksons, a whole life quote for that same million-dollar coverage would be financially crippling and completely misaligned with what they actually need. Term life gives them the massive safety net they require without wrecking their monthly budget.

Scenario 2: The Estate Planner

Now, let’s meet Ms. Davis, a 60-year-old business owner with a significant estate. Her goal is to pass her assets to her grandchildren efficiently, which means leaving behind a tax-free inheritance and covering any potential estate taxes.

- Her Goal: A permanent death benefit and a smart way to transfer wealth.

- The Right Tool: A whole life insurance policy.

- Why It Clicks: Her policy guarantees a payout regardless of when she passes away. The policy’s cash value also grows at a set rate, giving her another asset she could tap into if necessary.

For Ms. Davis, a term policy just wouldn't work. It would almost certainly expire before she passed, leaving her without any coverage right when her estate plan needed it. While there's a lot more to the difference between term and permanent life insurance, these two stories show how your personal situation is the ultimate guide.

How to Evaluate Quotes for Each Policy Type

Since these two policies have different jobs, you have to judge their quotes using different scorecards. You can't compare them apple-to-apples without knowing what to look for in each.

The most common mistake people make is applying the same checklist to both term and whole life quotes. Term is all about getting maximum temporary coverage for the lowest price. Whole life is about permanent guarantees and long-term cash value growth.

Here’s a more focused way to approach it.

When Comparing Term Life Quotes, Look At:

- Premium Stability: Is that premium locked in for the entire term? Steer clear of any policy where the price can jump up later on.

- Conversion Options: This is a big one. Can you convert the policy to a permanent one down the road without another medical exam? This feature gives you crucial flexibility if your health changes or your needs evolve.

- Available Riders: Check the cost of add-ons, like a waiver of premium rider, which keeps your policy active if you become disabled and can't work.

When Comparing Whole Life Quotes, Look At:

- Guaranteed Returns: What is the guaranteed interest rate on the policy's cash value? This is the bedrock of its performance.

- Dividend History: For participating policies, ask about the insurer's track record of paying dividends. Past performance isn't a guarantee, but a consistent history is a very good sign.

- Loan Provisions: Get the details on borrowing against your cash value. What are the interest rates? How flexible are the terms? Favorable loan rules can make the policy a much more powerful financial tool.

By using this kind of targeted approach, you can see beyond just the monthly price tag and figure out which policy structure truly supports your family's financial security. It's about investing in the right strategy, not just buying a product.

How Market Trends Impact Your Quotes

It’s easy to think a life insurance quote is all about you—your age, your health, your lifestyle. While that's a huge part of the equation, it's not the whole story. The quotes you see are also a direct reflection of what's happening in the wider economy.

Think of it this way: the price you're offered is a snapshot in time. Economic forces like interest rates and inflation are constantly at play, quietly pushing premiums up or down. Knowing how these trends work gives you a real edge, helping you understand why quotes fluctuate and when it might be the best time to buy.

The Big One: Interest Rates

By far, the most powerful economic force shaping your life insurance quote is the current interest rate environment. Insurance companies don't just stash your premium payments in a safe. They invest that money, mostly in conservative, long-term bonds, to grow their reserves.

Those investment returns are fundamental to their business. It's how they fund future death benefits and cover their own costs. So, when interest rates are high, their investments earn more, and they can afford to offer you a lower premium to win your business.

But when rates are low, the opposite happens. Their investment income shrinks, and to make sure they can still meet their obligations decades from now, they have to charge higher premiums. This effect is especially noticeable with permanent policies like whole life, which are built on the foundation of long-term investment growth.

A low-interest-rate environment often makes term life insurance look like an even better deal. Permanent policies get more expensive to compensate for weaker investment returns, making the cost gap between term and perm even wider.

This is exactly why a quote you get today might look different from one you got a few years back, even if nothing about your health has changed.

Inflation and Stock Market Swings

Inflation also has a say in the price you pay. When inflation is high, the value of money erodes over time. That $500,000 death benefit you're buying today simply won't have the same buying power in 20 or 30 years.

Insurers have to price that reality into their new policies. Plus, their own day-to-day operating costs go up with inflation, from employee salaries to rent, and that gets passed on.

The stock market’s performance can also influence certain products, especially those with an investment component like universal and variable universal life insurance. A bull market can make the non-guaranteed projections for these policies look very attractive, but market volatility introduces risk that forces insurers to be more cautious in how they price and design these products.

How to Navigate an Unpredictable Economy

The life insurance industry is always adjusting to these economic tides. We saw this in 2021 with a massive surge in life insurance sales, a level of growth the industry hadn't seen in over 40 years. With total U.S. life insurance premiums projected to hit around $15.9 billion in 2024, it's clear that economic factors are shaping what people buy and how it's priced. You can get a closer look at the key drivers behind these life insurance market trends.

So, what does this mean for you? It means you need to be strategic.

- Time Your Shopping: If you hear news about interest rates rising, that might be a great time to start shopping for quotes. Insurers will likely be more competitive with their pricing.

- Know Your Policy's Sensitivity: Universal life policies are much more sensitive to interest rate changes than term or whole life. If you're looking at a UL policy, don't be afraid to ask how current rates are impacting its projected performance.

- Lock It In: If you get a great quote for a term or whole life policy, especially when the economy feels stable, locking it in is a smart move. It protects you from any future price hikes driven by market volatility.

Understanding the "why" behind the numbers on your quote sheet moves you from simply being a consumer to being an informed buyer. You'll be in a much better position to find the right coverage at the best possible value for your family.

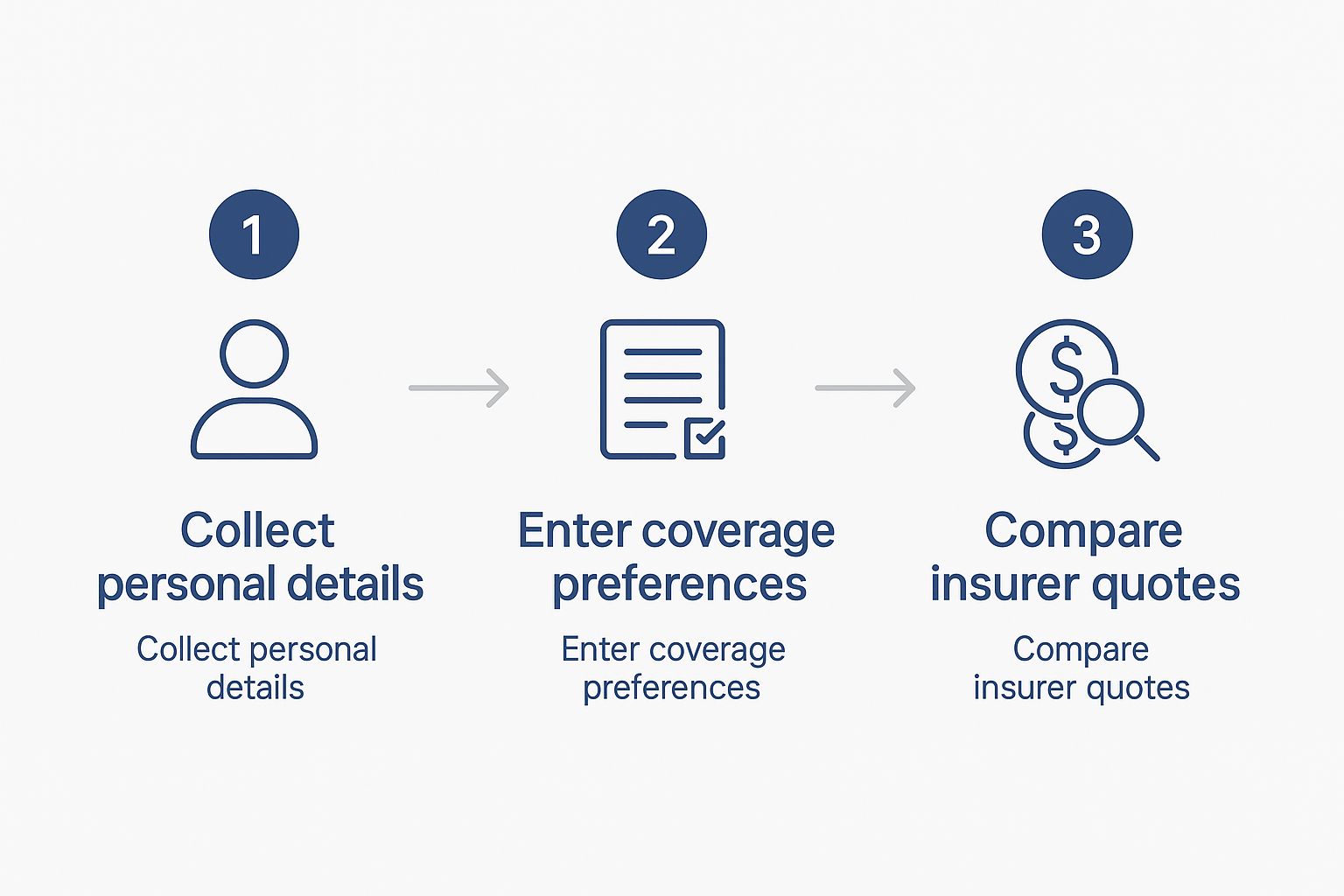

A Practical Workflow for Gathering and Comparing Quotes

Once you know the kind of policy you need, it's time to roll up your sleeves and start shopping. The key to not getting overwhelmed is having a system for collecting and evaluating your options. This isn't about gut feelings; it's about laying out the data so you can make a clear, side-by-side comparison.

There are really three main ways to get quotes, and each has its own pros and cons. The right path for you boils down to how much guidance you want versus how much of the legwork you're willing to do yourself.

Choosing Your Quote Collection Method

Your first decision is where you'll get your quotes from. This choice really sets the tone for the whole process.

-

Directly from Insurers: You can go straight to an insurance company's website or talk to one of their agents. This is a solid approach if you already have a company in mind, maybe because you bundle your auto or home insurance with them. The big drawback? It’s a huge time sink. You have to fill out the same information over and over for every single company you want a quote from.

-

Through an Independent Broker: Think of an independent broker as your personal shopper for insurance. You give them your information once, and they go out and collect a variety of quotes from the different companies they work with. Their experience is priceless, especially if you have a tricky health history or need to find a specialized insurer who might give you a better rate. The only catch is that you're relying on their recommendations, and they might not work with every single insurer out there.

-

Via Online Comparison Platforms: These websites are, without a doubt, the fastest way to get a bird's-eye view of the market. You plug in your info once and get a handful of preliminary quotes back in minutes. It's fantastic for that initial research phase to get a ballpark idea of costs. Just remember, these initial numbers are often just estimates. They can, and often do, change after you go through the official underwriting process.

This simple visual breaks down the general flow, no matter which route you take.

As you can see, the core steps—gathering your info, figuring out your needs, and comparing the offers—are the same across the board.

Building Your Comparison Spreadsheet

As quotes start rolling in, you need one central place to keep everything straight. Honestly, a simple spreadsheet is your best friend here. We're not talking about complex formulas—just a clean, organized grid that lets you spot the critical differences at a glance.

Set up your spreadsheet with a row for each insurer and columns for the most important data points. This one step will transform a confusing pile of documents into a powerful decision-making tool.

If you remember only one thing, make it this: provide the exact same information to every insurer. Any tiny difference in your health history, lifestyle, or coverage amount will throw off the quotes and make a true apples-to-apples comparison impossible.

Here are the non-negotiable columns you should have in your spreadsheet:

- Insurer Name: The company behind the quote.

- A.M. Best Rating: Their financial strength grade—super important.

- Policy Type: Is it a 20-Year Term, Whole Life, etc.?

- Death Benefit: The total coverage amount.

- Monthly Premium: The bottom-line cost.

- Included Riders: Any "freebies" like an Accelerated Death Benefit rider.

- Optional Rider Costs: The price to add extras like a Waiver of Premium.

- Conversion Options: A simple "Yes/No" and any important deadlines.

- Notes: Your personal space for red flags, unique perks, or questions to ask later.

Following this systematic approach pushes you to look past just the monthly premium and see the full value of what you're buying. By taking the time to fill this out, you’ll sidestep some of the most common mistakes when buying life insurance and be in a great position to make a choice you feel good about.

Making Your Final Decision with Confidence

You've organized the quotes and dug into the fine print. Now comes the moment of truth: making the final call. This is where you pull all your research together, shifting your thinking from finding the “lowest premium” to securing the “best value.” Let's be honest, the cheapest policy isn't the best one if it’s tied to an unreliable company or misses key features you actually need.

True confidence comes from finding that sweet spot between the monthly premium and the insurer's long-term reliability. A life insurance policy is a promise, plain and simple. You need to be certain the company can keep that promise, potentially decades down the road. It means looking past the price tag to weigh the things that define an insurer's character and dependability.

Moving from Cost to Value

The final hurdle in comparing life insurance quotes is evaluating the company itself. A low premium might catch your eye, but it’s worthless if the insurer is known for frustrating customer service or dragging its feet on claims. The last thing your family needs is a bureaucratic battle during an already heartbreaking time.

Think of these factors as non-negotiable:

- Financial Stability: Go back to that A.M. Best rating. An ‘A’ grade or higher is the gold standard, signaling the company has the financial muscle to pay out claims without a hitch.

- Customer Service Reputation: What are actual policyholders saying? Scour reviews and ratings to see how the company handles everyday inquiries, policy adjustments, and—most importantly—complaints.

- Claims-Paying History: A little digging into the company's track record for processing death benefits can tell you a lot. A compassionate and efficient claims process is a massive part of a policy's true worth.

A life insurance policy's real value isn't measured by its price tag, but by the peace of mind it delivers. That peace of mind is directly linked to the insurer’s reputation for integrity and reliability.

The Final Checkpoint

Before you put pen to paper, run through one last mental checklist. This is your chance to confirm the policy aligns with your life today and where you see yourself in the future. Answering these questions can help you lock in your choice with total certainty and clarify what exactly does life insurance cover for your specific plan.

- Is the premium 100% guaranteed to stay the same for the entire term?

- Are the conversion options flexible if my circumstances change later on?

- Have I double-checked all the riders—both included and optional—to make sure they add real value?

- Does this insurer’s reputation genuinely give me confidence for the long haul?

It’s also smart to consider the bigger picture. In 2025, for instance, Marsh’s Global Insurance Market Index highlighted several quarters of falling insurance rates worldwide, driven by fierce competition. While that’s great for getting a competitive price, the industry is still navigating economic uncertainty. This could lead to unpredictable premium shifts down the line, making it all the more important to lock in a solid rate with a stable provider now. You can read the full analysis on global insurance market trends on Marsh.com.

Frequently Asked Questions

It's only natural to have questions pop up when you're sorting through life insurance quotes. Finding clear answers is what gives you the confidence to pick the right policy.

Key Questions Answered

How often should I really be shopping for life insurance?

A good rule of thumb is to take a fresh look at your options every few years, but you absolutely should do it after any major life event. Think about it: getting married, welcoming a new baby, buying a house, or even landing a big promotion all shift your financial responsibilities. Re-shopping ensures your coverage still makes sense for your new reality and that you're getting a competitive price.

Will pulling all these life insurance quotes hurt my credit score?

Nope, not at all. Requesting life insurance quotes has zero impact on your credit score. Insurers run what’s called a "soft" credit inquiry, which you can see on your own report, but lenders can't. So, go ahead and gather as many quotes as you need to feel comfortable—it won't penalize you.

The single biggest mistake when comparing life insurance quotes is focusing only on the monthly premium. A cheaper policy might have serious drawbacks, like fewer riders, poor conversion options, or an issuer with weak financial stability. Always compare the complete value, not just the price.

What's the most common mistake people make when comparing quotes?

Hands down, the biggest misstep is getting tunnel vision and only looking at the premium. It's so easy to do, but that narrow focus means you might miss the bigger picture. A slightly cheaper quote could come from a company with a shaky financial strength rating or be missing crucial features, like a waiver of premium rider. Your goal should always be to find the best overall value—a balance of affordable cost, solid coverage, and an insurer you can count on.

Ready to find a policy that truly fits your life and your budget? The experts at My Policy Quote can help you compare options from top-rated insurers in minutes. Get your free, no-obligation quotes today and secure the peace of mind your family deserves. Visit us at https://mypolicyquote.com.