The big question on many people's minds is, "Can I actually have two life insurance policies?" The answer is a clear and simple yes. Not only is it possible, but it’s a smart financial move that many people use to create a stronger, more flexible safety net for their families. It's not some kind of loophole; it's just good planning.

Yes You Can Own Multiple Life Insurance Policies

Think of your financial protection like a toolkit. A good contractor wouldn’t use a hammer for every single job, right? They pick the right tool for the task. The same idea applies here. You can use different life insurance policies to cover different financial goals. This is often called "insurance stacking" or "laddering," but it really just means layering your coverage to match the different stages of your life.

For example, you might have one policy that’s big enough to cover your 30-year mortgage. At the same time, a second, smaller policy could be there just to make sure your kids' college tuition is paid for, no matter what happens. This approach is much more efficient than just buying one massive policy that you might not even need in 20 years.

Tailoring Coverage to Your Life

The ability to own more than one policy is a cornerstone of modern financial planning. There are no laws against it in places like the United States, Canada, or the United Kingdom. People do it all the time to meet specific needs—like pairing a big term life policy to cover debts with a smaller whole life policy meant for leaving an inheritance.

This strategy gives you incredible flexibility. Life changes. The policy you bought in your 20s probably isn't enough once you've bought a house, had kids, or started a business. Adding a second policy is often the smartest way to fill those new gaps without having to give up your original—and probably cheaper—coverage.

The real magic is that each policy has its own job. By matching different policies to different financial responsibilities, you build a safety net that's custom-fit for your family.

To give you a quick overview, here's a look at the common reasons people choose to hold more than one policy.

Reasons for Owning Two Policies at a Glance

| Aspect | Key Consideration |

|---|---|

| Covering Specific Debts | Use one policy for the mortgage and another for smaller loans like car or student debt. |

| Income Replacement | One policy provides a lump sum while another might offer a steady stream of income. |

| Business Needs | A personal policy protects your family, while a business policy protects your company. |

| Laddering for Changing Needs | As one term policy expires (e.g., after kids graduate), another continues for the mortgage. |

| Estate Planning | A whole life policy can be used to cover estate taxes or create an inheritance. |

| Locking in Low Rates | Keep an affordable policy from your younger years and add a new one for new needs. |

This table shows just how versatile this strategy can be, allowing you to fine-tune your financial protection as your life evolves.

You can get a deeper dive into structuring your coverage in our guide on having more than one life insurance policy. It’s all about being targeted, ensuring every premium dollar is working hard to protect what matters most.

Why Smart Financial Planning Often Involves Two Policies

Knowing you can have two life insurance policies is one thing. Understanding why you'd want to is where truly smart financial planning begins. Your life doesn't stand still, so your financial safety net shouldn't either.

The most common reason for adding a second policy is simple: life changed.

Maybe you started with a small policy from your first job. It seemed like enough at the time, but it rarely keeps pace with your growing responsibilities. All of a sudden, you have a mortgage, a growing family, or a new business venture. These new obligations create financial gaps your original policy was never designed to fill.

For instance, a young professional might have a basic term policy through her employer. But after buying a home and welcoming a child, she realizes that small group policy wouldn't even cover half the mortgage, let alone support her family for years. Adding a larger, private term policy is the logical next step to protect her new assets and loved ones.

Matching Policies to Specific Goals

Think of each policy as having a specific job to do. You can assign one policy to cover your mortgage and a separate one to make sure your kids' education is funded. This targeted approach is often much more efficient and affordable than buying one massive policy meant to cover everything at once.

Here are the key drivers that lead people to get more coverage:

- Covering New Debts: A new mortgage, a business loan, or even significant student debt often requires a fresh layer of protection.

- Adjusting for a Higher Income: As your salary grows, so does the financial hole your family would face. A second policy helps replace that larger income.

- Supplementing Employer Coverage: Group life insurance is a great perk, but it's often small and you can't take it with you if you leave your job. A private policy puts you in control.

- Separating Financial Goals: You can earmark one policy for paying off debts and another purely for leaving a tax-free inheritance to your family.

A Common Strategy for Modern Families

This strategy is more common than you might think. As people have become more financially savvy, they've realized that a one-size-fits-all policy is rarely the best fit. In fact, data shows that around 15-20% of insured individuals now hold two or more life insurance policies.

This trend reflects a shift toward more detailed financial planning, where coverage is matched to specific life stages and needs. A small business owner is a perfect real-world example. He might have a personal term life policy to protect his family’s home and lifestyle. At the same time, he could have a second, separate policy as part of a buy-sell agreement with his business partner, making sure the company can continue smoothly if one of them passes away.

Deciding what type of coverage to add depends heavily on your age and current financial situation. To get a better feel for what might work for you, check out our guide on choosing the best life insurance in your 30s, 40s, and 50s.

Ultimately, having multiple policies is about creating a responsive, multi-layered financial defense for the people who count on you most.

Combining Different Types of Life Insurance Policies

Think of your financial strategy like a toolkit. You wouldn’t grab a hammer to tighten a screw; you find the right tool for the right job. It’s the same with life insurance. When people ask if you can have two life insurance policies, the answer isn't just "yes"—it's that combining different types can solve different problems.

This approach gives you a powerful, personalized safety net. Instead of being locked into a single, one-size-fits-all policy, you can mix and match coverage that truly aligns with where you are in life. This is where holding multiple policies really starts to make sense.

The Classic Combo: Term Plus Whole Life

One of the most common and effective pairings is a term life policy combined with a whole life policy. Each one plays a distinct role, and together they create a balanced, robust financial plan.

A term life policy is your temporary shield. It’s designed for your biggest, but time-sensitive, financial hurdles. Think of it as protection for:

- Your mortgage: A 30-year term policy can make sure your family’s home is paid off, no matter what.

- Raising your kids: A 20-year policy can replace your income until your children are grown and financially independent.

- Major debts: It can cover business loans or student debt that have a clear end date.

At the same time, a whole life policy acts as your permanent foundation. It’s the bedrock of your financial security that never expires as long as you pay the premiums, and it even builds cash value over time. This makes it perfect for lifelong needs, like covering final expenses, leaving a guaranteed inheritance, or funding estate planning.

By pairing these two, you get the best of both worlds: affordable coverage for your largest, temporary needs and a permanent foundation of security that grows right alongside you. This strategy ensures you’re not overpaying for coverage you only need for a certain number of years.

Getting Smart with the Laddering Strategy

Another brilliant way to use multiple policies is a technique called “laddering.” This is where you stack several term policies with different expiration dates. The goal is to create customized coverage that shrinks as your financial responsibilities decrease over time.

Instead of just buying one massive 30-year, $1 million policy, you could structure your coverage like this:

- Policy 1: A 10-year term for $500,000 (to cover your highest-need years when the kids are young).

- Policy 2: A 20-year term for $300,000 (to continue covering the mortgage and income replacement).

- Policy 3: A 30-year term for $200,000 (to protect your spouse all the way into retirement).

As each shorter-term policy expires, your total coverage—and your total premium—drops. Laddering makes sure your insurance always matches your actual need, preventing you from paying for protection you no longer require. It’s an incredibly cost-effective way to get the right amount of coverage at every stage of your life.

Navigating the Application for a Second Policy

Applying for a second life insurance policy is surprisingly straightforward, but it all comes down to one simple, non-negotiable rule: be completely honest. When you decide you need more coverage, you must tell the new insurer about every other life insurance policy you already have. This isn't a trick question on the application; it’s a standard part of the process that ensures transparency.

There’s a good reason for this. Insurers need the whole story to figure out your total "insurable interest." That’s just industry-speak for the legitimate financial need for life insurance based on your income, debts, and overall financial picture. They use this to prevent people from being over-insured, making sure the death benefit serves as a safety net, not a lottery win.

What Underwriters Look For

When an underwriter gets your application for another policy, they're doing more than just reviewing your medical history. They’re putting on their financial analyst hat to make sure the total coverage you’re asking for makes sense. Think of it like a bank making sure you can handle another loan before approving it.

Their main job is to answer one question: does the combined death benefit from all your policies align with your actual financial situation?

Here's what they’ll be looking at:

- Your Annual Income: This is the big one. Most companies will cap your total coverage at a multiple of your salary, usually somewhere between 10 to 30 times what you make in a year. That multiple tends to get smaller as you get older.

- Your Total Debts: They’ll want to know about your mortgage, any business or student loans, and other major financial responsibilities.

- Your Assets: While your assets matter, they’re really weighed against your income and debts to see if there’s a genuine need for cash (liquidity) when you pass away.

- Your Stated Reason: This is huge. You can't just be vague. You need to clearly explain why you need more insurance, because a fuzzy answer can raise a red flag.

The secret is to show them a clear, logical need. You have to connect the dots and show them the "why" behind your request—whether it's for a new mortgage, to protect your growing family's future, or to fund a buy-sell agreement for your business.

How to Justify Your Need for More Coverage

To make the application process as smooth as possible, come prepared to explain your reasoning with specifics. Instead of just saying, “I need more coverage,” tell them the story.

For example, you could say: "My first $250,000 policy was perfect when we bought our starter home. But we’ve since had two kids, our income has doubled, and I need an additional $750,000 term policy to make sure their college is paid for and my income is replaced until they're on their own." That kind of concrete justification is exactly what an underwriter needs to see to sign off on your application.

A solid justification also helps ensure your loved ones have an easier time during the claims process, which you can read more about in our guide on life insurance without a will.

It’s a good idea to have documents like recent pay stubs or mortgage statements handy. When you’re transparent and prepared, you’re not just applying for a policy—you’re showing the insurer that you’re making a responsible financial choice. And that’s what they want to see.

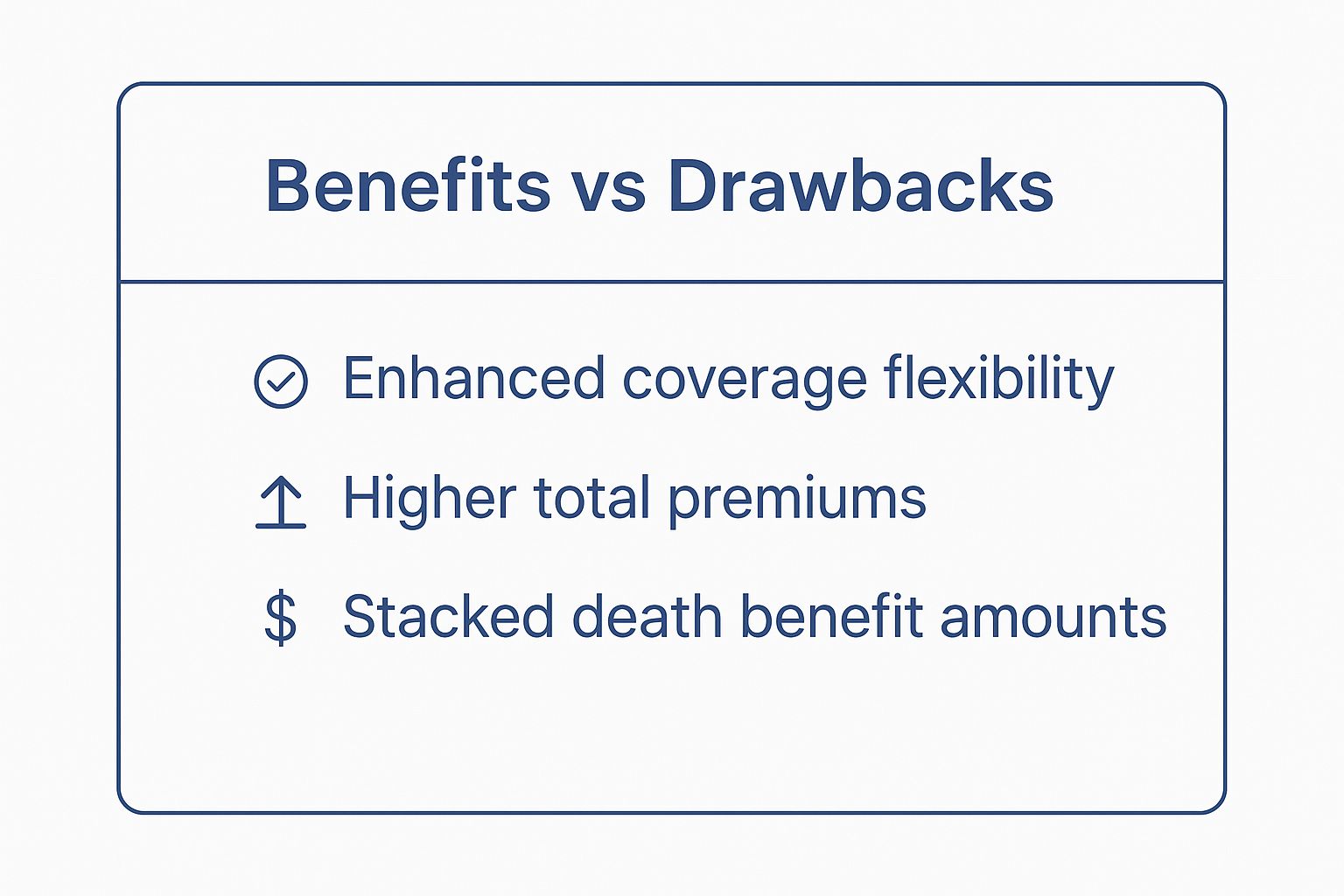

Weighing The Benefits And Drawbacks

Deciding to get a second life insurance policy isn't a simple yes or no answer. It’s a bit like deciding whether to own one all-purpose kitchen knife or a full set of specialized blades. One gives you simplicity; the other gives you precision.

On one hand, holding two policies can give you incredible flexibility and perfectly tailored protection. On the other, it adds a layer of complexity that just isn’t a good fit for everyone. You have to look at both sides to see if the strategic advantages are worth the extra effort for your specific life situation.

The Strategic Upside

The biggest win here is customization. A single life insurance policy is often a blunt instrument, trying to cover every single financial need at once. By using multiple policies, you can give each one a specific job. For instance, one policy could be set up just to pay off the mortgage, while a second one is there to replace your income until your kids are grown and independent.

This targeted approach can actually save you a lot of money, especially if you use a strategy called "laddering." A single, massive 30-year term policy can be pricey because you're paying for maximum coverage for three whole decades. But by layering smaller policies with different term lengths, you only pay for the highest level of coverage when your financial responsibilities are at their peak. As your needs decrease, the smaller policies expire, and so do your premium payments.

As you can see, it all comes down to balancing the enhanced flexibility and stacked death benefits against the reality of higher initial premiums and more to manage.

So, what are the concrete benefits?

- Targeted Protection: You can get really specific. Maybe one policy is for your spouse to cover daily living costs, and another is set up in a trust to fund your children’s college education, making sure every goal is perfectly funded.

- Cost Efficiency Over Time: That laddering strategy we mentioned means your total premium payments will drop as shorter-term policies end. This lines up your insurance costs with your shrinking financial obligations, like a paid-off mortgage or kids finishing college.

- Separation of Needs: This is a huge one for business owners. You can keep your personal and business protection completely separate. One policy protects your family’s home and future, while the other funds a buy-sell agreement for your company, preventing a messy financial crossover.

By combining policies, you’re not just buying insurance; you're building a financial safety net that is both strong and agile. It’s a forward-thinking strategy that understands your financial life isn’t static—it's a journey with evolving needs.

The Practical Downsides

Of course, this approach isn't a magic bullet. It comes with its own set of challenges. The most obvious one is the administrative headache of juggling multiple policies. This means keeping track of different premium due dates, policy numbers, and renewal notices from different companies.

You also have to be careful not to create redundant or overlapping coverage. Without a crystal-clear plan, you could easily end up paying for more insurance than you actually need, which completely defeats the purpose of trying to be cost-effective. You can learn more about how to sidestep these issues by reviewing some common mistakes when buying life insurance.

Finally, there's the very real risk of getting denied. Insurers always look at your "financial justification"—the reason you need the amount of coverage you're asking for. If your combined death benefits seem way out of line with your income (carriers usually cap total coverage at 10-25 times your annual salary), they might reject your application for an additional policy. Being honest and clearly explaining why you need the extra coverage is absolutely critical.

Pros and Cons of Holding Multiple Life Insurance Policies

To make things even clearer, let's break down the advantages and disadvantages side-by-side. This direct comparison can help you see which column carries more weight for your personal situation.

| Benefit | Drawback |

|---|---|

| Customized Coverage: Assign a specific purpose to each policy (e.g., mortgage, income). | More Management: Juggling multiple premiums, documents, and renewal dates. |

| Cost Savings: Laddering policies can lower your total long-term premium costs. | Higher Initial Premiums: Your total monthly payments at the start might be higher. |

| Flexibility: Adapt your coverage as your life changes without canceling older, cheaper policies. | Application Hurdles: Must prove financial justification for the total coverage amount. |

| Separation: Keep business and personal financial protection distinctly separate. | Risk of Over-Insuring: Potential to pay for more coverage than you actually need. |

Looking at this table, the choice really boils down to a personal preference for precision versus simplicity. There’s no single right answer, only the one that best protects your family and aligns with your financial philosophy.

Clearing Up the Confusion: Your Top Questions Answered

Even after mapping out a strategy, it’s natural to have a few lingering questions. Let’s tackle the most common ones head-on, so you can feel confident about your decision to hold two life insurance policies.

Will My Family Actually Get Paid From Both Policies?

Yes, absolutely. Think of each policy as its own separate, legally binding promise. As long as both policies are active and you were upfront on your applications, your beneficiaries are entitled to the full payout from each one.

The insurance companies are contractually bound to honor valid claims. The key is transparency—you must have disclosed your existing coverage when you applied for the second policy. Honesty is everything here.

Is There a Cap on How Much Life Insurance I Can Have?

While there’s no law limiting the number of policies you can own, there’s a practical limit on the total dollar amount of coverage. Insurers call this your "financial justification."

They calculate this based on a multiple of your annual income, typically between 10 to 30 times what you earn, depending on your age and financial needs. It’s their way of making sure the insurance is for protection, not for profit. If the total coverage you're asking for seems way out of line with your financial reality, they’ll likely turn down your application.

The Bottom Line: Your ability to get more coverage comes down to honesty and a clear, provable need. Insurers just want to see that you're making a responsible choice to protect your family, not simply trying to stack up death benefits without a real purpose.

How Do I Juggle Multiple Premium Payments Without Missing One?

When you’re managing more than one policy, staying organized is your new best friend. A simple system is all it takes to prevent an accidental lapse in coverage, which could be devastating for your family.

Here are a few practical tips to keep everything on track:

- Automate Everything: This is the easiest, most foolproof method. Set up automatic payments from your bank account for every policy. You'll never have to worry about a due date again.

- Sync Your Billing Dates: If the carriers allow it, try to line up your premium payments for the same day of the month. It makes budgeting so much simpler when you know exactly when the money is coming out.

- Keep Your Documents in One Place: Create a secure digital folder or a physical binder for all your policy paperwork. This way, you—and more importantly, your beneficiaries—can find everything in one spot when it’s needed most.

- Schedule an Annual Policy Check-In: Set a reminder once a year to sit down and review everything. Do the coverage amounts still match your family's needs? Are your beneficiaries up to date? A quick review keeps your financial safety net strong.

This hands-on approach makes managing multiple policies feel simple and secure, not overwhelming.

Are you ready to build a customized financial safety net for your family? The team at My Policy Quote can help you compare options and find the right combination of policies to fit your specific needs and budget.

Explore Your Life Insurance Options with My Policy Quote Today