When it comes to finding a life insurance policy that won't break the bank, one choice stands out above all others: term life insurance.

For most families, term life hits the sweet spot. It provides a huge amount of coverage for a specific window of time—like the years you're paying off a mortgage or raising your kids—but costs a fraction of what a permanent policy would. It’s the simplest, most effective strategy for getting affordable financial protection.

What Really Drives Your Life Insurance Cost

Before you even think about getting quotes, you need to understand how insurers look at you. It’s like they’re putting together a puzzle, with each piece representing a part of your life. The final picture tells them how much risk they’re taking on by insuring you.

The more risk they see, the higher your monthly premium will be.

Most people know that age and health are the big ones, but the list goes on. Everything from your job to how you spend your weekends can move the needle on your final price. Once you know what these drivers are, you have a much better idea of what you can (and can't) control to lock in a genuinely low rate.

The Two Pillars of Pricing: Health and Age

Your health is, without a doubt, the single biggest factor. When an insurer puts you through medical underwriting, their goal is to get a clear picture of your life expectancy. They’ll dig into your medical records, see what prescriptions you take, ask about your family's health history, and almost always require a medical exam with blood and urine tests.

Age is right there beside it. The logic is simple: the younger you are when you buy a policy, the longer you’re likely to pay premiums before the company has to pay out a claim. It’s a numbers game.

A healthy 30-year-old might pay just $25-$35 a month for a solid term policy. But a 50-year-old in similar health could easily be looking at $75-$100 or more for the exact same coverage.

Here’s the honest truth: Time is your best friend when buying life insurance. Locking in a rate while you're young and healthy is the single most powerful move you can make to secure a low premium for decades.

Beyond the Basics: Lifestyle and Other Factors

Insurers don’t just stop at your physical health. They want to know about your lifestyle choices and personal history, because those also paint a picture of risk.

Here's what else they're looking at:

- Tobacco and Nicotine Use: This is a huge one. If you smoke or use any nicotine products, expect to pay 2 to 4 times more than a non-user.

- Driving Record: A history of DUIs, reckless driving citations, or a stack of speeding tickets signals high-risk behavior to an insurer.

- High-Risk Hobbies: Do you love skydiving, scuba diving, or rock climbing? These activities can lead to higher premiums or even special exclusions in your policy.

- Your Job: A quiet desk job is viewed as much lower risk than being an airline pilot, a commercial fisherman, or a logger.

To get a better handle on these elements, here’s a quick breakdown of what insurers are weighing.

| Key Factors Influencing Your Life Insurance Premium | ||

|---|---|---|

| Factor Category | Specific Elements | Impact on Cost |

| Health Profile | Medical history, current conditions, prescription drugs, family health history | High Impact: The single most significant driver of your premium. |

| Age & Gender | Your current age and assigned sex at birth | High Impact: Younger applicants get significantly lower rates. |

| Lifestyle Choices | Smoking/nicotine use, alcohol consumption, high-risk hobbies | High Impact: Smokers can pay up to 4x more; risky hobbies also raise rates. |

| Personal Data | Driving record (DUIs, accidents), credit history, occupation | Medium Impact: A poor driving record or a dangerous job increases your premium. |

| Policy Details | Coverage amount (death benefit) and policy length (term) | Medium Impact: Higher coverage and longer terms cost more. |

This table isn't meant to be exhaustive, but it covers the main puzzle pieces an underwriter uses to build your risk profile. The more favorable these factors are, the more affordable your coverage will be.

Why Term Life Is the Champion of Affordability

The type of policy you choose has a massive effect on your monthly cost. This is where the difference between term and whole life insurance becomes so important. If you want to dive deep into the pros and cons, you can explore our guide on term versus whole life insurance to see which one truly aligns with your goals.

Term life insurance is pure, straightforward protection. You pay for coverage for a set period—say, 10, 20, or 30 years. If you pass away during that term, your family gets the money. That’s it. There’s no complicated cash value or investment component, which is exactly why it’s so affordable.

On the other hand, whole life insurance is built to last your entire life and bundles in an investment-like cash value account. Because it does two things at once, the premiums are dramatically higher—often 5 to 15 times more expensive than a comparable term policy. The proof is in the numbers: term life makes up over 85% of individual policies sold each year because people are looking for real, affordable protection.

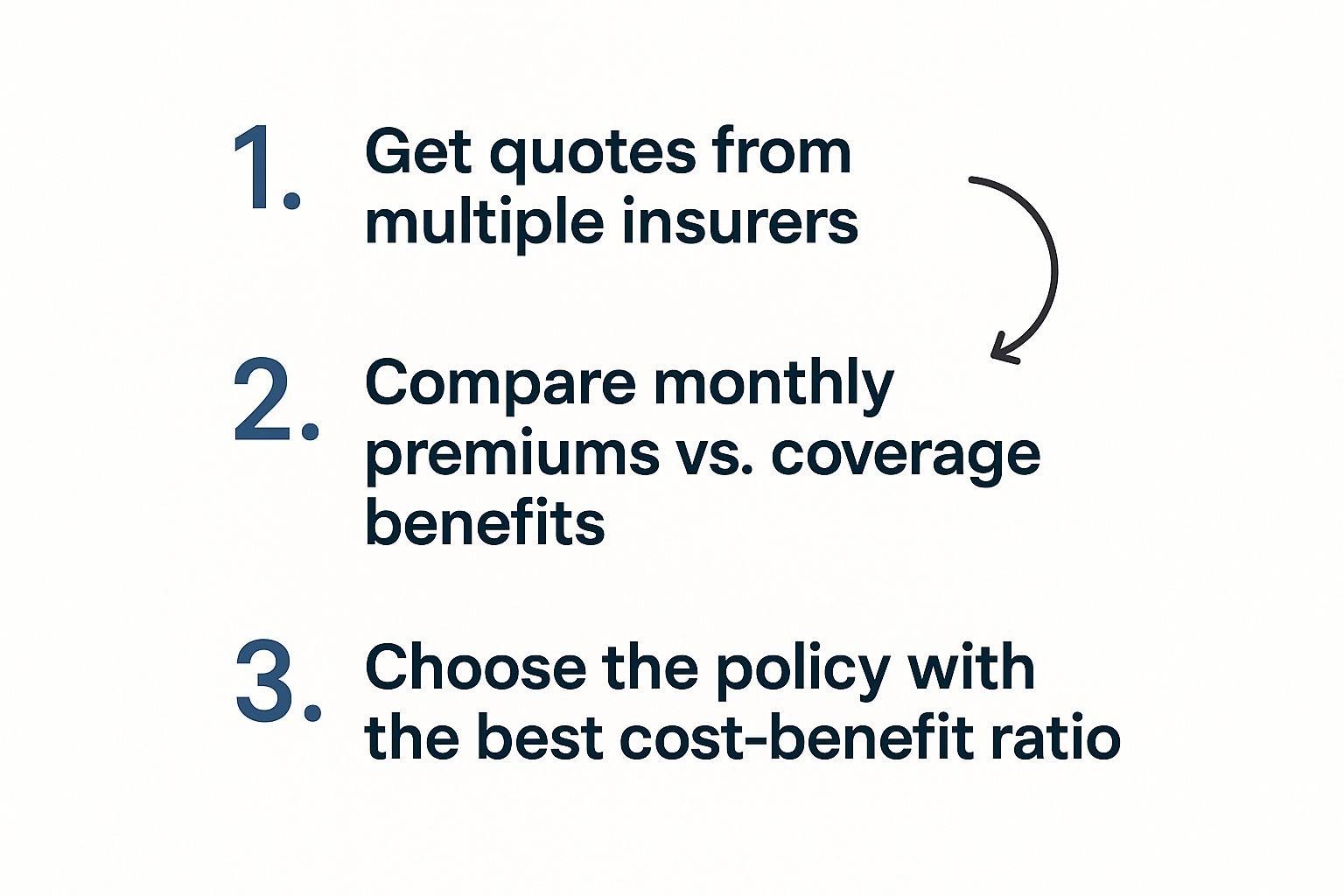

A Smarter Way to Compare Insurance Quotes

Getting the best price on life insurance isn’t just about collecting a bunch of quotes. It's about knowing what you’re looking at.

A stack of ten different price points means nothing if you can’t see what’s behind each number. This is where a smart shopping strategy really pays off, separating those who find a decent deal from those who lock in the best low cost life insurance policy for their family.

Your first move is deciding how you want to shop. The two main paths are working with an independent broker or using a direct online tool. There's no single right answer here—it all comes down to what you’re comfortable with and what your life looks like.

Broker vs. Online Tool: Which Is Right for You?

An independent broker is a licensed pro who has relationships with multiple insurance companies. Their entire job is to learn about your situation—your health, your finances, your family—and then go to bat for you in the market.

This is a fantastic route if you have a complicated health history, a high-risk job, or you just want an expert to cut through the noise. A good broker knows which companies are more forgiving about specific health conditions, saving you a world of time and potential rejection letters.

On the other hand, direct online tools are all about speed and control. You enter your information and get a handful of quotes back in minutes. This path is perfect if you’re in good health, your needs are straightforward, and you feel confident managing the process on your own. The responsibility, however, is all on you to make sure the quotes you’re comparing are for the exact same coverage.

Luckily for all of us, the insurance market is incredibly competitive right now. A recent softening trend in global insurance pricing means companies are fighting for your business. We’ve seen consecutive quarters of declining rates, which puts you in the driver’s seat. This competition is your best ally in finding a low cost life insurance policy with great terms. For more on this, you can explore the complete global insurance market report from Marsh.

Making an Apples-to-Apples Comparison

Once the quotes start coming in, the real work begins. Remember, a lower price isn’t always a better deal if it comes with less coverage or a critical exclusion hiding in the fine print.

To make a true comparison, you need to get organized. Create a simple spreadsheet or even just a list for each quote and track these key details:

- Insurance Company & AM Best Rating: The company's name and its financial strength rating (you want to see A, A+, or A++).

- Policy Type: Is every quote for Term Life? Make sure.

- Term Length: Are you comparing a 20-year term to another 20-year term? Don’t get them mixed up.

- Coverage Amount: The death benefit must be identical across the board, for example, $500,000.

- Monthly Premium: The actual price you’ll pay each month.

I’ve seen it happen countless times: someone gets excited about a super-low premium, only to realize later it was for a 10-year term when they really needed a 30-year policy. Always, always verify the core details first.

Look Deeper Than Just the Price

With the basics lined up, it’s time to dig into the details that truly separate one policy from another. This is where you can find valuable perks or spot hidden limitations.

1. Check for Conversion Privileges

Does the policy let you convert your term coverage into a permanent one later on without a new medical exam? This is a hugely valuable option. If your health takes a turn down the road, this feature ensures you can keep your coverage.

2. Scrutinize Riders and Add-Ons

Riders are extra benefits you can add to a policy, usually for an extra cost. Some common ones include:

- Accelerated Death Benefit: Lets you access part of your death benefit early if you’re diagnosed with a terminal illness. Many top-tier policies include this for free.

- Waiver of Premium: If you become totally disabled and can't work, this rider pays your premiums for you. It costs a little more, but it’s an incredible safety net.

Make sure you’re only comparing policies with the riders you actually want. If one quote looks cheap but is stripped bare, while another is a few dollars more but includes valuable protections, the pricier one might be the better deal.

3. Read the Exclusions Carefully

Every policy has them. Exclusions are situations where the company won't pay the death benefit. The most common is the "suicide clause," which usually applies for the first two years of the policy.

More importantly, check for exclusions related to high-risk hobbies. If you’re a pilot or a scuba diver, you need to be upfront about it during your application. Hiding it might get you a lower quote now, but it could lead to a denied claim when your family needs it most. Honesty is always the best policy.

How Your Health Profile Impacts Your Premium

When an insurance company looks at your application, they're not just seeing numbers on a page. They're trying to get a clear picture of your future risk, and your current health is their most reliable guide.

This is actually fantastic news. It means your health is the one factor you can directly control to lower your life insurance costs. Unlike your age, your health isn’t set in stone. Small, documented improvements can make a massive difference in how an underwriter sees you, leading to very real savings over the life of your policy.

The Financial Power of a Healthier You

Think of life insurance rate classes like airline seating: Preferred Plus, Preferred, Standard Plus, and Standard. Your goal is to get into the best class possible. Why? Because each step up can slash your premium by 25% or more.

So, how do you climb that ladder? It’s often simpler than you’d think.

Quitting smoking is, without a doubt, the single biggest move you can make. If you’ve been tobacco-free for at least a year, you can move from sky-high "Smoker" rates to far more manageable "Non-Smoker" rates. The difference is staggering—smokers often pay 2 to 4 times as much for the exact same coverage. Over a 30-year term, that one decision could save you tens of thousands of dollars.

Here’s a real-world example: A 45-year-old client of ours, Mark, was a long-time smoker and got a quote for about $180/month for a $500,000 policy. He decided to quit. One year later, he got re-evaluated, and his new premium was just $65/month. That simple change saved him $41,400 over his 30-year policy.

The Health Metrics That Matter Most

Beyond tobacco use, underwriters zoom in on a few key health stats that you can actively improve. Showing a positive trend in these areas—even over just 6-12 months before you apply—shows you're responsible and lowers your risk profile in their eyes.

1. Body Mass Index (BMI)

Insurers use your weight-to-height ratio as a quick reference point. While it’s not the whole story, a BMI outside the "healthy" range can easily knock you down a rate class. Losing even a little bit of weight to get your BMI into a better category can lead to a much better offer.

2. Blood Pressure

High blood pressure is a major red flag for heart-related risks. If your doctor has recommended lifestyle changes or medication, following that advice is key. When you can provide records showing your blood pressure is well-managed, you’re in a much stronger position to qualify for preferred rates.

3. Cholesterol Levels

Just like blood pressure, high cholesterol (especially the "bad" LDL kind) points to potential health troubles down the road. Working with your doctor to lower your numbers through diet, exercise, or medication is a powerful move. Proving you've made progress over time can be a great negotiating tool. For younger people, building these healthy habits early can set you up for a lifetime of savings. You can learn more in our guide to life insurance for young adults.

Nailing Your Application and Medical Exam

After you've put in the work, it's time to make sure your medical exam shows off your progress. This is your moment to lock in the great rate you've earned.

Here’s a simple checklist to follow in the days before your exam:

- Get Your Paperwork Ready: Have your doctor's contact info, a list of all your medications (with dosages), and dates of any recent surgeries or check-ups on hand.

- Hydrate, Hydrate, Hydrate: Drink plenty of water in the days leading up to the exam. It makes the blood draw easier and can help produce a more accurate urine sample.

- The 48-Hour Rule: For two days before your appointment, steer clear of intense exercise, salty or fatty foods, and alcohol. These can temporarily spike your blood pressure and throw off your cholesterol readings.

- The 12-Hour Fast: Most exams require you to fast for 8-12 hours. That means no food and only water to drink. Yes, skipping that morning coffee is tough, but the caffeine can artificially raise your blood pressure.

By taking these steps, you’re not just crossing your fingers for a low cost life insurance policy—you’re actively building your case for one. You're showing the insurer the best, most accurate version of your health, and that's how you secure a premium you can feel great about.

Using Group Policies to Your Advantage

Sometimes the easiest and most affordable life insurance isn't something you have to hunt for—it's waiting right where you work. Many companies offer group life insurance as a perk, and frankly, it's one you should absolutely take advantage of.

Why is it so cheap? Often, it's completely free. Insurers spread their risk across the entire company roster, not just one individual. This lets them skip most of the intense underwriting, making it a simple and cost-effective benefit for employers to offer.

What Does Group Coverage Actually Look Like?

When you enroll in your company’s plan, you'll typically get a death benefit equal to one or two times your annual salary. So, if you earn $60,000 a year, your employer might hand you a $60,000 or $120,000 policy without you paying a single dime.

Many employers also give you the option to buy more coverage, often called "supplemental" or "voluntary" life insurance. You pay for this extra amount out of your paycheck, but the rates are usually much better than what you could find on your own because you're still part of that low-risk group.

Key Takeaway: If your employer offers free basic group life insurance, sign up. It’s a no-brainer and instantly creates a foundational layer of protection for your loved ones.

This is a massive part of the insurance world. In just one recent quarter, group life insurance premiums hit around US$857 million. That number shows just how many families rely on this benefit. Its affordability is a direct result of that large-scale risk pooling.

The Big Catch with Workplace Policies

Group insurance is a fantastic starting point, but it comes with a major string attached: it's almost always tied to your job. This is the part you can't afford to overlook.

Here’s what that really means:

- It's Not Portable: If you leave your job—quit, get laid off, or retire—that coverage usually disappears. You can't take it with you.

- You Can Have Gaps: When you switch companies, you might face a waiting period for new benefits to kick in, leaving your family completely unprotected in the meantime.

- The Amount Isn't Enough: A policy worth one or two times your salary is a nice gesture, but it’s rarely enough to pay off a mortgage, fund college, and replace your income for decades.

This is exactly why financial experts will tell you, time and time again, not to depend solely on your employer's plan. Think of it as a great supplement, but never your only safety net. For parents, making sure you have enough coverage is non-negotiable. Our comprehensive guide to life insurance for parents breaks down how to figure out what your family truly needs.

Consider your group policy the solid ground floor of your financial protection plan. It’s a valuable, low-cost place to start. The next move is to build on top of it with a personal term life policy that you own and control, one that stays with you no matter where your career takes you.

Navigating the Final Application Steps

You’ve done the hard work. You compared quotes, weighed the pros and cons, and picked an insurer that feels right. Now it’s time to cross the finish line. The final application and medical exam are the last two hurdles standing between you and locking in that great rate.

Getting this part right is absolutely crucial. A simple mistake, like missing information or a poorly timed medical exam, can cause frustrating delays. Worse, it could mean getting a higher premium than you were quoted. Think of it as your final interview—a chance to show the insurer you’re the low-risk applicant they believe you are.

Preparing for Your Application

To make the process as smooth as possible, get your documents and information together before you start. Trust me, scrambling to find details at the last minute is stressful and where mistakes happen.

Here’s a quick checklist of what you'll almost certainly need:

- Personal ID: Your driver's license number and Social Security number.

- Medical History: The names and contact info for any doctors you’ve seen in the last five years.

- Prescription Details: A list of all your current medications, including the name, dosage, and who prescribed them.

- Family Health History: Be ready to answer questions about the health of your immediate family (parents and siblings), especially regarding major illnesses like heart disease or cancer.

Having all this organized and ready will make the paperwork a breeze. It also sends a signal to the insurer that you’re serious and prepared, which never hurts.

This is the core process for securing an affordable policy, from getting those initial quotes to making your final choice.

The key takeaway? Finding a low-cost life insurance policy isn't about luck. It's a structured process where each step builds on the last, guiding you to the best possible value.

Mastering the Medical Exam

The medical exam is where your quoted rate gets real. The examiner's report gives the underwriter the final, objective data they need to make a decision. Your goal is to provide the most accurate—and favorable—snapshot of your health.

Here are a few pro tips for the 48 hours leading up to your exam:

- Hydrate, Hydrate, Hydrate: Drink plenty of water in the day or two beforehand. Good hydration makes for an easier blood draw and helps ensure your lab results are accurate.

- Skip the Intense Workout: Strenuous exercise can temporarily elevate your liver enzymes and protein levels, which could send a false red flag. Take it easy for a day or two.

- Watch What You Eat: Stay away from overly salty or fatty foods. They can temporarily spike your blood pressure and cholesterol readings.

- Avoid Morning Coffee & Alcohol: Both caffeine and alcohol can throw off your results. It's best to fast for at least 8-12 hours before your appointment, sticking to just water.

I once had a client whose blood pressure was slightly elevated during his exam, which bumped him down a rate class. The culprit? Two large coffees he drank on the way to the appointment. It’s a tiny detail that can have a huge financial impact.

Once your policy is approved and active, it’s also smart to make sure it works with your overall estate plan. A policy without a clear beneficiary plan can create headaches for your loved ones. To get a better handle on this, you can read our guide on life insurance without a will and see how to properly integrate your coverage.

By navigating these final steps with a little care, you can secure the low-cost policy you worked to find and ensure it truly protects your family when they need it most.

Your Top Questions About Affordable Life Insurance, Answered

Even after you've done your homework, compared quotes, and prepped for the medical exam, it’s completely normal to have a few questions rattling around in your head. Life insurance can feel like a maze, and you want to be 100% certain you're making the best move for your family's future.

Let's cut through the noise. We’ve pulled together the most common questions we hear from people just like you, all on the hunt for a genuinely low cost life insurance policy. Getting straight answers will give you the confidence to lock in the right coverage.

Is a No-Exam Policy a Shortcut to a Good Deal?

It's tempting, isn't it? The idea of skipping the medical exam and getting coverage in days, not weeks, sounds amazing. These "no-exam" or "simplified issue" policies definitely win on convenience. But that speed almost always costs you more.

When an insurer skips the exam, they're taking a bigger gamble on your health because they have less information. To make up for that unknown risk, they charge higher premiums. If your main goal is locking in the absolute lowest rate and you're in decent health, a traditional, fully underwritten policy (the kind with a medical exam) is almost always the better financial choice.

Think of a no-exam policy as paying a premium for convenience, not for value. It's a fantastic tool for those who need coverage right now or have a serious aversion to medical tests, but it's not a secret backdoor to the cheapest rates.

How Often Should I Revisit My Policy?

Your life changes, so your life insurance should keep up. A great rule of thumb is to give your policy a quick review every 3 to 5 years, or whenever a major life event shakes things up.

What counts as a major event? Things like:

- Getting married or divorced

- Welcoming a new baby or adopting a child

- Buying a new house and taking on a bigger mortgage

- Getting a significant promotion or salary bump

But here’s the pro tip: you should absolutely shop for a new policy if your health has gotten better. Have you quit smoking for a few years? Lost a good amount of weight and kept it off? Finally got your blood pressure under control? These kinds of improvements could bump you into a much better rate class, potentially saving you a ton of money on a brand-new policy.

Can I Make My Current Policy Cheaper?

Once a term life policy is active, your premium is locked in for the whole term. You can't just call up the insurer and ask for a discount. But that doesn't mean you're stuck if your budget or needs have changed.

First, like we just mentioned, if your health is better now, your best move is to shop around. If you qualify for a better rate, you can simply accept the new, cheaper policy and cancel the old one. Easy.

Second, you can ask your current insurer to lower your coverage amount. Let's say you bought a $1 million policy back when you had a huge mortgage and young kids. If you've since paid down that debt, you might only need $500,000 in coverage today. Reducing your death benefit will directly reduce your monthly premium. Just be sure to confirm with your provider that your specific policy allows for this.

Does a Longer Term Automatically Mean a Higher Premium?

Yes, it does. For the same death benefit, a 30-year term policy will have a higher monthly payment than a 10-year term. From the insurer's perspective, they're guaranteeing your rate for a much longer time, which increases their risk.

However—and this is critical—choosing the longer term from the very beginning is almost always the smarter, more cost-effective strategy.

Let’s look at a 30-year-old who needs coverage for the next three decades.

| Coverage Strategy | How It Works | The Financial Reality |

|---|---|---|

| Option A: One 30-Year Policy | Buys a single 30-year term policy at age 30. | Locks in a low rate based on their youth and current health for the entire 30 years. Predictable and affordable. |

| Option B: Three 10-Year Policies | Buys a 10-year policy at age 30, another at 40, and a third at 50. | The premium will jump dramatically at each renewal. The rate at age 40 will be higher, and the rate at 50 will be significantly higher, reflecting their older age and any new health issues. |

Locking in that 30-year term today is far cheaper in the long run than trying to stitch together coverage over time. You protect yourself against future price hikes and, more importantly, the risk of becoming uninsurable if your health changes down the road.

Finding the right low cost life insurance policy is one of the most powerful and loving financial decisions you can make for your family. At My Policy Quote, we simplify the process, letting you compare quotes from top-rated insurers so you can get the protection you need at a price that fits your life.